Digital assets to improve capital market liquidity, banking efficiency

Innovations in areas such as central bank digital currencies and asset tokenisation could mark significant improvements to the way digital payments and capital markets operate

CRYPTOCURRENCIES and their associated significant risks, uncertain valuation and high volatility may come to mind when digital assets and blockchain technology are brought up. As such, UOB has refrained from participating in the cryptocurrency space, nor offering cryptocurrencies to clients, until related investment protection regulation is securely in place.

Still, UOB believes that related innovation around these underlying blockchain technologies could improve how capital markets function and generate efficiencies for the lender, streamline operations, make transactions more efficient, and enable banks to offer innovative products.

In the area of digital assets, UOB Head of Blockchain and Digital Assets, Leong Yung Chee believes that they will become an important asset class, and will eventually see significant and widespread use across the banking industry.

He largely categorises digital assets into four key types - Central Bank Digital Currencies (CBDCs), tokenised securities, stablecoins and cryptocurrencies.

Among these categories, the bank is focused on developing use cases around CBDCs and tokenised securities and is keeping a close tab on stablecoins.

Leong says that CBDCs could complement fiat money and transform the payment landscape, while tokenised securities could help fractionalise assets such as equities, bonds, structured products and even real estate.

In the area of CBDCs, he notes that existing payment and transaction processes, particularly for cross-border payments, still rely heavily on different workflows to transfer funds in a secure manner daily.

"The use of blockchain technology and upcoming innovation in the form of CBDCs can innovate this process further, by reducing latency and friction in payment, thereby improving the speed, transparency and security of payment," he says, adding that they could be applied to retail, wholesale and cross-border payments.

For example, cross-border payments could be made more efficient and secure with CBDCs. This could reduce payment costs and further improve financial inclusion among unbanked consumers globally.

Already, numerous central banks worldwide have been experimenting with CBDCs as well. In the latest update by the Bank for International Settlements (BIS) published in Jul 2023, the BIS noted that "the responses from 86 central banks show that the proportion engaged in some form of CBDC work has risen to 93 per cent and that the work on retail CBDC is more advanced than on wholesale CBDC". Specifically, the BIS noted that "there could be 15 retail and nine wholesale CBDCs publicly circulating in 2030".

Money bound for specific purposes

On the digital Singapore dollar front, UOB is working with the Monetary Authority of Singapore (MAS) on Project Orchid, which is a series of industry pilots testing different use cases. One such use case is the concept of Purpose Bound Money (PBM).

Leong says that while money has traditionally been used broadly, PBM can help to make the use of money more targeted by defining specific and targeted uses.

"For example, blockchain technology is now used to ensure that donations of funds reach the desired charity organisations and are used for the specific charitable cause, thereby reducing fraud," he says, noting that PBM could also improve efficiency and security.

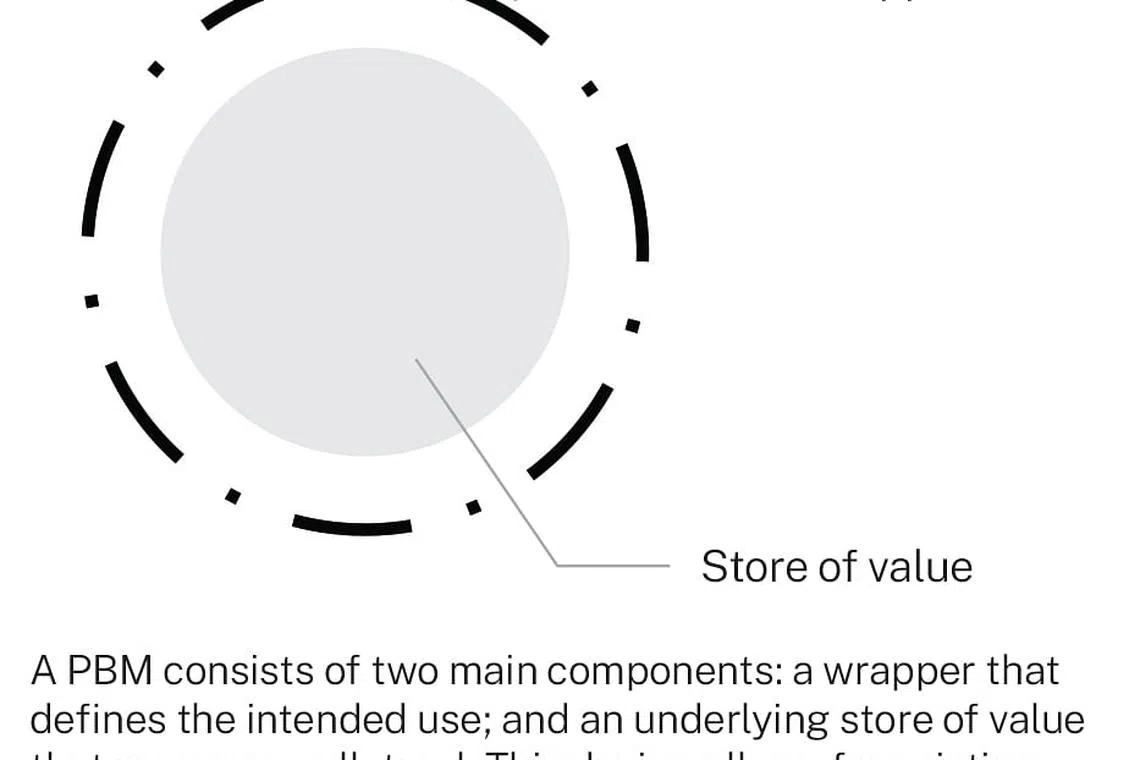

In essence, PBMs involve a programmed wrapper applied around an existing digital money token, which stores value. When certain payment conditions are met, the wrapper is removed so that the digital money token is released and transferred to the recipient, who could be a merchant or service provider.

At the Formula One festivities in September this year, UOB was part of the industry team that piloted the use of PBM for programmable rewards. Consumers received digital vouchers in their Singapore Pitstop Pack, which had a set validity period and pre-selected merchants that could receive the digital money.

"When a consumer pays for his purchase using PBM, funds are transferred to the merchant immediately if the terms of use are fulfilled, with minimal follow-up reconciliation processes," Leong says, adding that the bank continues to work with the industry to explore and experiment with new use cases.

As for tokenised securities, Leong says that the fractionalisation of existing financial assets could make fund raising more efficient.

"(Tokenised securities) can potentially add more liquidity, generate more value, and bring more accessibility to these underlying assets.

"In addition, the underlying blockchain technology can help make the process of managing the distribution, trading and corporate action of these assets more efficient and thereby reducing cost and inefficiencies," he says.

He notes that UOB, as part of MAS-led Project Guardian, in collaboration with HSBC and Marketnode, has successfully concluded the technical pilot on the issuance and distribution of a digitally native structured product. Marketnode is a joint venture between Singapore Exchange group and Temasek.

"The pilot successfully demonstrated the potential for lower issuance costs, reduced issuance and settlement times and deeper customisation," he says.

The pilot, which was launched in November 2022, aimed to fully digitalise the wealth management product value chain, which is largely paper-based, using distributed ledger technology.

Distributed ledger technology refers to platforms where ledgers are stored on separate, connected devices in a network to ensure data accuracy and security.

"We will continue to further pilot the issuance of equity linked structured notes under HSBC's existing issuance programme, tokenised by Marketnode's multi-asset issuance platform, and distributed by UOB for its wealth management activities," Leong says.

With these new use cases, Leong notes that they are still in their infancy as the technical design of the underlying blockchain technology improves by "leaps and bounds" on a regular basis.

"Until the use case can evolve and mature into a more impactful business case with broader potential for real world application in the banking system and the economy, there will be significant risks and costs involved in terms of the constant experimentation," he says, adding that industry partnerships are crucial when testing new blockchain-related use cases.

He notes that in the area of asset tokenisation, UOB has already partnered successfully with digital securities trading platform ADDX to tokenise green bonds and digital bonds.

Managing stablecoin risks

Another space that UOB is actively observing is that of stablecoins, which are cryptocurrencies pegged to another currency or asset with a stable value.

"Given their unique ability to maintain a stable value and redemption at par, stablecoins have the potential to offer the reliability of value and provide a potential bridge for the transfer of value between fiat money and cryptocurrencies," Leong says.

Still, he notes that there have been incidents of fraud among algorithmic stablecoins, and regulation is not yet in place to govern the use and trading of collateral-backed stablecoins.

In August this year, MAS announced that it had revised its stablecoin regulatory framework and is seeking feedback from industry players before finally proposing changes to the Payment Services Act.

Under the draft amendments, stablecoin issuers who wish to be labelled "MAS-regulated" must submit independent attestations of their reserves on a monthly basis to the central bank and upload them on their websites, among other requirements.

Leong says that the bank maintains its stance against offering or participating in cryptocurrencies to its clients and partners as it prioritises the security of their assets.

"Recent events of the past few months involving fraud and risk management issues in the cryptocurrency space reinforced our prevailing concerns," he says.

He adds that cryptocurrencies' risk treatment under Basel rules are akin to assets close to default, and that robust global regulation for consumer protection is not yet in place.

Instead, Leong says that the bank's innovations around digital assets and blockchain technology revolve around making the banking process more efficient.

"All these innovations have one singular goal in mind: To further make the banking experience more efficient, more secure and more pleasant for our banking consumers," he says.

Brought to you by

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services

TRENDING NOW

Extra S$300 in CDC Vouchers, U-Save rebates for households as part of S$900 million support package

Singapore banks’ battle for wealth talent goes beyond private bankers

Keep moving, keep learning, live fully: Lessons from actor Tay Ping Hui and a ‘granfluencer’

Philippines’ income upgrade hides grim reality for most Filipinos