CapitaLand's S$11b buy is big, but will it be beautiful?

Proposed acquisition of Ascendas-Singbridge will see AUM hit S$116 billion across more than 30 countries, up from S$93 billion

Singapore

IT will be big, but would it be beautiful?

CapitaLand's S$11 billion proposed acquisition of Ascendas-Singbridge from Temasek Holdings will place it among the top 10 real estate investment managers globally.

It would not just elevate its global profile significantly but also result in a sizeable expansion and diversification.

Assets under management (AUM) will hit S$116 billion across more than 30 countries from the previous S$93 billion.

The company would add 100 properties in logistics/business parks and data centres in Singapore, and markets like China and India to its portfolio. CapitaLand will also strengthen its presence in several markets like Singapore, where AUM will increase some 40 per cent to S$38.6 billion.

This is also a rejig by state-owned Temasek, which will receive S$6 billion, half in new CapitaLand shares and half in cash. Following the deal, CapitaLand will be 51 per cent owned by Temasek Holdings, up from 40.8 per cent; Temasek Holdings and JTC Corporation jointly own Ascendas-Singbridge.

Market watchers were quick to recognise what was at play.

JLL senior consultant Karamjit Singh said the move consolidates the two groups' geographic exposure, asset types and management expertise, which are fairly complementary.

He said: "In the broad area of business space as an asset class, ASB is largely focused on business parks and warehousing/logistics, while CapitaLand has a concentration around office and retail assets.

"Some lines between these sub-classes would continue to blur as business requirements change over time, which supports the consolidation."

Cushman & Wakefield chief executive Dennis Yeo said the deal was "a good way to allocate and prioritise across different capital markets".

"A hot topic has been the merging of logistics and retail," he said. "But CapitaLand wasn't in logistics. So by putting the two together, you prioritise according to market changes and opportunities and can battle disruption."

It would also mean that CapitaLand and Temasek could become more competitive in the area of township and city development, which has been a focus for Singapore Inc.

"In the early stage of a township it begins with industrial development, then residential and other components like retail or commercial. This would harness all the experiences and track records (of CapitaLand and Ascendas-Singbridge) into one organisation," he said.

"One possibility is that Surbana (Jurong) provides township/city consulting, planning and designing; the new all-property CapitaLand develops, invests and divests (via Reit structure or directly upon maturity)."

Surbana Jurong is also owned by Temasek.

"Given the uncertain external environment, it is important for developers to broaden their revenue base and provide synergy among verticals," said Tan Boon Leong, Knight Frank Singapore executive director and head of industrial.

"With this move, the company becomes much bigger and more complicated. It remains to be seen whether managing such a massive company with a global presence and new asset classes could prove to be successful and realise the potential net asset value growth (NAV) growth," noted Tata Goeyardi, managing director, co-head of equities at SooChow CSSD Capital Markets.

"Being a private company, there's not a lot of transparency on Ascendas-Singbridge to start with. CapitaLand will have to improve its reporting and transparency in order for analysts and investors to better understand and value the bigger entity."

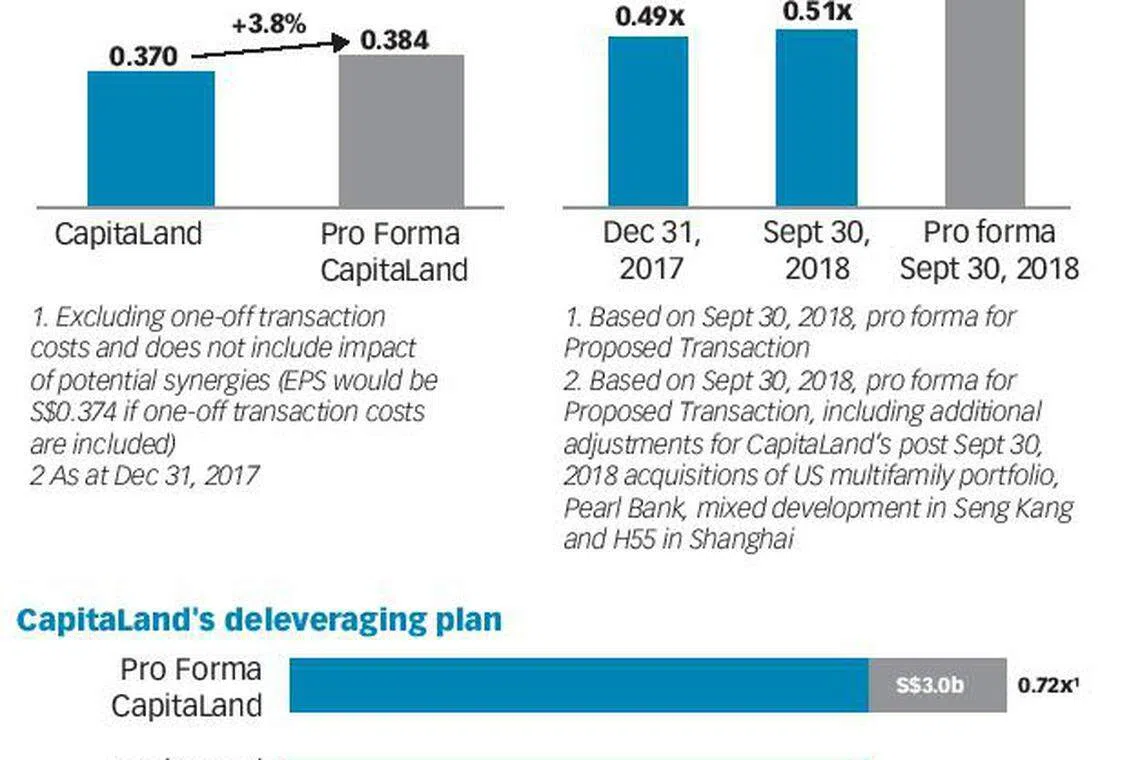

While immediately accretive to earnings per share and return on equity, the transaction is expected to result in a 4 per cent dilution in pro forma net asset value (NAV) per share.

A market watcher, who declined to be named, said: "Managing a huge company with global footprint of this size is a tough ask and it remains to be seen if they have the depth in management for this. The additional potential downside is the inability to be nimble in seizing different market opportunities."

The market had previously speculated that Ascendas-Singbridge might put up a sizeable portfolio of 33 US office properties it acquired last year in an initial public offering (IPO).

With Monday's news, Gabriel Yap, executive chairman of GCP Global, suggested that these office assets could be considered for injection into CapitaLand Commercial Trust, "if they do not get such a great valuation depending on the sentiment for an IPO".

The proposed acquisition will have to be approved by CapitaLand's independent shareholders at an extraordinary general meeting (EGM), expected to be convened by first-half 2019.

READ MORE:

Share with us your feedback on BT's products and services

TRENDING NOW

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Cold Storage moves into convenience retail with On The Go, to replace FairPrice at 58 Esso stations

Three Arrows going after founder Zhu Su’s wife for US$40 million from Dubai property sale

A ‘shadow bank’ hiding in Singapore’s Little India casts light on financial services gap