MPACT’s Q2 DPU rises to S$0.0201 on higher contributions from Singapore properties

For the half-year ended Sep 30, distribution per unit is lower at 4.02 cents

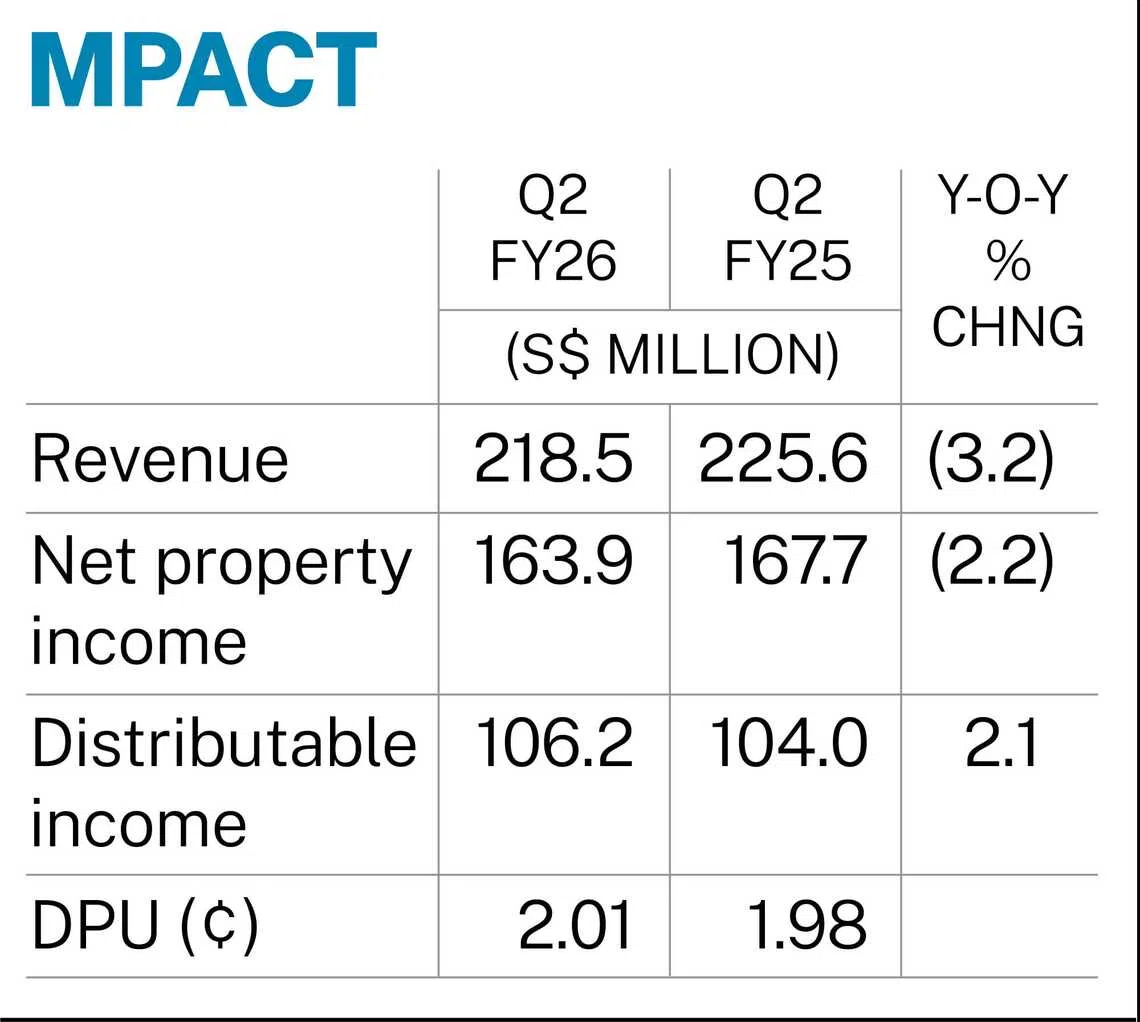

[SINGAPORE] Mapletree Pan Asia Commercial Trust (MPACT) posted a rise in distribution per unit (DPU) to 2.01 Singapore cents for its second quarter ended Sep 30, from 1.98 cents for the same period a year earlier.

The increase was mainly driven by higher contributions from Singapore properties, the trust’s manager said on Wednesday (Oct 22). This, it noted, was despite the absence of income from Mapletree Anson following its divestment in July 2024.

Revenue slipped 3.2 per cent year on year to S$218.5 million from S$225.6 million, largely due to weaker overseas contributions. These were “further dampened” by a stronger Singapore dollar against the Hong Kong dollar and Chinese yuan, as well as the divestment of two properties in Japan.

Net property income (NPI) fell 2.2 per cent to S$163.9 million from S$167.7 million previously.

This was partly offset by a 16.4 per cent drop in finance expenses to S$47.4 million, from S$56.6 million a year earlier, helped by “favourable interest rate conditions”.

Consequently, the amount available for distribution to unitholders in Q2 FY2026 rose 2.1 per cent to S$106.2 million, from S$104 million. The distribution will be paid out on Dec 4.

For the half-year ended Sep 30, DPU came in 1.2 per cent lower at 4.02 cents, compared with 4.07 cents for H1 FY2025. The amount available for distribution fell 0.8 per cent to S$213 million. Revenue declined 5.4 per cent to S$437.1 million, and NPI fell 5 per cent to S$329.9 million.

MPACT’s portfolio comprises 15 properties with a total lettable area of 10.4 million square feet. Singapore remains its “core market”, the manager said, accounting for 57 per cent of total assets under management of S$15.9 billion as at Mar 31.

The manager added that during H1 FY2026, the trust renewed and re-let about 1.4 million sq ft of space, of which 1.1 million sq ft were under leases expiring in FY2026.

Portfolio committed occupancy stood at 88.9 per cent as at Sep 30.

“The Singapore portfolio recorded healthy occupancy levels, while higher commitment levels were also achieved across most other markets, including Greater China despite persistent broader headwinds,” said the manager.

Speaking at a briefing on its financial results on Wednesday evening, Koh Wee Leong, head of investments and asset management of the Reit manager, said the real estate markets in Shanghai and Beijing remain weak, with competition between landlords pushing down rentals.

Occupancy “is not going to improve anytime soon” for its Japan portfolio, added Koh. He said that the occupancy rate will fall by around 15 per cent when the master lease for the Fujitsu Makuhari building ends at the end of the year.

Koh said that the trust will look into divesting its Makuhari assets to reduce the size of its Japan portfolio, but noted that the market is “a little bit weak” at the moment.

On the other hand, the Singapore portfolio continues to “fly” especially now that some asset enhancement works at VivoCity have been completed, said Sharon Lim, chief executive officer of the Reit manager.

On whether there are potential acquisitions in the pipeline, Lim said that the price and asset of the target acquisition will have to be aligned, and that there are no acquisition plans for now.

Units of MPACT closed unchanged at S$1.46 on Wednesday.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

Extra S$300 in CDC Vouchers, U-Save rebates for households as part of S$900 million support package

Singtel explores Nasdaq-SGX dual listing for data centre arm Nxera, local data centre Reit

Singapore banks’ battle for wealth talent goes beyond private bankers

Singapore rolls out S$900 million support package for businesses, households in light of Iran war