Leasehold favoured over freehold properties in current en bloc fever

Land-starved developers prefer larger leasehold sites that can achieve greater economies of scale and churn out substantial revenue

Singapore

DEVELOPERS' love for freehold property in residential en bloc sales in the past appears to have given way to a preference for leasehold assets in the current en bloc cycle.

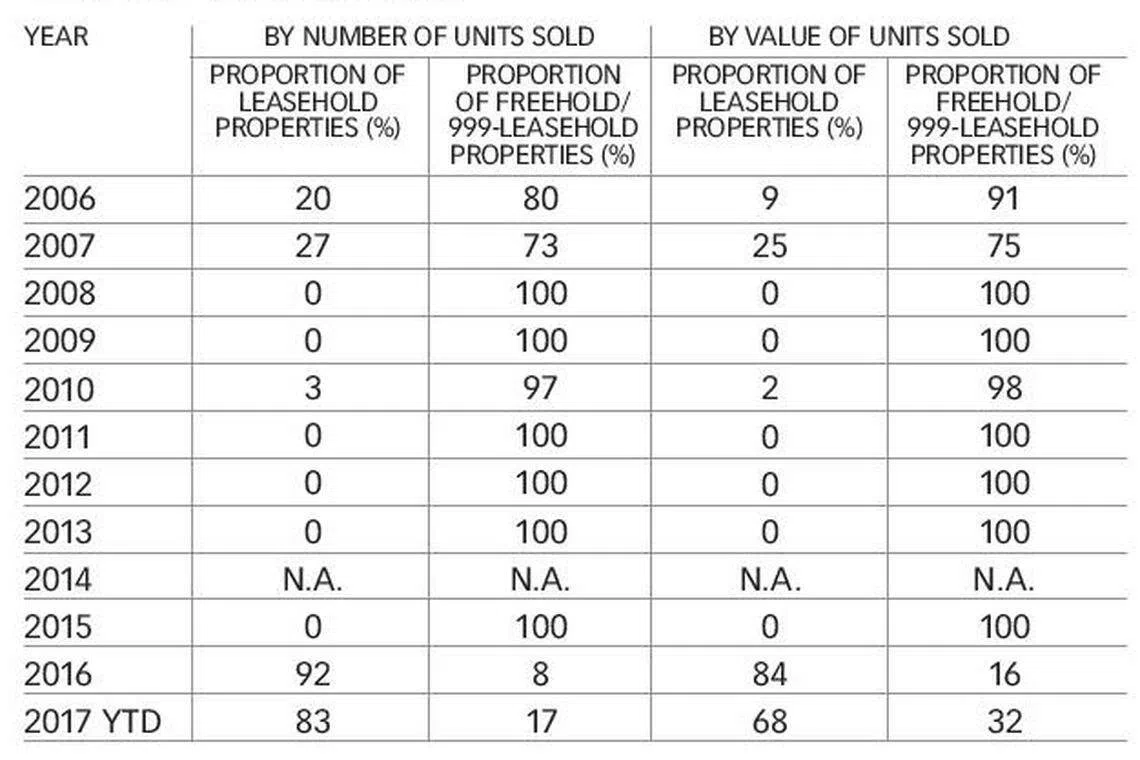

A Cushman & Wakefield study finds that the proportion of leasehold property sold in residential en bloc deals - by number of units sold - has risen to 92 per cent in 2016 and 83 per cent in 2017 year-to-date.

This marks a swing from 2008-2013 when nearly all residential units sold enbloc every year were freehold. The exception was in 2010, when 3 per cent of those units sold collectively were leasehold properties. Freehold property was also the market darling during the previous en bloc boom of 2005-2007, accounting for more than 70 per cent of the total deals by number of units sold, said Cushman & Wakefield research director Christine Li.

The current trend of leasehold-dominant en bloc sales also holds when measured by value of deals, even though freehold properties tend to have higher values.

Many reasons are feeding into this swing from freehold to leasehold, but industry players see insufficient supply from government land sales (GLS) and strong purchasing demand for mass-market private homes among the biggest factors.

Land-starved developers also prefer larger leasehold sites that can achieve greater economies of scale and churn out substantial revenue, said JLL national director for research and consultancy Ong Teck Hui.

Former HUDC (Housing and Urban Development Company) estates are large and relatively cheaper in terms of land rate on a per square foot per plot ratio (psf ppr) basis compared to other residential en bloc sites, thus making them relatively attractive, he told BT.

Interestingly, the last collective sales fever of 2005-2007 was driven by the high-end segment, and eventually spread to the mass-market segment. But this time around, the collective sales cycle started from the mass market. This came on the back of strong purchasing demand for mass-market private homes from Singaporeans, whose buying power is clipped by the total debt servicing ratio (TDSR), which limits their outstanding borrowings at 60 per cent of gross monthly income.

Of the total residential collective sales since last year involving over 3,200 existing homes, about 70 per cent of these existing units are in former HUDC estates, based on BT's estimates.

JLL regional director of investments Tan Hong Boon observed that more privatised HUDC estates than before also became available; given their large scale, they are good candidates to meet developers' land-banking needs.

From 2011 to 2017, seven HUDC estates were privatised - namely Eunosville, Shunfu Ville, Raintree Gardens, Rio Casa, Serangoon Ville, Florence Regency and Braddell View. All of these, except Braddell View, have been sold in collective sales since 2016. Braddell View and earlier privatised HUDC estates Laguna Park, Chancery Court, Lakeview, Ivory Heights and Pine Grove have also started the en bloc process.

Many of the HUDC owners are in their 60s and would want to cash out of their ageing properties that have depleting leases, Mr Tan said.

Cushman & Wakefield's Ms Li noted that the urgency among owners of former HUDC estates may explain their land rates being more reasonable than some freehold properties, whose owners are taking time to "shop around for the best deal".

She reckoned that owners of leasehold properties are also more realistic in their pricing, for fear of being unable to cash out as property value depreciates significantly when the lease drops below 60 years.

Among those showing such urgency was 488-unit Normanton Park, which achieved 80 per cent consensus from owners by share value and strata area in 11 days - likely the fastest on record - even though they have up to 12 months to do so.

Ms Li noted that the typical timeframe for achieving the 80 per cent consensus is around six to nine months for medium to large-scale projects with at least 100 owners.

Demand from HDB upgraders has also been strong in recent years, she flagged. This year, total non-landed residential homes snapped up by HDB addressees stood at 35 per cent, up from 22 per cent in 2007.

Given the buying demand from upgraders and an all-time low in demand from foreigners who tend to favour prime locations, developers may prefer popular HDB estates in suburban locations where most homes are leasehold properties.

She believes the 10-15 per cent price premium that freehold properties tend to command over leasehold properties also present a hurdle to quantum-sensitive buyers and investors as the TDSR remains in place.

Agreeing, Knight Frank's head of investment and capital markets Ian Loh said: "Affordability has got a big part to play in a product that can sell in Singapore's highly regulated real estate market." Thus, developers have shifted their focus.

Mr Loh reckoned that massive infrastructural improvements with the opening of new MRT lines have also lifted the prices of properties in non-prime areas. Owners may think it is time to unlock that value through the en bloc process.

The Urban Redevelopment Authority pointed out on Friday that the redevelopment of en bloc sites sold will add a significant number of housing units to the existing supply pipeline.

About 9,300 units could be generated from awarded en bloc sale sites from 2016 till mid-October this year. They form part of the potential supply of about 16,700 units (including executive condominiums) with no planning approvals yet, with the balance 7,400 units coming from awarded GLS sites.

A large part of this new supply of 16,700 units could be made available for sale in the next one to two years, and be completed by 2021 onwards.

READ MORE: Tanglin Shopping Centre in third bid at en-bloc sale

Share with us your feedback on BT's products and services

TRENDING NOW

Singapore Kitchen CEO, senior manager charged with alleged fraud, falsifying accounts; both to stay in jobs for now

Profit with purpose: Kim Choo Kueh Chang’s pivot from public listing to protecting heritage

HSBC, AIA, Prudential shares slide after report of Hong Kong bank account curbs

How the ultra-rich buy property