From foreign exchange fees to recurring software bills: What is draining your business – and how to preserve your profits

As hidden transaction costs chip away at margins, tools like the UOB Business World Debit Card can help small enterprises keep more of what they earn

SINGAPORE’S small and medium-sized enterprises (SMEs) are transforming fast.

As they embrace technology and pursue global growth ambitions, their operating behaviour and spending habits are seeing an equally rapid shift: Cheques and manual invoices have been replaced by digital-first payment methods, and domestic market-focused companies are increasingly building a global-by-default business model.

A typical SME today may pay for digital advertisements on Meta or Google, for tools like Adobe and OpenAI, and to overseas suppliers or service providers – all within the same month, and almost all online.

The numbers reflect that. Overall digital payments adoption in Singapore stood at 92 per cent in 2025, with the total market projected to grow to US$480.6 billion (S$622 billion) by 2030, or at a compound annual growth rate of 18.3 per cent, according to PwC.

The changes in the spending mix, however, often comes with hidden costs.

Two pressure points stand out: rising foreign exchange (FX) exposure and the growing weight of recurring digital subscriptions. The fact that payments to overseas merchants or clients can incur a mark-up of about 3 per cent on FX conversion shows how steep the charges can get and how quickly these extra costs can add up.

As these costs scale quietly in the background, even small inefficiencies can weigh on margins. Reducing FX charges on your Google Ads digital ad spend or software-as-a-service subscriptions, for instance, can translate into meaningful savings over time. Greater fee transparency also gives businesses clearer visibility over their outflows – an increasingly important advantage as operating environments grow more complex.

Against this backdrop, payment tools are evolving alongside SME needs. Cards like the UOB Business World Debit Card have been designed with the spending behaviour and saving needs of today’s businesses in mind.

Saving with minimal effort

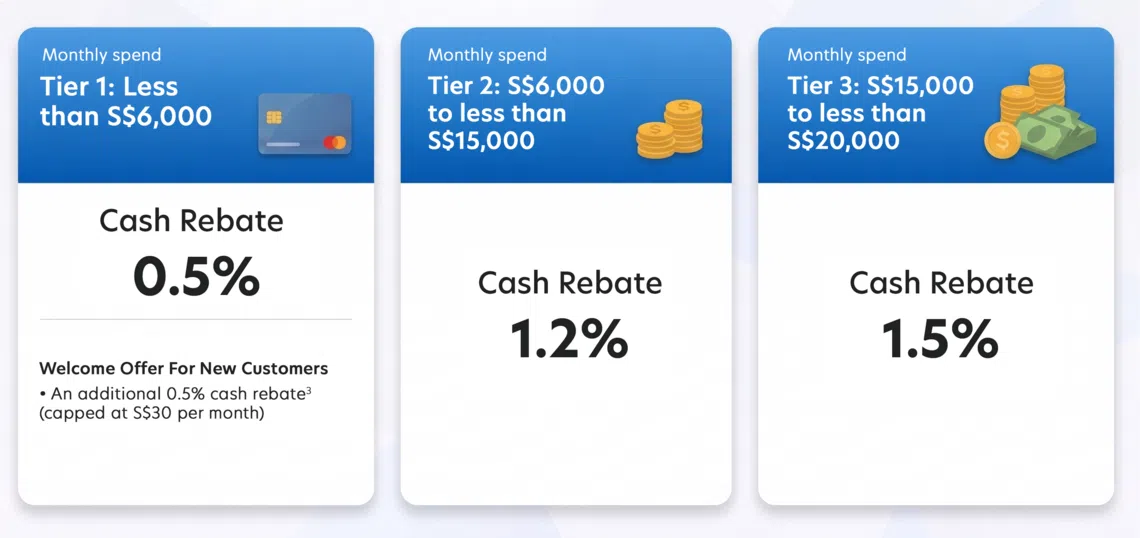

With up to 1.5 per cent cash rebate1 on local spending, and zero foreign transaction fees worldwide1 with no minimum spend and cap – a feature increasingly offered by many fintech debit cards – the UOB Business World Debit Card allows SMEs to enjoy similar cross-border payment savings while backed by a full-service bank.

These features enable businesses to save on everyday local and international transactions without changing the way they operate. Over time, these incremental savings add up, especially for businesses with recurring local and international expenses.

As more payments move online and across borders, another increasingly relevant consideration for SMEs is the increased risk of unauthorised transactions. The UOB Business World Debit Card safeguards companies against such risks, offering complimentary corporate waiver liability of up to US$1.5 million2 per company.

Says Tan Min Yeow, head of Singapore Cards and Payments, UOB: “When developing the card’s value proposition, the aim was to address two of the most common challenges SMEs face today: ongoing business expenses and exposure to cross‑border transaction costs.

“Rather than requiring businesses to monitor spend thresholds, rebates or adjust how and when they pay, the features were designed to work automatically, delivering savings through routine spending. This reflects how SMEs operate in practice, where simplicity, predictability and cost efficiency are key.”

Customers who are new to the UOB Business World Debit Card can enjoy an exclusive sign-up offer3 when they apply before Jan 31, 2027. They can also earn up to S$4,500 cash bonus per annum1 when they bundle it with a UOB eBusiness Account4. For SMEs managing tight cash flows, such upfront gains can provide a practical buffer, helping to ease day-to-day expenses.

This has never been more important. Swings in the currency markets have increased dramatically this year amid geopolitical upheavals and rising oil prices, both of which have disrupted supply chains and put many businesses under pressure. Amid these shifts, tools that bolster the bottom line without adding complexity become valuable.

Having a banking partner that grows with you

As operating conditions become more complex, some SMEs are placing greater value on banking partners that offer more than just individual products.

Increasingly, businesses are looking for a banking partner that can connect them to the broader financial ecosystem, providing access to infrastructure and integrated services that can support them at different stages of growth.

This is where UOB plays a pivotal role in driving growth for SMEs through strategies designed to strengthen capabilities and build resilience, helping businesses participate more confidently in the wider business ecosystem.

One of UOB’s SME capability-building initiatives is the UOB BizSmart programme, an ecosystem of partners offering a suite of digital solutions across seven categories – accounting, human resources (HR) and payroll, digital transactions and marketing, payments and point-of-sale systems, cybersecurity, business essentials and artificial intelligence. These digital tools can empower SMEs to run smarter and scale sustainably.

Through UOB’s digital banking platforms, SMEs can also link select accounting and HR or payroll solutions to their UOB business account, providing a more complete view of their finances, faster salary processing and improved day-to-day oversight.

UOB BizSmart also includes complimentary advisory services from digital advisers, who work with SMEs to understand their business needs and recommend suitable technology partners.

As SMEs grow more digital and internationally connected, payment tools are evolving beyond convenience alone to play a larger role in managing costs, cash flow and operational efficiency.

Through the UOB SME app, SMEs can access an interactive dashboard to get real-time visibility over cash flow, book preferential FX rates and create personalised watchlists to monitor currency movements. They can also receive market insights and invitations to events that facilitate networking with industry peer networks.

Products such as the UOB Business World Debit Card, with zero FX fees worldwide, cash rebates on local spend and built-in protection against unauthorised transactions, reflect this broader shift in business banking.

This year, UOB was named the World’s Best Bank for SMEs by The Digital Banker and the Best SME Bank in Asia Pacific by The Asian Banker. These awards reflect UOB’s continued focus on supporting SMEs through its regional network, connecting businesses of different sizes to opportunities across ASEAN and beyond.

Extra rebates for new sign-ups

For small and medium-sized enterprises already looking to optimise everyday spending, current sign-up promotions offer a modest but practical boost to baseline savings.

From now to Jan 31, 2027, businesses that sign up for the UOB Business World Debit Card can receive an additional 0.5 per cent cash rebate on eligible local spend, capped at S$30 per month over a 12-month period.

This comes on top of the base cash rebate structure, which starts from 0.5 per cent with no minimum spend and no cap. Depending on monthly spend, the total rebate can range from 0.5 per cent to 1.5 per cent. Over the full promotional period, the additional rebate is capped at S$360 per card.

Learn more about how the UOB Business World Debit Card can help your business.

Footnotes:

1Subject to qualifying criteria. Terms and conditions apply.

2Up to US$1,500,000 per company per annum or US$10,000 per card user per annum coverage. The company needs to have two (2) or more cards in good standing on or after establishing a card account with UOB or as otherwise agreed.

3Sign up from March 9, 2026 to Jan 31, 2027 (both dates inclusive). A Sign Up Cash Rebate of 0.5 per cent (“Sign-Up Cash Rebate”) will be awarded based on eligible local spend from March 9, 2026 to Feb 28, 2027 (both dates inclusive), capped at S$30 per month during the 12-month promotional period. Total Sign Up Cash Rebate is capped at S$360 per card. The Sign Up Cash Rebate is awarded in addition to the Base Cash Rebate (which varies from 0.5 per cent to 1.5 per cent depending on the monthly volume of eligible local spend). The base 0.5 per cent cash rebate has no minimum spend and no cap. Medical Transactions earn a flat 0.2 per cent rebate and do not earn any other rebate. Visit uob.com.sg/bizdebitwelcomeoffer for details.

4SGD deposits are insured up to S$100k by SDIC.

Share with us your feedback on BT's products and services

TRENDING NOW

Yeoh Pei Xien: YTL’s third-gen scion with a pastor’s heart

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Keppel H1 net profit drops 59% to S$155 million on impairments, M1 deal fallout; shares fall 4%

Singtel explores Nasdaq-SGX dual listing for data centre arm Nxera, local data centre Reit