High net worth wealth reverses 7-year uptrend in 2018

Singapore

GLOBAL wealth held by high net worth individuals (HNWI) deteriorated in 2018 after seven consecutive years of growth, dragged down by Asia Pacific and China, in particular.

Capgemini's World Wealth Report 2019 said some US$2 trillion in wealth evaporated last year, half of which was accounted for by the Asia Pacific.

Almost all asset classes did poorly last year, weighed down by concerns over a global economic slowdown, trade tensions and expectations of higher interest rates. Global market capitalisation was down by nearly 15 per cent at end-2018. Asia Pacific ex-Japan markets registered the steepest fall of 23.8 per cent. Markets have since rebounded this year.

Still, Capgemini said asset allocations shifted significantly as cash replaced equities to become the most held asset class in Q1 2019, representing 28 per cent of HNWI financial wealth. Equities slipped to second position at nearly 26 per cent, a decline of five percentage points.

Among Asia ex-Japan HNWI, equities allocation dropped by five percentage points to 22 per cent, but the share of alternative investments rose by 4 percentage points, thanks to keen interest in private equity and venture capital.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

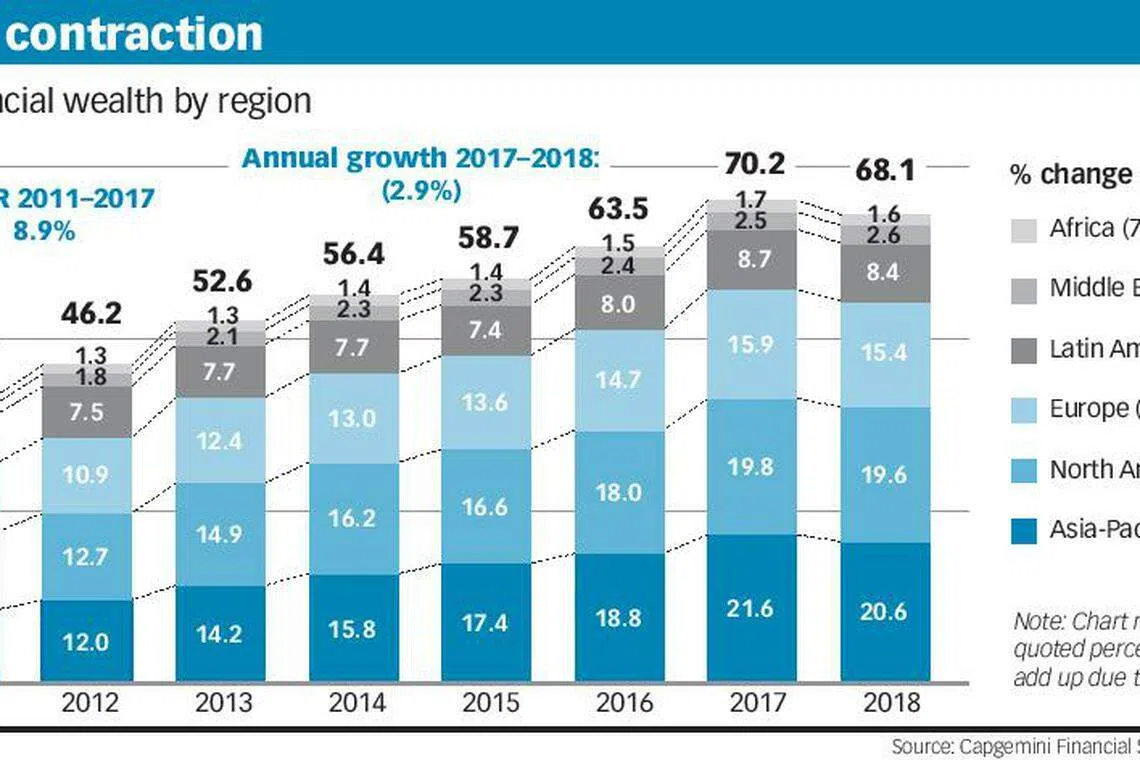

HNWI financial wealth globally was estimated at US$68.1 trillion, held by 18 million individuals. Asia-Pacific wealth was estimated at US$20.6 trillion, giving it a 30 per cent share.

Over the past seven years, Asia-Pac had been the driver of global wealth, with overall growth of 92 per cent since 2011, compared to global growth of 62 per cent.

China accounted for nearly 53 per cent of the overall Asia Pacific wealth decline, and 25 per cent of the overall global HNWI wealth decline. Chinese markets lost more than US$2.5 trillion in market capitalisation due to trade tensions with the US and pressure on the yuan.

In terms of wealth bands, the ultra HNW segment, defined as those with assets of at least US$30 million, was hit hardest, as its population and wealth were down by 4 and 6 per cent, respectively. This segment accounted for 75 per cent of the total global wealth decrease.

The "millionaire-next-door'' segment (wealth of US$1-5 million) were the least affected, as their wealth dipped by less than 0.5 per cent. This segment accounts for almost 90 per cent of the HNWI population.

The silver lining was that trust level and satisfaction in wealth management firms rose by 3 percentage points, despite the contraction in wealth. Globally, net promoter scores (NPS), which indicates the likeliness to recommend one's primary wealth manager, rose by 3 percentage points in Q1 2019 on a year-on-year basis. But in Asia Pacific ex-Japan the NPS dropped by about 15 percentage points. Capgemini said the decline is likely due to volatile economic conditions and market performance, "combined perhaps with limited progress on digital and hybrid advice offerings''.

An unsatisfactory service experience was the biggest reason for HNWIs to switch firms last year. Fewer than 50 per cent of HNWI clients said they were satisfied with current mobile and online platforms, and 85 per cent demanded more digital interaction when accessing portfolio information.

Anirban Bose, chief executive of Capgemini's financial services strategic business unit, said the wealth management industry is at a crossroads. "Future success will depend on the ability of wealth management firms to evolve the client experience and find new ways to add value through more personalised services... The landscape is shifting so quickly that companies must not be afraid to overhaul their strategy and business models if needed.''

Copyright SPH Media. All rights reserved.