DBS CEO Tan Su Shan strikes upbeat tone on deposits, wealth growth after strong Q1

The lender declares a dividend of S$0.81 per share, up from S$0.75 the year before

[SINGAPORE] DBS has raised its 2026 deposit growth outlook, citing stronger-than-expected inflows, even as it guides for earnings to hold steady amid an uncertain rate environment.

“We’re seeing higher-than-expected deposit growth,” said chief executive Tan Su Shan, who struck an upbeat tone at the lender’s virtual first-quarter results briefing on Thursday (Apr 30). “Deposit growth should be at the high (to) higher single-digit range.”

At the same time, the bank’s earnings outlook has turned slightly more positive.

DBS chief financial officer Chng Sok Hui said that this quarter’s guidance has turned “more nuanced”, with net profit for FY2026 now expected to come in at around 2025 levels – an improvement from a quarter ago when it had guided for earnings to fall below that.

“It’s actually turned slightly more positive (from) the last guidance,” she noted.

Customer deposits rose 9 per cent year on year to S$629.9 billion in Q1, with more than two-thirds of the increase coming from current accounts and savings accounts (Casa). This outpaced the 4 per cent growth in customer loans to S$453.2 billion.

Excess liquidity that is not deployed into loans will be channelled into high-quality liquid assets, which Tan described as a low-risk, high-return-on-equity option.

“If we can continue on this path of high deposit growth – especially for Casa, (with) high low-cost deposit growth, that’s all upside,” she said.

Loan growth also helped cushion the impact of lower interest rates, as the benchmark Singapore Overnight Rate Average (Sora) more than halved year on year.

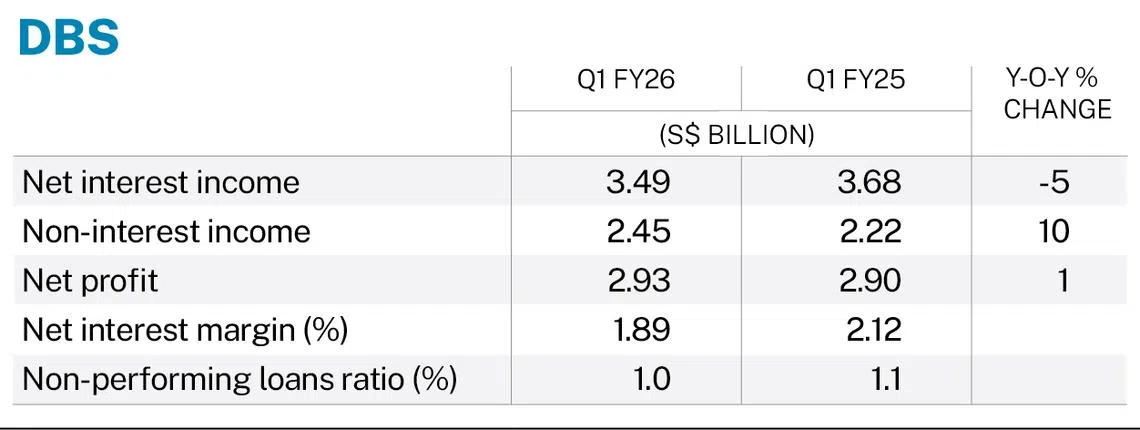

Average Sora stood at 1.07 per cent a year in Q1, down from 2.54 per cent in the same period a year earlier. This contributed to a 5 per cent decline in net interest income to S$3.49 billion for the three months ended Mar 31, though this was offset by a 10.3 per cent rise in non-interest income to S$2.45 billion.

Net fee and commission income climbed 16 per cent to a record S$1.48 billion, driven by wealth management fees, which hit a new high of S$907 million on stronger investment product sales and bancassurance. Transaction services fees also reached a record S$257 million.

Wealth management continued to be a key growth driver, with S$10 billion in net new money flows bringing assets under management to S$492 billion.

Tan said the momentum was broad-based, supported by “very, very strong” bancassurance sales, which are “sticky” in nature.

“Particularly pleasing” was the lender’s Taiwan consumer banking franchise, which delivered strong wealth fee growth in the quarter, she added.

Overall, total income rose 1 per cent to a record S$5.95 billion, while net profit edged up 1 per cent to S$2.93 billion, beating Bloomberg analysts’ expectations of S$2.88 billion.

Rates outlook and guidance

The bank’s outlook has also been shaped by a shift in interest rate expectations.

At its fourth-quarter briefing in February, DBS had pencilled in two US Federal Reserve rate cuts for 2026. It now expects no cuts, a shift that Tan said was actually negative for margins, challenging the assumption that banks automatically benefit from higher rates.

For every basis point of increase in US dollar rates, net interest income for DBS falls by about S$4 million, she noted.

This reflects how banks may be positioned such that rising rates become a headwind – for instance, due to hedging strategies. This means that a higher-for-longer rate environment does not always translate into stronger net interest income.

Earlier on Thursday, the Fed kept rates unchanged at 3.5 to 3.75 per cent.

This is compounded by a lower expected Sora, now guided for 1 per cent a year, compared with 1.25 per cent previously.

“We are not counting (on) Sora to trade higher, but if it does, well, that’s upside for us,” said Tan.

Taken together, DBS expects full-year total income to be at or around 2025 levels, unchanged from prior guidance.

On profitability, Chng said the bank has “a good shot” at “getting close to 2025 levels” for FY2026 net profit.

DBS reported a full-year net profit of S$10.9 billion and total income of S$22.9 billion for FY2025.

Limited exposure to Middle East conflict

On whether DBS has seen client flows out of the Middle East, Tan said that wealth flows remain broad-based across markets and client segments, both onshore and offshore.

It is not as if there would be sudden flows from the Middle East, after the Iran conflict, she noted.

The CEO added that DBS has “very limited” exposure to the ongoing Middle East conflict and holds ample general provision reserves to manage “unexpected scenarios”.

The war, which began on Feb 28, has entered its third month. On Thursday, Brent crude rose above US$120 per barrel, its highest level since 2022.

Stress tests conducted across multiple scenarios – including sustained oil prices above US$120 per barrel and disruptions to energy supplies such as aviation fuel – indicate the bank will be “okay, but we’re watchful”, she added.

“The truth is, the short-term future doesn’t look very clear… politics could go either way,” said Tan “That’s why staying resilient in a time of great stress is so important… (which) means having a strong balance sheet, being nimble and being able to meet the volatilities ahead.”

The lender declared a total dividend of S$0.81 per share for Q1, comprising an ordinary dividend of S$0.66 and a capital return dividend of S$0.15, up from S$0.75 a year earlier.

Shares in DBS rose 3.4 per cent, or S$1.94, to close at S$58.50 on Thursday.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.