Time to get personal about personal finance

Anxious about making the right investment decisions? You don't need to be the smartest in the room, just ask what you want out of life

Singapore

FINANCIAL planning can be daunting if we don't know where to start.

Global asset management firm Franklin Templeton released a survey just this month which showed that young Singaporeans are eager to invest, but a third of them are also anxious about making the right investment decisions.

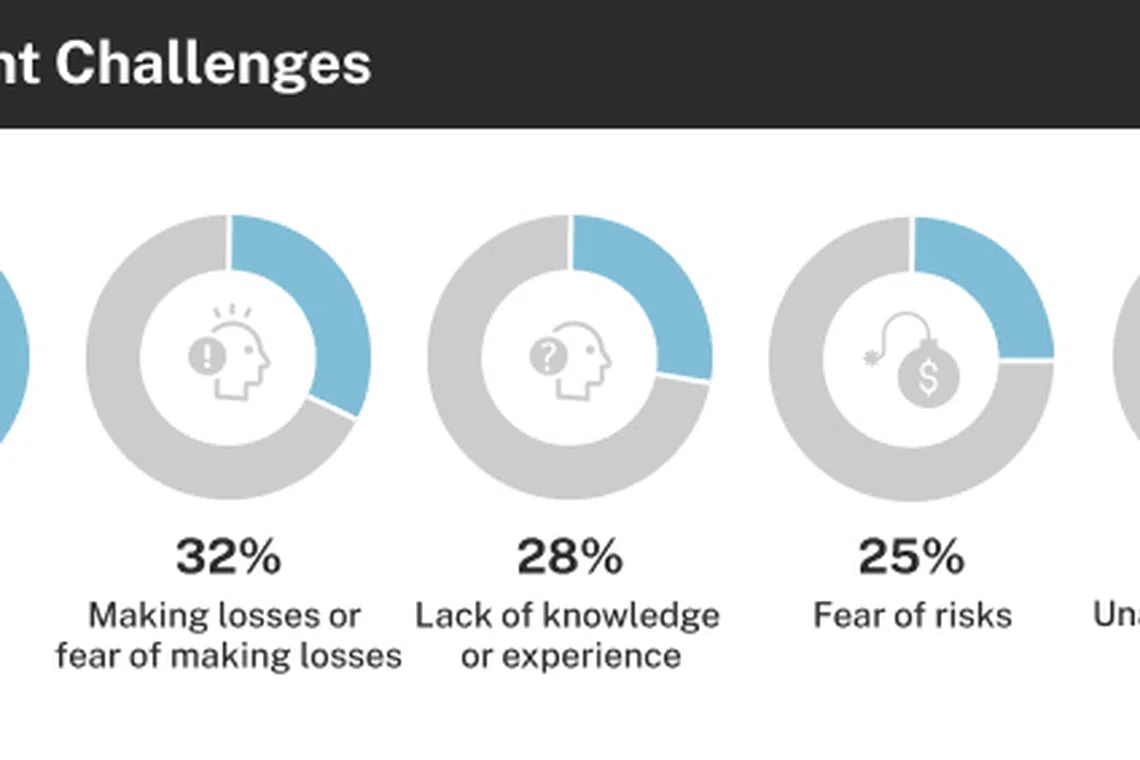

The inaugural Next-Gen Investor Survey - which polled 500 Singaporeans aged between 18 and 35 - suggested that for young investors, having a limited budget, fear of incurring losses and a lack of investment knowledge are among the top challenges this generation is confronted with when thinking about investments.

Half of the respondents agree that investing should start at a young age and that it is an important practice for financial planning.

But about a third also agreed with statements such as "making the right investment is difficult" and "investment makes me anxious".

Let's address this anxiety.

Perhaps what helps is to think about the fundamentals of personal finance: It's about you.

That means the investment targets are defined by the investment timeframe and the goals that you might have. It also depends on your lifestyle expectations.

Morgan Housel, author of The Psychology of Money, pointed out in his book: "Money's greatest intrinsic value . . . is its ability to give you control over your time. To obtain, bit by bit, a level of independence and autonomy that comes from unspent assets that give you greater control over what you can do and when you can do it."

The richest dividend to be paid from personal finance, is therefore, freedom. Having this as a starting point would better define your outlook on market risk, and taking the first steps to investing.

Back to the Templeton survey, which showed that slightly over a third have a limited budget for investment while 32 per cent have made losses or fear making losses.

Nearly 30 per cent of the respondents feel they lack investment knowledge or experience, while a quarter find investment too risky.

On risks, Mr Housel would point to a quote from Benjamin Graham. In explaining the concept of margin of safety, the famed investor said "the purpose of the margin of safety is to render the forecast unnecessary".

The bottom line here is to keep room for error. That ability to endure volatility will keep you invested long enough to let the odds of benefiting from a low-probability outcome fall in your favour, said Mr Housel.

"Compounding doesn't rely on earning big returns. Merely good returns sustained uninterrupted for the longest period of time - especially in times of chaos and havoc - will always win."

Warren Buffett would also point to the experience of hedge fund manager Long-Term Capital Management (LTCM), which went bust in 1998 amid a roaring bull market, despite being run by rich and smart traders.

LTCM took outsized leverage bets and were caught out by crises.

"To make money they didn't have and didn't need, they risked what they did have and did need - and that's foolish. Doesn't make any difference what your IQ is. If you risk something that is important to you for something that is unimportant to you, it just does not make any sense," Mr Buffett said.

So at a time of loud social-media chatter, find a way out of noisy comparisons about your financial worth.

Start by valuing yourself, to ask: What do you want from life? Personal finance begins from there on.

READ MORE:

- Boom or bust: my one week roller coaster with AMC

- Young, raring to go - and time to start prepping for retirement

We asked four financial professionals what finance means to them personally, and what is the one thing they would like to improve about financial access in Singapore. Here's what they shared:

Samuel Rhee, Chairman and Chief Investment Officer, Endowus

People think of finance as an abstract concept but it's more intertwined in their lives than most would imagine. From buying your daily cup of coffee, to thinking about how you want to grow your "spare" income, finance is something that can bring about significant change in a person's life, as well as improve an entire society.

Retirement as a financial topic is extremely close to my heart, and I'm passionate about solving the generational challenges of retirement today - being able to deliver on a quality of life by starting your financial journey as early as possible. At its core, the financial industry is supposed to deliver on the aspect of "service", to meet the clients' needs as a fiduciary of their wealth and to always work in their best interests in all scenarios.

In my over two decades of experience in the wealth industry, truly serving a client's needs does not naturally take precedence over profit. Providing access should be at the heart of what we do as wealth advisors as custodians of a person's hard-earned savings. Many times, we've seen how unfairness in the industry can be exhibited. Lowered fees for the wealthy due to the larger quantum they can invest, and exclusive access to funds not available to the common person. And fees are the single most crucial determinant of success in investing, and to deny fairness of fees or differentiate that based on a person's wealth, is simply unethical.

At Endowus, we sought to align interests by imparting the same fee structures accorded to larger institutional investors, and to give back all of the trailer fees from fund managers. The creation of this unbridled access gives everyone an equal chance of improving their life, no matter how much they start from. And rebating the trailer fees makes us entirely aligned to only improving the performance of the client's investments, rather than pushing funds that dangle incentives to gather assets.

Financial education and improving literacy will help prepare people but the supply side issues remain. It is our responsibility to serve our clients so that they can secure their financial future for themselves and their loved ones.

Evy Wee, Head of Financial Planning & Personal Investing, DBS

Finance is a life skill that enables us to unlock options and attain our dreams. It is also my passion, which was why I chose it as a career. One of the biggest drivers behind this passion for finance was the struggle I went through as my family's sole breadwinner - I had to penny-pinch to make ends meet, and clear my family's debt when we were evicted from our home. Today, I'm able to not only provide for my family, but also pursue my love for cooking and art.

The knowledge and confidence in taking control of one's personal finances is therefore invaluable. This fuels my drive to help others to get better at managing their money, so they can also attain financial freedom and realise their goals and dreams. DBS has also allowed me to bring more people on this journey to financial freedom as we saw the compelling need to help raise financial literacy and provide access to financial advice and tools in Singapore.

It is heartening to see more industry players come together and participate in this movement to help consumers by enhancing their financial planning propositions. That said, our efforts now need to focus on helping each and every individual, whatever their starting circumstances, to understand and distil what is most relevant to them at each specific phase of their financial journey.

Financial decisions are not as "fixed" as most people think they are: they are impacted by multiple factors such as age, employment status, life stage, specific goals and aspirations, and some of these situations can change quicker than we thought possible.

Take the Covid-19 pandemic as an example, most people were caught unawares or unsure about how to set and adjust their monthly cashflow due to impacted salaries, whether they had enough emergency savings or protection coverage, and even how to re-calibrate their investment holdings, home repayment and retirement plans.

Together with the rest of the industry, we can do more to empower the individual, which will go a long way towards resolving the financial and retirement planning challenge we face collectively as a nation.

Tan Siew Lee, Head of Wealth Management Singapore, OCBC

The recent trending Financial Independence, Retire Early (FIRE) movement has caught the eyes of many millennials. This movement is based on a highly frugal lifestyle while saving and investing between 50-80 per cent of one's income to achieve financial freedom early. In layman's terms, it simply means, "suffer now and enjoy later".

This type of mindset is not something new. I have seen peers who have compromised on their lifestyles to accumulate as much wealth as possible, albeit without a clear goal in mind.

Our OCBC Financial Wellness Index 2020 showed that 75 per cent of Singaporeans are not on the right track to achieve their desired retirement lifestyle. One should take a step back and ask: "What is my game plan?"

It is my view that one should save and invest with an end goal in mind. Set a plan of what one would like to achieve within a timeframe and then work towards it through savings and investments. To retire comfortably does not mean sacrificing your current lifestyle and going on an extremely tight budget.

While there is no lack of financial information on the internet nowadays, many new investors still find it daunting to take their first steps. From YouTube to Instagram and even TikTok, people have all kinds of financial advice within reach. No doubt some have pretty good advice, but it's important to always discern every piece of information with a pinch of salt and watch out for financial "hype" that sounds too good to be true.

We find that many customers do not know how to begin their investment journeys and that holding cash provides them a sense of security. Having cash may appear to be safe in the current volatile markets. However, with deposit rates hovering at record low levels, and with rising inflation, I believe this would make it challenging for those relying on cash savings to achieve their financial goals.

My advice is to look beyond savings - there are many investment products, such as unit trusts and ETFs, that allow one to achieve diversification and generate better returns in their investment portfolio.

Jacquelyn Tan, Head of Group Personal Financial Services, UOB

Disciplined money management and planning have always helped me to meet my financial goals and lifestyle needs through the different stages of my life. My life experiences and what matters to me and my loved ones shape my attitude towards financial management and risk.

For example, when I first entered the workforce, I was more focused on saving for a mid-term goal such as buying a home. My financial priority has shifted as a mother. My child's education and future now take precedence.

Retirement planning is also a priority so that I do not become a financial burden to my child in time to come. My wish is also to provide my child a headstart in life with little financial commitment. I have an established financial plan to help me achieve my short- and long-term financial goals which is reviewed with my adviser annually to ensure that my portfolio remains relevant to my needs and risk appetite.

In Singapore, access to banking and payment services is readily available, underpinned by government initiatives such as MyInfo for easy online account applications as well as a well-connected electronic payments network.

However, I believe there are areas where financial access can be further deepened. Wealth management is one of them because it enables individuals to protect and to grow their wealth. Yet wealth management, which includes insurance and investment, is often perceived to be for those with larger disposable incomes.

A UOB survey conducted in September 2020 found that more than seven in 10 Singaporeans are not investing as much as they should and have surplus savings in their emergency fund. One-third of respondents also said they are not well-prepared to meet their financial goal. Often the reason they shy away from investing is because of a lack of financial confidence as they do not know how and where to start.

At UOB, we created a digital solution, SimpleInvest, to help our customers start their investment journeys. They can invest as little as S$100 into three actively-managed funds suited to their risk appetite and objectives of liquidity, income or growth.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services