OCBC’s new CEO Tan Teck Long pivots to Asean, wealth integration in new growth road map

For 2026, he expects total income to be ‘stable to growing’, in part contributed by double-digit wealth growth

[SINGAPORE] A strategic shift towards Asean, wooing the high net worth to expand OCBC’s wealth pie, and an intensified focus on technology – these are some of the key strategies that the bank’s new group chief executive officer, Tan Teck Long, intends to spearhead.

Tan, who took over from Helen Wong in January, laid out his plans for “the next frontier of growth” during the lender’s fourth-quarter results briefing for the period ended Dec 31 on Wednesday (Feb 25).

“I assume that with a new CEO in town, there will be interest to hear our new strategy,” he quipped.

He described four broad thrusts, the first of which is a “pivot to focus on (the) Asean domestic market”. But he stressed that Greater China – which includes Hong Kong – “remains important” to the lender.

By geography, loans in Singapore, Malaysia and Indonesia made up about 57 per cent of OCBC’s S$341.1 billion in gross loans in the 2025 financial year, up marginally from about 56 per cent in FY2024.

Over the same period, loans in Greater China declined to S$70.9 billion from S$74.5 billion.

“There’s a huge opportunity for us (in Asean),” Tan said. “If there’s any inorganic opportunity in Asean, we will certainly want to take a look,” he added, noting that the lender would consider opportunities in mergers and acquisitions “as and when required”.

Wealth integration

The second push is a “franchise shift”, focused largely on wealth management.

OCBC plans to step up cross-selling through a “whole-of-wealth” approach – particularly through Bank of Singapore (BOS), its private banking arm, and Great Eastern Holdings (GEH), its insurance unit. At the same time, it will reinforce its twin wealth hubs of Singapore and Hong Kong.

SEE ALSO

Tan cited servicing older clients as an example: deposit accounts for seniors through OCBC, succession planning via BOS, and retirement-focused insurance plans through GEH.

The bank will also set up a new wealth management committee comprising Tan, BOS CEO Jason Moo, GEH group CEO Greg Hingston, and OCBC head of global consumer financial services Sunny Quek.

The aim is to ensure a “coordinated tone from the top” so the group’s wealth heads can jointly lead new initiatives, said Tan.

He also outlined several initiatives to further boost the bank’s wealth proposition.

In Malaysia, for instance, OCBC plans to expand its affluent base through GEH’s ecosystem. He pointed out that the base in the insurer’s business there equates to almost half of Singapore’s population.

He also ruled out further acquisition of shares in the insurer, following OCBC’s failed privatisation bid last July. The 93.7 per cent stake that the lender holds in GEH is “good enough” for collaboration, he said.

As part of this wealth integration drive, the bank sharpened its gold strategy last year, with revenue from digital gold sales rising eightfold.

Beyond digital retail access through its app, OCBC is also exploring the option of offering allocated physical gold to institutional and high-net-worth clients, he added.

The wealth push comes as the lender’s non-interest income rose 16 per cent to S$5.46 billion in FY2025 from S$4.72 billion, driven partly by a 22 per cent increase in net fee income to S$2.41 billion.

Wealth management fees jumped 33 per cent, with contributions across all product channels and regions, particularly Singapore and Hong Kong. They accounted for more than half of net fee income.

Insurance income from GEH grew 17 per cent to S$1.07 billion for the full year.

Overall, total income for FY2025 edged up 1 per cent to S$14.61 billion, while full-year net profit slipped 2 per cent to S$7.42 billion on higher taxes.

Tech to power growth, net-zero still on track

The third pillar centres on technology, such as financing the technology supply chain, including data centres.

“We have been very successful in identifying and expanding our coverage of the TMT (technology, media and telecommunications) sector. In the last few years, we have managed to register double-digit growth,” said Tan.

OCBC also intends to further harness technology – artificial intelligence included – internally, with the bank to make investments in this area.

The fourth approach focuses on net-zero, with the continued financing of renewable energy projects and the greening of industries. This includes support for small and medium-sized enterprises.

Even as Tan outlined his plans, he maintained that the bank is still “at the early stage of implementing the new corporate strategy”, and not in a position to disclose formal targets for returns on equity (ROE).

He added, however, that the direction will focus on uplifting ROE over time.

Guidance for 2026

For 2026, Tan expects total income to be “stable to growing”, in part through double-digit wealth growth. This is as net interest income could experience a “slight to moderate” decline, with net interest margins continuing to compress.

The lender is guiding for mid-single-digit loan growth and a cost-to-income ratio in the low to mid-40 per cent range. Credit costs are expected to come in at between 20 and 25 basis points.

OCBC also intends to maintain its 50 per cent ordinary dividend payout ratio, after paying out 60 per cent – inclusive of special dividends – in FY2024 and FY2025.

While the payout ratio may be lower than in the past two years, Tan said the bank’s focus on growing total income through its four pillars could result in higher dividends in absolute terms over time.

In Q4, the lender declared a final dividend of S$0.42 per share, up from S$0.41 in the year-ago period, and is proposing a special dividend of S$0.16 per share.

These bring the total FY2025 dividend to S$0.99 a share.

Q4 performance

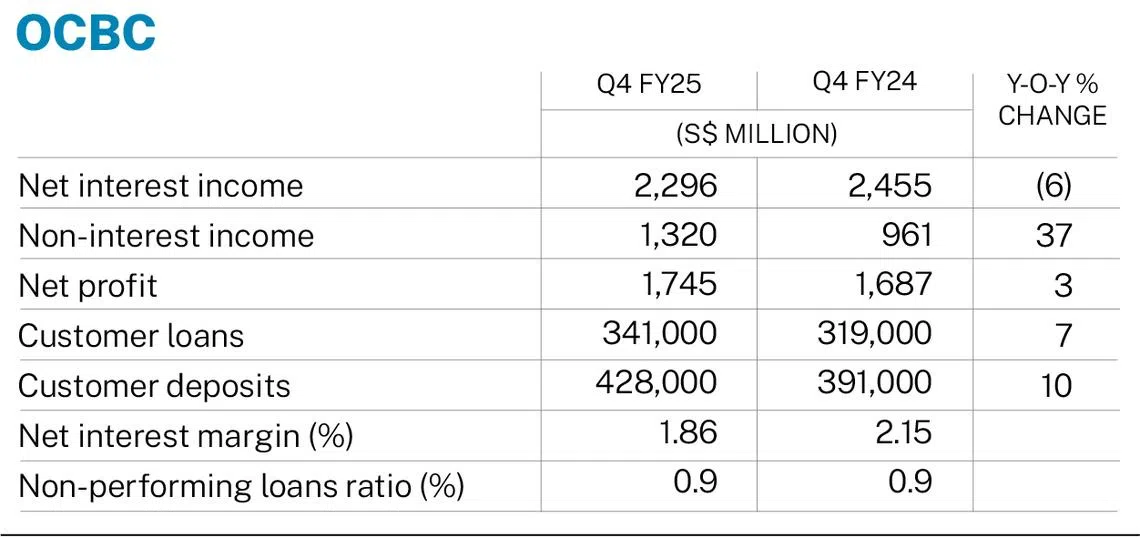

OCBC on Wednesday reported that its Q4 net profit rose 3 per cent to S$1.75 billion – from S$1.69 billion in the year-ago period – on stronger non-interest income.

The result was above the S$1.72 billion consensus estimate in a Bloomberg survey of five analysts.

Net interest income fell 6 per cent in Q4 to S$2.3 billion amid compressed yields, but this was offset by a 37 per cent surge in non-interest income to S$1.32 billion.

Net interest margin narrowed by 29 basis points to 1.86 per cent during the quarter, from 2.15 per cent previously.

The non-performing loan ratio was unchanged at 0.9 per cent, while total allowances declined 4 per cent to S$200 million.

OCBC rounded off the earnings season for Singapore’s three local banks, following DBS on Feb 9 and UOB on Tuesday.

Shares of OCBC finished Wednesday down 0.1 per cent or S$0.03 at S$21.40.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.