Analysts warn of high uncertainty, inflation risks pressuring rate decisions after Iran conflict

The impact depends on how the conflict plays out as well as whether markets have accumulated enough fundamental strength, say analysts

[SINGAPORE] Oil and gold prices surged while defence stocks rose. But global aviation stocks dived, and markets from Asia to Europe fell on the first trading day after the US and Israel’s weekend attacks on Iran.

The aftermath played out unevenly across sectors, but the broad impact on markets is yet to be seen – and largely depends on how the conflict plays out, as well as whether markets have accumulated enough fundamental strength, say analysts.

Still, they say these geopolitical tensions are set to weigh on equity valuations in at least the short term.

On Feb 28, the US and Israel launched strikes against Iran, pushing the Middle East into a renewed conflict that has widely disrupted global air travel, with key international airports in the region, such as Dubai, remaining shut.

Ayatollah Ali Khamenei, the supreme leader of Iran, was declared dead, along with several other leaders of the country. Iran’s security chief said on Monday (Mar 2) that the country will not negotiate with the US.

Thousands of flights globally have been disrupted due to the most recent strikes as the region’s airspace stayed closed. That includes the cancellation of 26 Singapore Airlines (SIA) and Scoot flights between Feb 28 and Mar 7. Other SIA flights could be affected, too, amid the fluid situation, said the national carrier on Mar 1.

Limited market correction – or something worse?

Asia markets broadly ended lower on Monday, with the Straits Times Index slumping 2.1 per cent to 4,890.86. Losers outnumbered gainers 511 to 191.

DBS ended 2.6 per cent lower at S$55.63, OCBC closed 2.3 per cent down at S$20.93, and UOB fell 1.8 per cent to S$36.30. Singapore Airlines (SIA) ended the trading session 4.7 per cent down at S$6.84.

Meanwhile, Singapore-listed energy and gold counters, as well as defence stock ST Engineering , were up.

SEE ALSO

“The STI’s 1.76 per cent decline this morning is a rational repricing, not a panic,” said Oriano Lizza, sales trader at CMC Markets Singapore, adding that the market is differentiated as he noted the different performances of CNMC Goldmine , ST Engineering and SIA.

“Bank declines of 1.5 to 2 per cent are sentiment-driven, not balance-sheet events,” he added.

“Singapore’s safe-haven credentials are structural; they play out over quarters, not during the first hours of a shock. Once volatility clears, the ‘AAA’ rating, deep capital markets, and institutional stability should reassert their pull on capital flows.”

In Japan, the Nikkei 225 fell 1.4 per cent on Monday, and the Topix closed 1 per cent down. Hong Kong’s Hang Seng Index was down 2.1 per cent. South Korean markets were closed for a holiday. China’s Shanghai CSE 300 Index rose 0.4 per cent, while Australia’s ASX 200 ended the day flat.

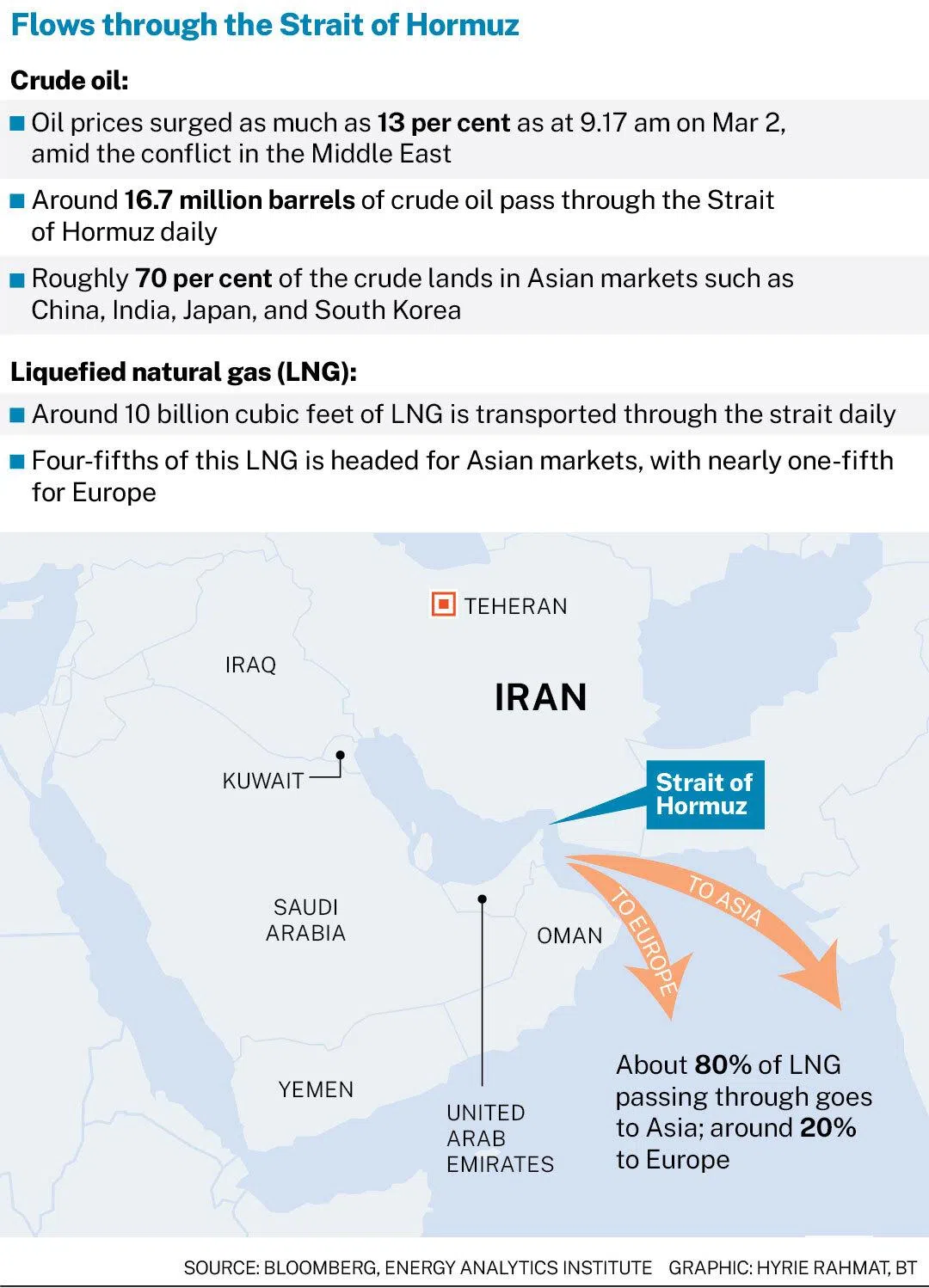

Spot gold prices were up 2.2 per cent at US$5,392.70, while Bitcoin slumped to US$66,266 on Monday evening. Brent oil was last up 6.2 per cent at US$76.76 a barrel. Gas prices also rose, with Asian liquefied natural gas (LNG) benchmarks soaring more than 30 per cent.

Overall, how markets pan out – as a mild correction or something worse – will depend on the duration of the conflict, Lizza said.

“The single variable that determines whether this is a 5 per cent correction or something worse: Does commercial shipping through Hormuz resume within two weeks?” he asked. “A contained, short engagement likely recovers most of today’s losses, while a protracted regional conflict will force a fundamental portfolio rethink,” he added.

Qatar has the world’s third-largest LNG export capacity, and around 20 per cent of global LNG trade transits the Strait of Hormuz, making shipping risk a gas-market event as much as an oil-market event.

CGS International said in a note that the key question is not just geopolitical impact. “If balance sheets remain robust, geopolitical shocks are likely treated as buy-the-dip opportunities,” it said.

“However, elevated leverage or rising hesitation could amplify price reactions – this would allow correlations to spread, with previously underperforming sectors such as energy and resources potentially moving next, in our view.”

Lizza said this is the type of threshold where a pricing event becomes a fundamentals event and forces central bank responses, from the US Federal Reserve to the Monetary Authority of Singapore (MAS).

Christian Gattiker, head of research at Julius Baer, said that sector dispersion is likely to dominate at present, where cyclicals, consumer-facing industries, chemicals and transport remain most “exposed” to sustained energy cost pressure.

Do not buy the dip

Analysts warn that investors should not make hasty investment decisions amid the present “short-run” conditions.

“We would not yet label this a clean buy-the-dip set-up, as duration, shipping/insurance mechanics, and the endgame matter more than the first headline,” said market strategists from Franklin Templeton.

Afdhal Rahman, executive director of wealth advisory at OCBC, pointed out that clear political incentives frame this argument, with US midterm elections approaching this year, and an electorate fatigued and sceptical of “forever wars”.

“The Trump administration has an incentive to keep the conflict contained and brief,” he added.

Still, while the midterm elections argue against a protracted conflict, uncertainty remains high, said Julius Baer’s Gattiker.

“Against the current backdrop, chasing short-term moves appears less attractive than maintaining discipline: A defensive bias remains warranted until greater clarity on the trajectory of the conflict emerges.”

Inflation and interest rates

Surging oil prices will also create heightened inflation risks, in turn causing central banks to be on the defensive again.

Ipek Ozkardeskaya, senior analyst at Swissquote, noted that energy typically makes up around 8 to 10 per cent of consumer price index baskets. However, during major shocks, it can account for up to one-third to half of headline inflation, with indirect effects amplifying the impact further.

“This, combined with the US producer price index coming in significantly higher than expected last Friday, suggests that the last mile towards the Federal Reserve’s 2 per cent target could be even more complicated than previously anticipated,” she said.

Ozkardeskaya added that in Europe, a period of rising energy prices could compromise the recent easing of inflation below the European Central Bank’s policy target.

Nigel Green, CEO of global financial advisory firm deVere Group, said investors are “now confronting a renewed inflation threat at a moment when price growth in major economies remains above or only just approaching central bank targets”.

“Policymakers who believed inflation was moving steadily back towards target would face renewed pressure,” he said.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

ABSD deadline extended to up to 7 years for developers of large en bloc sites to encourage reuse of land

15-month wait-out curb lifted for private property owners buying HDB resale flats

Mortgagee-sale listings hit six-year high in H1 2026 as financing conditions tighten

Knight Frank winds down real estate agency unit, agents to move to OrangeTee & Tie