Q2 corporate profits dive, but silver lining seen for quarters ahead

Claudia Tan HS

DeeperDive is a beta AI feature. Refer to full articles for the facts.

Singapore

SINGAPORE-LISTED companies turned in a largely weaker set of second-quarter earnings, in line with market expectations that the quarter will bear the brunt of the economic fallout from the Covid-19 pandemic. But the worst appears to be over for several sectors, said analysts.

Of the 134 companies listed on the Singapore Exchange (SGX) that had issued their quarterly scorecards as at August 28, 62 were in the red and 72 were profitable. In the same period last year, 283 companies were in the black and 135 companies incurred losses. The gap in total number of companies reporting was largely due to the lifting of mandatory quarterly reporting.

For the latest quarter, total earnings were down 47.3 per cent to S$2.588 billion from a year earlier, according to data compiled by The Business Times.

There were 59 companies that had better bottomlines, including 15 that swung into profitability. That outnumbered the 40 companies that posted poorer results, including 18 that fell into losses from year-ago profits.

CGS-CIMB research head Lim Siew Khee said that most sectors have "seen their worst" and is expecting an "incrementally positive H2 2020 and beyond".

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

"The exceptions are aviation, telco and capital goods which could still struggle given the changes in travel patterns and stiff competition," she said.

Based on the companies that CGS-CIMB covers, 29 missed the research house's expectations and 11 beat forecasts. Another 24 were in line with expectations.

"We are taking a cautiously optimistic view that the worst of earnings cuts and disappointments are behind us. The negatives of recession, job cuts and lower demand as a result of the Covid-19 pandemic are known," said Ms Lim in a research report.

Meanwhile, Maybank Kim Eng said that fears of a worst-case scenario had painted a much grimmer picture than reality.

Despite the worst of the regional lockdowns in the second quarter of 2020, only 28 per cent of combined Straits Times Index (STI) and Maybank Kim Eng coverage stocks missed Street expectations while an equal number beat expectations.

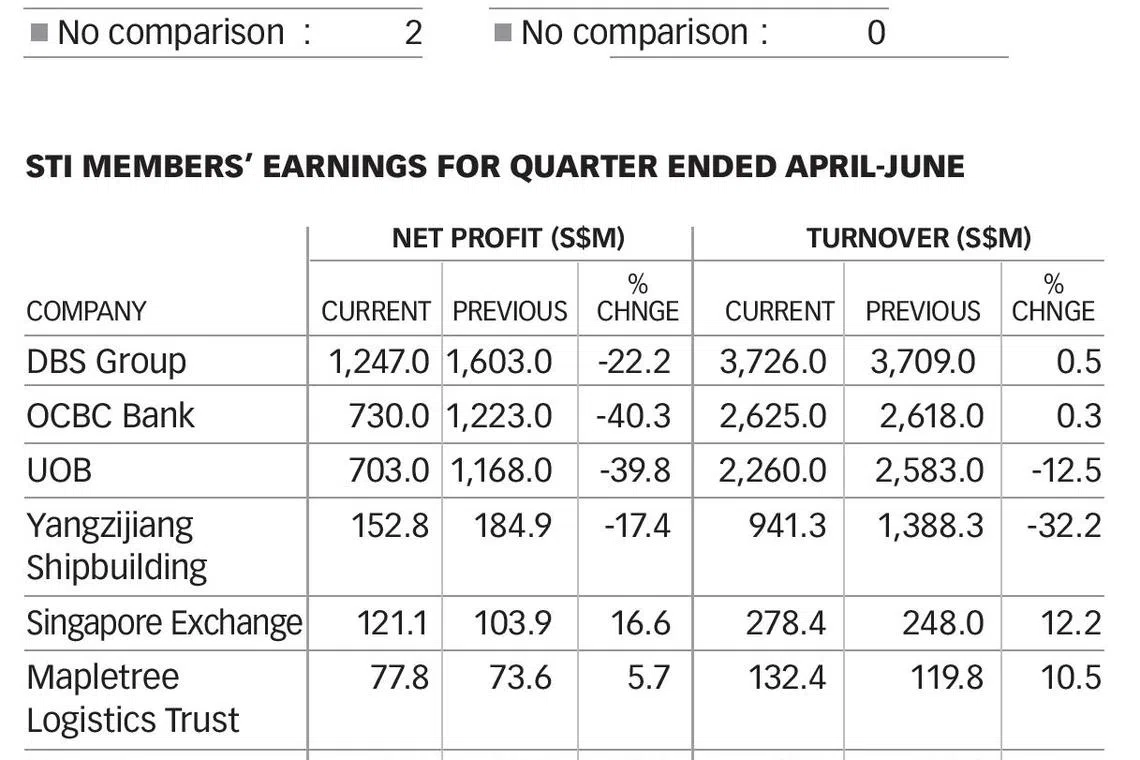

Local lenders and Reits, which together make up the lion's share of the STI, dragged down the total second-quarter income pool for Singapore-listed companies.

"The recent results of Singapore banks largely met lowered expectations with net interest margins (NIMs) pressure continuing to feature as a common thread," said OCBC Investment Research.

All three banks reported a drop in second-quarter net profit.

"Given the expected gradual pace of recovery and a prolonged low rate environment weighing on sector profitability, we think it would not be realistic to expect special dividends this year," said OCBC Investment Research. It sees a possibility of the Monetary Authority of Singapore's dividend restrictions to be extended into FY21.

Earnings were also soft among retail Reits, which registered the full impact of the circuit breaker period. Against this backdrop, net property income (NPI) of retail Reits took a hit while distribution per unit (DPU) was slashed.

BT had reported that S-Reits covered by head of investment research at OCBC Carmen Lee saw distribution per unit (DPU) drop 28 per cent year on year for the first-half period, with hospitality (-62 per cent) bearing the brunt of the impact followed by retail (-45 per cent).

CapitaLand Mall Trust's NPI, for instance, almost halved to S$68.1 million for the quarter, from S$133.2 million in the year-ago period and DPU fell 27.7 per cent to 2.11 Singapore cents.

Industrial Reits on the other hand have proven to be more resilient. Mapletree Industrial Trust and Mapletree Logistics Trust were among those that remained profitable in the face of the pandemic.

Ground handler and caterer Sats and Singapore Airlines were among the worst hit with both firms swinging into losses amid the vanishing demand for global air travel.

This comes as the International Air Transport Association (IATA) estimated that the recovery of global air transport industry may be prolonged and Revenue Passenger Kilometres (RPK) will only recover to pre-Covid-19 levels in 2024.

While companies in sectors such as hospitality and transportation were severely hit, head of research at Phillip Securities Research Paul Chew said that overall performance of firms under the research house's coverage fell within expectations.

The research house is expecting better earnings in the coming quarter as pent-up demand will accelerate revenue for some sectors such as land transport and property developers, said Mr Chew.

CGS-CIMB is also expecting better quarters head, with a 27 per cent year-on-year growth forecast for corporate earnings in FY2021.

READ MORE: Bright spots for investors as virus safety measures ease

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.