From ST Engineering, SIA to shipping: What stands to gain or lose from the Iran conflict?

Investors are differentiating between sectors facing immediate operational headwinds and those finding structural support in the flight to safety

[SINGAPORE] The outbreak of war in Iran has sent immediate shockwaves through global markets, forcing a sharp recalibration of risk across industries as investors weigh the potential for a protracted conflict.

Singapore’s Straits Times Index dropped 2.1 per cent on Monday (Mar 2), broadly tracking regional declines such as Japan’s Nikkei 225 and Hong Kong’s Hang Seng Index, which fell 1.4 and 2.1 per cent, respectively.

However, Oriano Lizza, sales trader at CMC Markets Singapore, said that the sell-off represents a “rational repricing” of specific exposures rather than indiscriminate panic.

Investors are differentiating between sectors facing immediate operational headwinds and those finding structural support in the flight to safety. This divergence was evident on Monday as capital rotated swiftly out of aviation and logistics plays and into defence, energy and gold-linked assets.

Singapore Deputy Prime Minister Gan Kim Yong on Monday warned that the war “could result in an increase in global energy prices, depending on how protracted the conflict is”. This could weigh on the global and Singapore economies, he added.

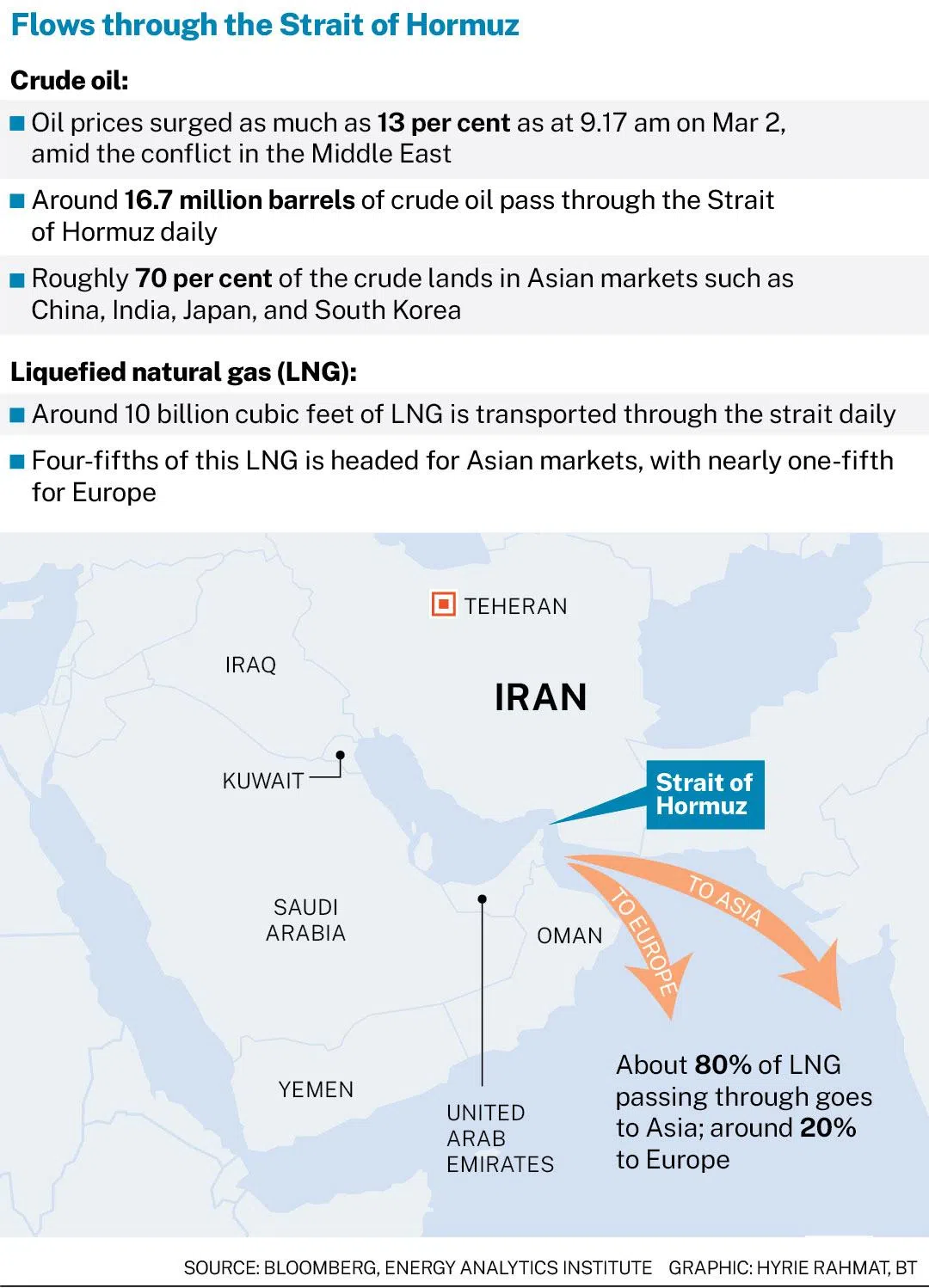

This economic weight is already visible in inflation forecasts. ANZ analysts warned of oil prices rising by US$5 to US$10 a barrel, noting that while Opec+ – the Organization of the Petroleum Exporting Countries and its allies – has pledged to add supply, the physical constraint of shipping lanes remains the primary risk to Asian inflation readings.

Capital inflows to energy, gold and defence

Since the outbreak of war, capital has flowed into sectors that investors believe are likely strategic hedges or direct beneficiaries.

Energy markets felt the most immediate lift. With Iran accounting for about 2 per cent of global oil output and the Strait of Hormuz facilitating 31 per cent of the Middle East’s crude exports, the supply risk is acute.

In Singapore, upstream players saw heavy trading on Monday, with Rex International climbing nearly 18 per cent and RH Petrogas rising more than 27 per cent as investors piled into the oil trade.

This scarcity premium extended to refining. Macquarie analyst Kaushal Ladha noted that while Singapore refiners face short-term cash-flow squeezes from higher inventory costs, players such as Thai Oil are poised for a profit boom as fuel prices rise faster than crude costs.

Defence engineering is another sector that is likely to see gains, with the market already responding on Monday. Shares of ST Engineering rose 2.8 per cent, buoyed by the prospect of rising global defence budgets.

“ST Engineering is looking to double its international sales this year, with the Middle East as its major market,” said PhillipCapital analysts, noting that supply chain diversification has become critical.

CGS International analysts added that the shift towards national self-sufficiency is expanding the company’s addressable market to more than US$11 billion.

Traditional safe havens also surged. Gold investment-related stocks such as CNMC Goldmine jumped nearly 11 per cent, tracking spot gold prices which touched US$5,400 per ounce.

Beyond commodities, Lizza noted that supermarket operator Sheng Siong is expected to outperform, as consumer staples tend to demonstrate resilience during periods of prolonged uncertainty.

Even the shipping sector had pockets of resilience. While transit is disrupted, potential expectations of higher freight rates lifted Yangzijiang Shipbuilding by 2.1 per cent and offshore vessel charterer Nam Cheong by 2.2 per cent.

Logistics, transport face selling pressure

Conversely, sectors reliant on the smooth movement of goods and people face immediate selling pressure.

Global air travel has been heavily disrupted as air strikes keep major Middle Eastern hubs such as Dubai, Abu Dhabi and Doha closed or restricted. Between Feb 28 and Mar 7, 26 Singapore Airlines (SIA) and Scoot flights were cancelled.

SIA shares fell 4.7 per cent on Monday, while Singapore Exchange-listed jet fuel supplier China Aviation Oil dropped 6.9 per cent. Shares of other major Asian carriers including Qantas, EVA Air and Japan Airlines also declined.

“Higher insurance prices and restricted capacity could further strain airlines already facing increased fuel costs and longer routes to detour around conflict zones,” noted Morningstar DBRS analysts.

Shipping lines faced similar dislocation. Major carriers including MSC, AP Moller-Maersk and Hapag-Lloyd have suspended crossings in the Strait of Hormuz, with Hapag-Lloyd announcing a “war risk surcharge” of US$1,500 per 20-foot container.

Compounding the issue, major marine insurers including Gard and NorthStandard have begun cancelling war risk cover for ships in Iranian waters.

Locally, offshore and marine giant Seatrium dropped 2.9 per cent. Lizza attributed the decline to specific investor concerns regarding risks to the company’s project sites in the Middle East.

A Seatrium spokesperson said that the company’s “direct business exposure to the impacted areas is limited” and that it has “no major projects in the Middle East in (its) order book”.

“We are monitoring developments in the Middle East closely and will take appropriate steps as the situation evolves,” added Seatrium.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.