Sats posts 31% rise in Q4 profit despite impact of Middle East conflict

Its board proposes a final dividend of S$0.05 a share, up from S$0.035 in the year before

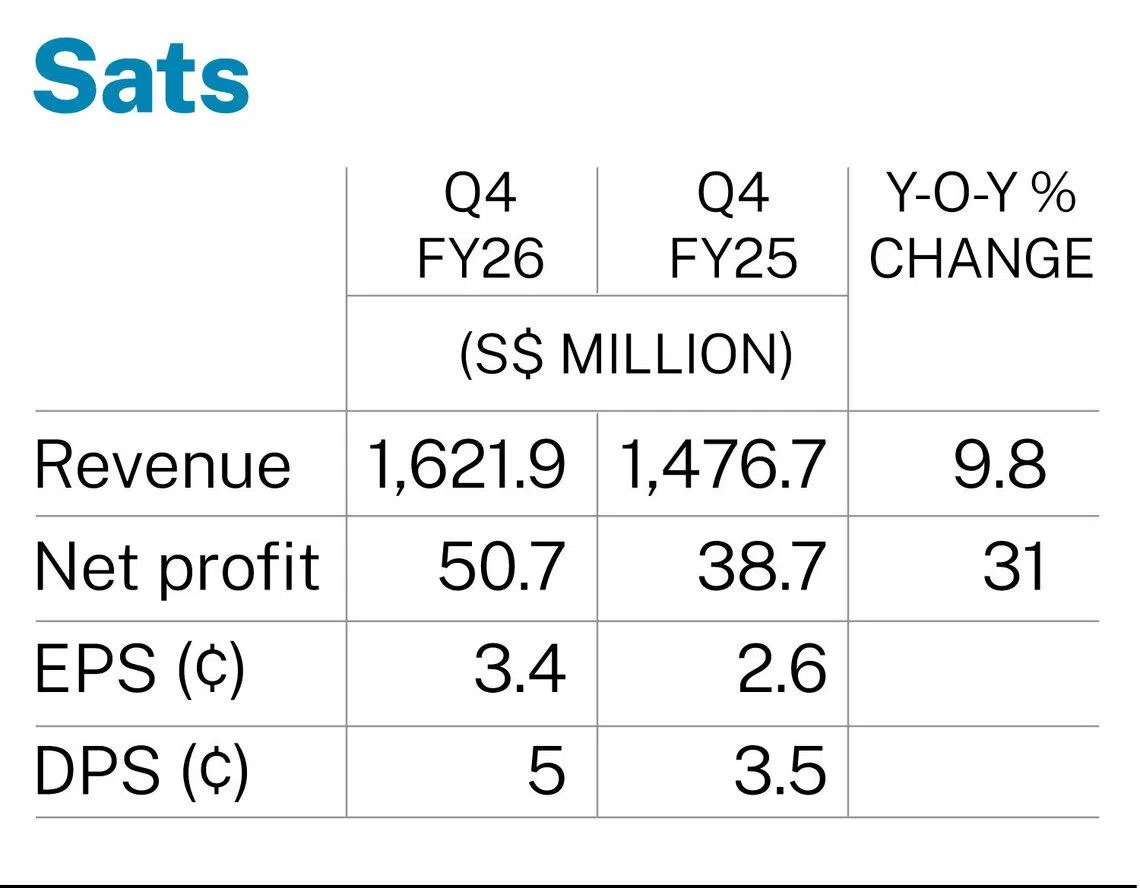

[SINGAPORE] Sats on Monday (May 25) reported a net profit of S$50.7 million for its fourth quarter ended Mar 31, up 31 per cent from S$38.7 million for the corresponding period a year earlier.

This translated to earnings per share (EPS) of S$0.034 for the quarter, from S$0.026 for Q4 FY2025.

Revenue rose 9.8 per cent year on year to S$1.6 billion, from S$1.5 billion previously.

“The Middle East conflict, which escalated in the final month of the quarter, weighed on revenue, costs, operating profit and associates and joint ventures’ earnings,” the group said.

Sats president and chief executive Kerry Mok noted that the war has “weighed on industry performance”.

“We have been working closely with our customers to maintain their cargo flows as routes and lanes shift, drawing on the breadth of our network to serve them wherever they need us.”

Operating profit for Q4 FY2026 edged up 1 per cent to S$109.4 million. However, the group’s operating profit margin narrowed to 6.7 per cent from 7.3 per cent the year before, due in part to ramp-up costs associated with new food facilities.

Its share of earnings from associates and joint ventures rose 4.2 per cent to S$22.2 million, supported by higher business volumes through most of the quarter.

Profit attributable to owners of the company climbed S$12 million to S$50.7 million, with net margin improving from 2.6 to 3.1 per cent. The improvement was partly driven by lower tax expenses in the quarter.

Higher dividend

Sats’ board proposed a final dividend of S$0.05 a share, up from S$0.035 a year earlier.

The group said this reflects its “commitment to delivering increased returns to shareholders as profitability grows”.

Combined with an interim dividend of S$0.02 a share, the full-year dividend will be S$0.07 a share, 40 per cent more than in the preceding year.

The dividend will be paid out on Aug 6, following shareholder approval, with the book closure date set for Jul 24.

For the full year, Sats recorded a revenue of S$6.35 billion, an increase of 9 per cent from FY2025. This was supported by “robust cargo volume growth and contributions from ground handling and food services”, the group said.

By segment, gateway services revenue for the year increased 10.8 per cent to S$4.95 billion, driven by “continued market share gains and cargo volumes”. Sats noted that these outpaced the global growth benchmarks of the International Air Transport Association (Iata).

The gateway services segment comprises Sats’ airport terminal operations, including airfreight and baggage handling, as well as cruise terminal and trucking services.

The group said that air cargo demand remained robust through much of FY2026 before the war’s escalation created a more challenging operating environment.

It noted that the suspension of flights and reduced capacity in the Gulf hubs “disrupted traffic flows among Asia, Europe and the Americas”; elevated input costs put further pressure on operations.

Full-year revenue for the group’s food solutions segment increased 2.9 per cent to S$1.39 billion, supported by “steady demand” amid growing air travel across the Asia-Pacific.

For FY2026, Sats’ operating profit rose 14.2 per cent to S$543.3 million. Operating profit margin improved from 8.2 to 8.6 per cent; the group said this reflected “stronger operating leverage”.

Its share of earnings from associates and joint ventures was stable at S$114.5 million, as underlying volume growth was offset by non-recurring items.

Profit attributable to owners of the company grew 17 per cent to S$285.2 million for FY2026, with net margin improving from 4.2 to 4.5 per cent.

Sats noted that the structural drivers supporting its long-term growth “remain intact”.

“As trade patterns shift and cargo reroutes through alternative lanes, shippers rely on handlers with consistent capabilities across multiple geographies,” it said, adding that its “diversified network” positions it to “support customers from origin to destination”.

“We have demonstrated this by pivoting resources to capture rising European cargo volumes to offset the impact of US tariff measures.”

The group’s network comprises more than 225 stations in 27 countries, and spans cargo, ground handling and specialised services.

Sats said that it is scaling its investment in technology and artificial intelligence in its global network, and using Singapore as an “innovation test bed for next-generation operating models”.

While near-term challenges persist, Mok said that the group’s operating model has consistently proven resilient.

“We enter FY2027 with a broader network, continued infrastructure investment, a strong pipeline of opportunities and confidence in our ability to deliver long-term value for our shareholders.”

Shares of Sats rose 2.7 per cent or S$0.09 to close at S$3.37 on Monday, before the news.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.