Brokers' take: DBS says worst over for listco earnings; Maybank likes Wilmar, ComfortDelGro

Fiona Lam

DeeperDive is a beta AI feature. Refer to full articles for the facts.

DESPITE deep cuts in the latest quarterly earnings of Singapore-listed companies and trusts, the worst is now behind them, said DBS Group Research in a market strategy report on Monday.

The second-quarter results season had suffered the full impact of global Covid-19 lockdowns, with a sharp 14.9 per cent FY20 cut in forecast earnings for stocks under DBS's coverage.

"Looking beyond the ashes of the Q2 earnings slash, we seek opportunities from the list of companies that saw upward earnings revisions or recommendation upgrades," analysts Yeo Kee Yan and Janice Chua said. These are companies that have emerged positively from the second quarter.

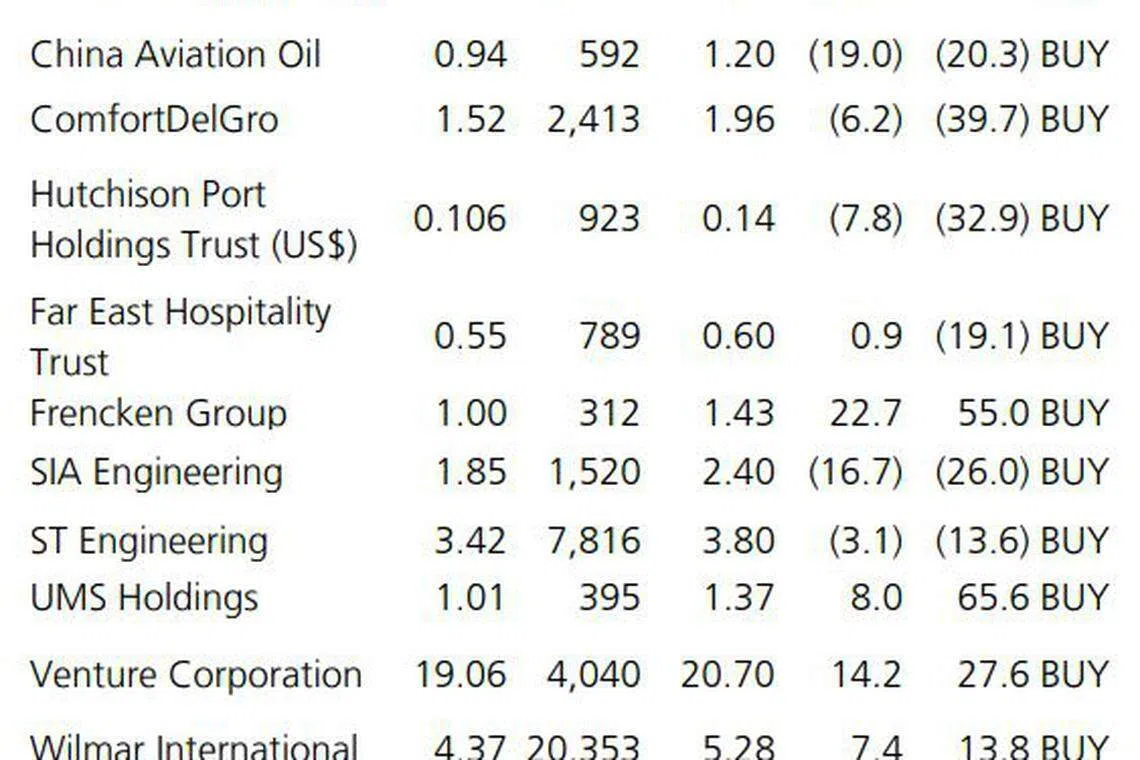

DBS's picks are Hutchison Port Holdings Trust (HPH Trust), ST Engineering, SIA Engineering Co (SIAEC), Wilmar International, UMS and Venture Corp, among counters with either a positive earnings revision of more than 5 per cent or a recommendation upgrade.

In addition, investor interest is likely to pick up for travel or leisure stocks, lifted by progress in Covid-19 vaccine candidates that are under third-phase trials, noted Mr Yeo and Ms Chua.

While the exact timeline for a vaccine to be made widely available is uncertain, DBS thinks the recovery in air travel will be swift once this materialises. The analysts pointed to empirical evidence showing that China's domestic air travel had recovered promptly to near pre-Covid-19 levels in a pre-vaccine environment within five months.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

DBS thus recommends investors look beyond the near term, to accumulate travel and leisure-related stocks in anticipation of the industry possibly recovering next year.

Its picks in the travel and leisure space are SIAEC, China Aviation Oil, ComfortDelGro Corp, Ascott Residence Trust, and Far East Hospitality Trust.

As for manufacturing and trade-related names, DBS noted the strengthening purchasing managers' indices in the US and China, as well as the transportation stocks' strong run-up from the third quarter.

These hint at a broadening manufacturing recovery and a revival in trade activities, said Mr Yeo and Ms Chua.

DBS's picks in these areas are semiconductor components maker UMS Holdings, capital and consumer equipment service provider Frencken Group, and Venture Corp, which provides contract manufacturing services to electronic companies.

DBS also favours HPH Trust, which the research team sees as a proxy to improving global trade activity, offering a yield of about 11 per cent.

Separately, the DBS analysts like Yangzijiang Shipbuilding, given the mainboard-listed Chinese shipbuilder's improving order flow and attractive valuation.

Meanwhile, Maybank Kim Eng has increased its target for the benchmark Straits Times Index (STI) to 2,995, from 2,200 previously, under a new methodology that takes into account fundamentals and massive market liquidity.

The higher STI target implies a 17.9 per cent upside, the brokerage said in a report on Friday, adding that its equity strategy calls for a balance between defence and growth, by weighting towards stocks with structural growth, dividend visibility and diversification.

Maybank KE's top "buy" ideas are Wilmar, Ascendas Reit and ComfortDelGro, as the research team noted that fears of a worst-case scenario seemed to have "overshot lockdown reality, with less earnings misses and higher earnings per share (EPS) upgrades in the Q2 2020 results season".

"Despite the worst of regional lockdowns in Q2, only 29 per cent of combined STI and Maybank KE coverage stocks missed Street expectations," its analysts wrote.

DBS on Monday maintained its year-end target for the STI at 2,850, with technical support at 2,440.

With the steep earnings cut in Q2, the STI now trades between 13.2 times (average) to 13.8 times (+0.5 standard deviation) of its 12-month price-to-earnings (PE) ratio.

Although the index's PE valuation no longer looks attractive, investors will likely look beyond the constituents' FY20 earnings, DBS said.

This is seeing as the worst of earnings have likely passed, with global economies reopening, manufacturing activity recovering and Singapore's shift out of its "circuit breaker" from June, the research team added.

The STI should continue to trade at an above-average PE in the current recession year when earnings forecasts are factoring in the Q2 global lockdowns, while Singapore's GDP is expected to recover going forward, Mr Yeo and Ms Chua said.

The index's price-to-book ratio is attractive "at a mere 0.84 times that is slightly lower than the Global Financial Crisis trough", they added.

"While US markets should pause for a breather in the coming weeks, we think equities will remain in favour amid optimism of vaccine development, broadening recovery and lower-for-longer rates."

In the second quarter of this year, five stocks disappointed for every three stocks that beat expectations.

The main culprits for the Singapore market's Q2 earnings drag were travel and leisure plays such as Genting Singapore and Singapore Airlines, as well as telco Singtel, along with a one-off cut for property developers CapitaLand, UOL and City Developments Limited, DBS said.

In contrast, technology names - UMS, Frencken and Hi-P International - and healthcare counters saw upward earnings revisions.

The STI's forecast earnings per share (EPS) contraction has deepened to 36.1 per cent for FY20. That said, there will be an equally sharp jump of 35.4 per cent for FY21 EPS, boosted by the anticipated 5.5 per cent recovery in gross domestic product on a low-base effect, the DBS analysts wrote.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

Shelving S$5 billion office redevelopment plan proved ‘wise’ as geopolitical risks mount: OCBC chairman

China pips the US if Asean is forced to choose, but analysts warn against reading it like a sports result

Beijing’s calculated silence on the Iran war

Middle East-linked energy supply shocks put Asean Power Grid back in focus