Frasers Hospitality Trust posts 24.8% lower H2 DPS; to divest Sydney asset for A$315m

DeeperDive is a beta AI feature. Refer to full articles for the facts.

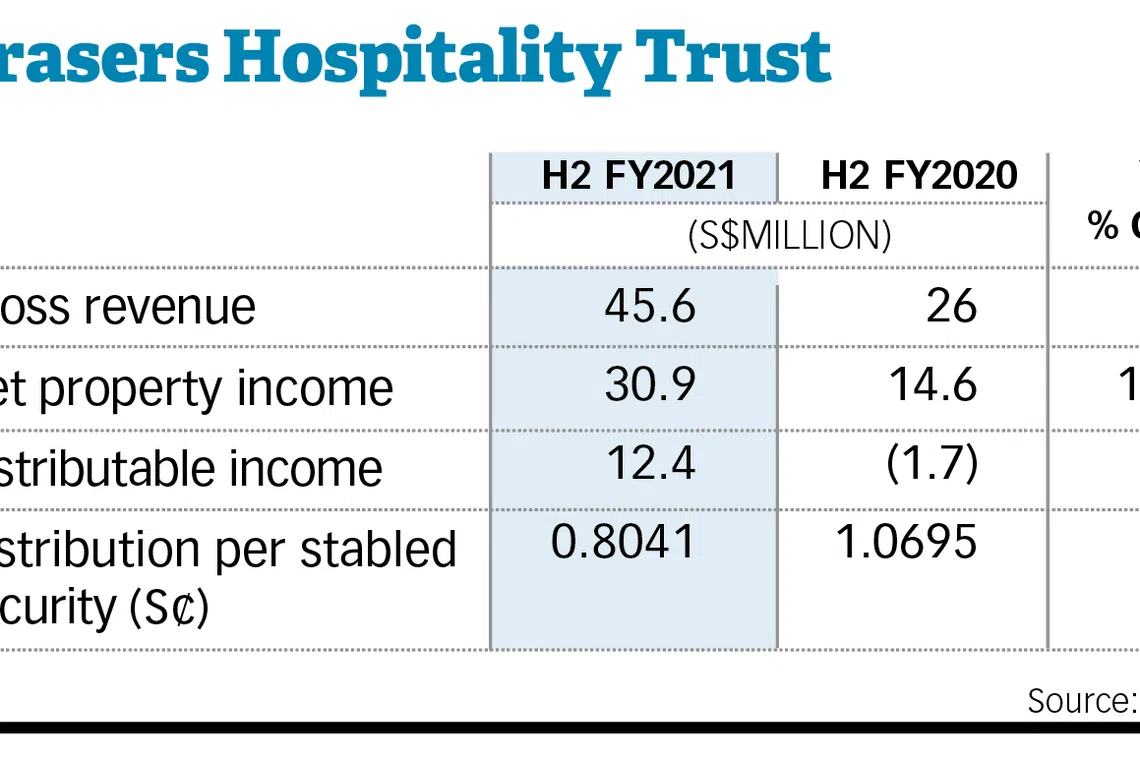

FRASERS Hospitality Trust (FHT) saw its distribution per stapled security (DPS) for the half year ended Sep 30, 2021 fall 24.8 per cent on-year from its H2 FY2020 DPS of S$0.010695, announced managers of the stapled group on Friday (Oct 29).

The decline was due to lower retained distributable income of S$4.3 million in H1 of FY2021, compared to S$22.3 million of distributable income retained in H1 FY2020.

The distribution payment date will be on Dec 29.

Distributable income for H2 FY2021 reversed to S$12.4 million from a S$1.7 million loss registered the previous year.

Net property income (NPI) more than doubled to S$30.9 million compared to that of H2 FY2020 on higher gross revenue and lower operating cost, attributed mainly to cost management.

Gross revenue for the half year grew 75.6 per cent year on year to S$45.6 million with a gradual recovery from the Covid-19 pandemic compared to H2 of FY2020 which marked the peak of the pandemic, said FHT's managers.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

The latest set of results brings FHT's DPS for the full year to S$0.009831, down 29.7 per cent from its FY2020 DPS of S$0.013982.

This includes a retained S$2.1 million or 10 per cent of the distributable income to conserve cash for working capital purposes, said the managers, citing uncertainties arising from the ongoing Covid-19 pandemic.

Managers of the stapled group noted that the impact of Covid-19 began in February 2020 and has not fully abated to date - leading to a comparative decline in performance for FY2021, which was affected for a full 12 months versus the 7 months affected in FY2020.

It added that improvement in H2 performance for the current fiscal year has helped to mitigate the lower gross revenue and NPI for FY2021 which declined 3.4 per cent and 3.7 per cent to S$85.5 million and S$57.6 million, respectively, versus S$88.6 million and S$59.8 million in FY2020.

Due to the lower FY2021 NPI as well as payment of management fees in cash instead of by way of issuance of stapled securities, distributable income for the full year decreased 29.7 per cent to S$21 million as opposed to S$29.9 million in FY2020.

"FY2021 was another challenging year for FHT as the tourism industry continued to be besieged by concerns over new coronavirus variants. Nonetheless, there are encouraging signs of gradual recovery for global travel in recent months, compared to a year ago and we see rising vaccination rates and progressive easing of border restrictions in the countries where we are operating. In the second half of FY2021, all country portfolios' gross operating revenue saw better year-on-year performance," noted Eu Chin Fen, chief executive of the managers.

As governments gradually reopen their economies, Eu expects a rebound in domestic tourism to benefit FHT's assets in Australia, Japan and the UK - which she notes to have sizeable domestic tourism markets.

"Our teams in these markets are preparing for the wider recovery when it comes," said Eu.

She added: "Although the risk from a resurgence in Covid-19 infections remains a threat to the industry, we believe FHT is well placed to capture the upside when the market recovers, with its portfolio of quality assets."

Separately on Oct 29, the managers announced it was acquiring a freehold reversionary interest together with a subsidiary of the stapled group's sponsor, Frasers Property, in Sofitel Sydney Wentworth for about A$10.6 million (S$10.4 million).

FHT will then divest this amalgamated freehold interest for A$315 million, which the managers estimate will translate to NPI yields of 4.1 per cent and 3.3 per cent for FY2019 and FY2021, respectively. Its managers said FHT's NPI figure for FY2020 was not used as it is not representative, considering the effects of the Covid-19 pandemic.

The sale price represents a 34.3 per cent premium over FHT's total combined purchase price of A$234.6 million, comprising the AS$224 million purchase consideration for acquiring the existing 75-year leasehold interest in Sofitel Sydney Wentworth, and the acquisition purchase price of A$10.6 million.

FHT's managers also noted the A$315 million sale price is 12.1 per cent above the property's independent valuation of A$281 million as at Sep 30, 2021, on a freehold basis.

Net proceeds from the divestment are estimated at A$282.5 million, and FHT's manager is expecting a net gain of about A$24.1 million from the transaction.

The managers intend to use net proceeds to repay debt and for distribution to stapled securityholders as well as to finance general corporate and working capital requirements.

Sofitel Sydney Wentworth is a 5-star, 17-storey hotel located in the central business district of Sydney, Australia.

Comprising 436 guest rooms and suites with a gross floor area of 33,589 square metres, the hotel sits on freehold land and is located about 200 metres away from Martin Place train station.

It is currently operating under the trading under the Sofitel brand as part of the Accor Group, under a hotel management agreement which expires in 2026. The property's master lease is due to expire in 2035.

"Despite the ongoing Covid-19 pandemic, we have achieved an attractive sale price for the asset. Our title re-structuring has enabled the unlocking of a value greater than if Sofitel Sydney Wentworth had been sold as a leasehold property. By doing so, we are unlocking the underlying value of Sofitel Sydney Wentworth at an optimal stage of the property's life cycle and enhancing returns for our stapled securityholders," said Eu.

The counter ended down at S$0.48 or S$0.01 lower on Oct 29 when market closed.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.