Home loans get pricier as banks hike interest rates again

Since the start of 2018, banks have raised rates for fixed and floating home loan packages by 10 to 30 basis points

Singapore

HOME loans are getting more expensive as banks jack up mortgage rates again to as high as 2.05 per cent, the second increase in as many months, in line with sharply higher interest rates.

This could dent some of the enthusiasm in the buoyant property market. One banker also warned that rising interest rates, coupled with declining rents and increasing vacancies raises the risk of defaults in investment properties as borrowers may not be able to cover the higher servicing costs.

Since the start of 2018, banks have hiked interest rates for both fixed and floating home loan packages by 10 to 30 basis points.

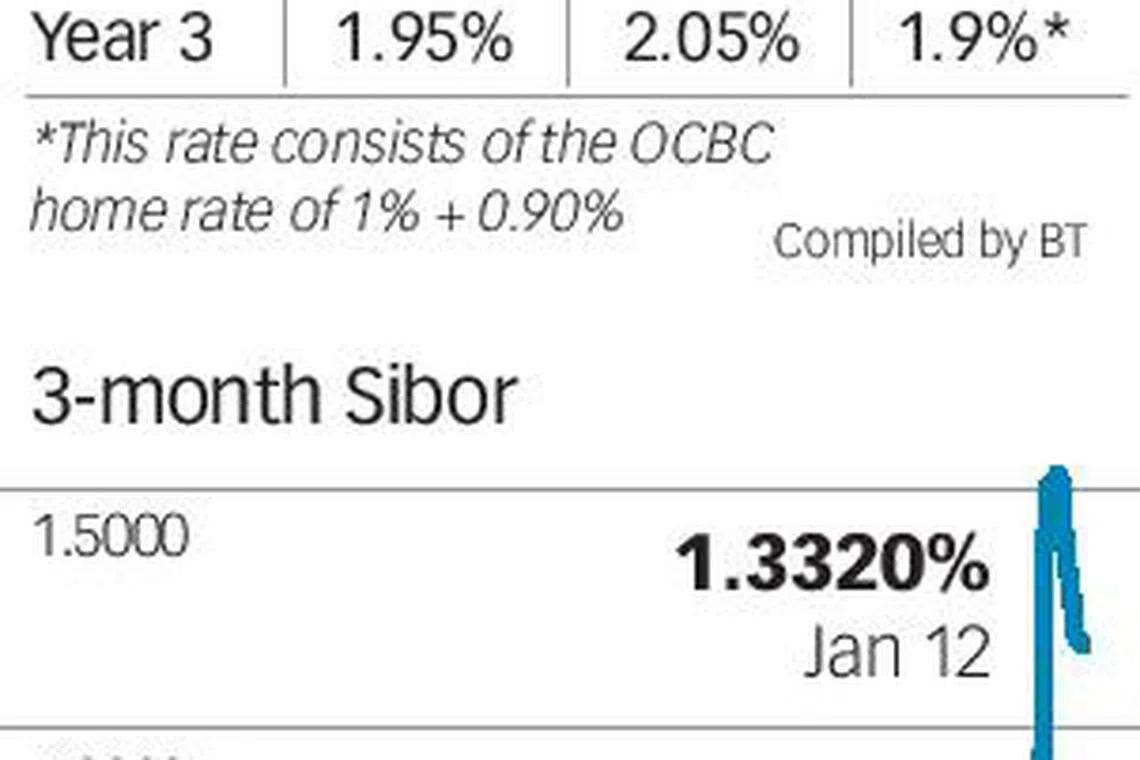

DBS Bank is now charging 1.95 per cent a year for each of the three years for its 3-year fixed rate package. UOB has increased its 3-year fixed rate package to 2.05 per cent a year for each of the three years.

OCBC Bank has raised its 2-year fixed rate package to 1.85 per cent from 1.75 per cent a year for each of the two years. The third-year rate is 1.90 per cent which is made up of the bank's home rate - currently at 1 per cent - plus 0.90 per cent.

The key 3-month Sibor or Singapore interbank offered rate surged towards the end of December to a high of 1.5 per cent on Jan 4, 2018; it had been range-bound for much of the second half of 2017 at around 1-1.1 per cent.

Used to price home loans, the 3-month Sibor has since eased to 1.3 per cent on Jan 12, 2018.

With the hikes from the US Fed Fund Rate in 2017 and the expectation of further hikes into 2018, market interest rates have been rising, said a DBS spokesman.

"This has translated to an increase in mortgage loan rates," he said.

It wasn't so long ago that both DBS and UOB were charging 1.85 per cent a year for each of the three years of their 3-year fixed rate packages in end-November 2017. And two months before that, in September 2017, their 3-year fixed rate packages stood at 1.68 per cent per year for each of the three years.

For every 10 basis points increase on a S$100,000 loan over 25 years, the monthly instalment goes up by S$4.80. So a 30 basis points increase for a S$1 million loan means an extra S$144 every month.

Floating rate loans are more popular among home buyers because fixed rate loans charge a premium of 20-30 basis points, said a banker.

Demand for fixed rate loans remains stable, the banker said. For borrowers who take fixed rate loans, the preference is for the 3-year fixed package as they want longer term certainty said the banker, whose bank sells both 2- and 3-year fixed rate deals.

Rising interest rates may skim some of the froth off the buoyant property market which has seen sales rebound sharply last year.

Pent-up demand for residential properties pushed total private home transactions to about 23,113 in the 11 months of 2017, compared to 16,378 for the whole of 2016.

Developers racked up 10,247 private home sales, excluding executive condominiums, in the first 11 months of 2017, surpassing the 7,972 units sold for the whole of 2016 and a yearly average of 7,576 units from 2014 to 2016.

Bankers caution buyers to assess the impact of higher rates before they make the leap, especially if they are looking at investment properties.

Property prices are affected by various factors, one of which will be mortgage rates, said Vasu Menon, OCBC Bank vice-president and senior investment strategist.

"Rising interest rates may curb the rise in property prices here, but it may not be enough to hurt property prices too badly on its own - especially if there are other positive drivers like a strong economy, a healthy job market and good wage growth," he said.

Given the current weak rental market, a rising interest rate raises the burden of servicing mortgages and reduces the appeal of investment properties, said Mr Menon.

"The ability to service the mortgage on an investment property depends on how easily the property can be rented out and the state of the rental market, which seems weak at the moment," he said.

Rents of private non-landed homes fell 0.5 per cent last year, moderating from a 5.9 per cent drop in 2016, according to flash estimates from SRX Property.

Unless a property owner can rent out his property easily, he may either end up owning a property that is vacant for long periods or have to slash rentals to secure a tenant, said Mr Menon.

"A combination of rising interest rates, lower rentals and prospects of a longer vacancy period, raises the risk of loan defaults among individuals that have investment properties."

Share with us your feedback on BT's products and services