From Tai Sin Electric to Toku: Industrials, tech stocks rule in RHB’s refreshed list of small-cap ‘jewels’

Those listed have compelling valuations, strong balance sheets and growth potential, say analysts

[SINGAPORE] Industrial and technology counters make up more than half of RHB’s latest list of preferred small-cap stocks, as the research house bets on themes tied to artificial intelligence, semiconductors and data centres.

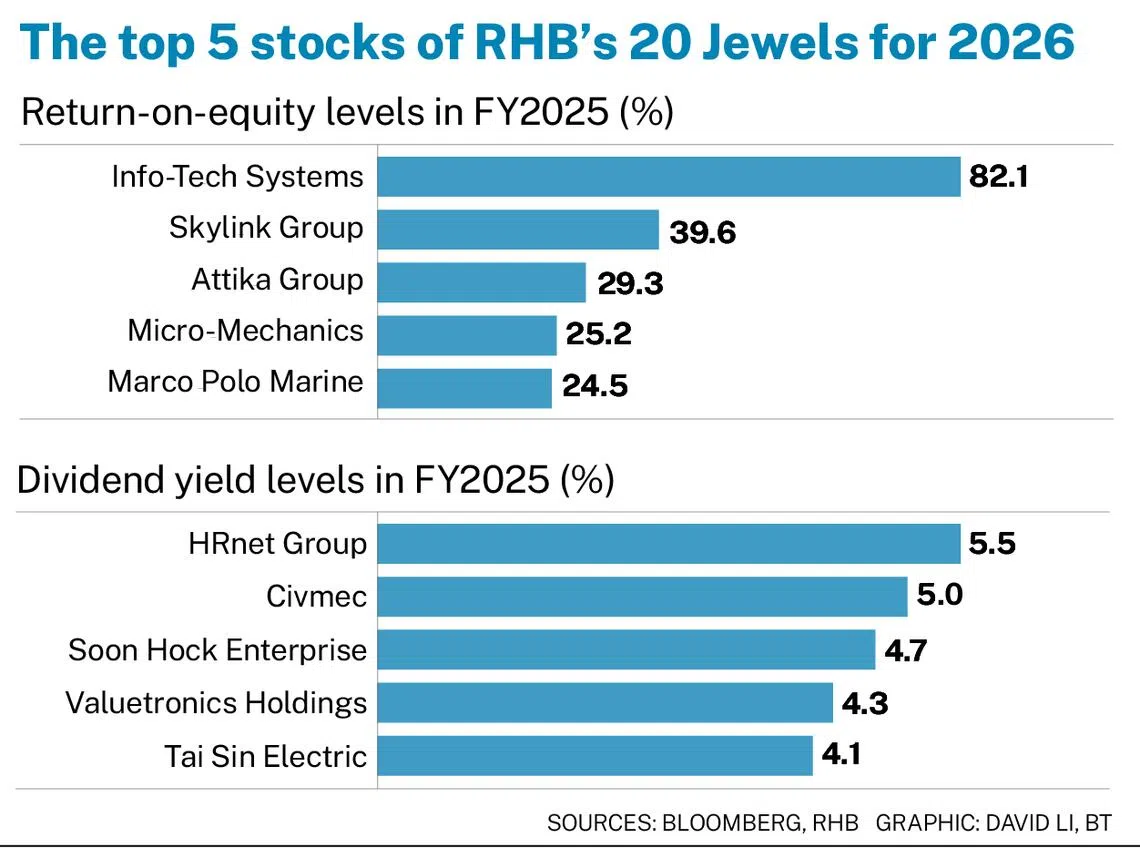

Published on Wednesday (May 13), the 16th edition of RHB’s Singapore Small-Cap Jewels report features 20 Singapore-listed companies with under S$1.5 billion in market capitalisation that the brokerage believes have a “great probability of generating good returns for investors”.

About 60 per cent of the companies featured in this year’s edition were excluded in the previous two editions, reflecting what RHB described as a “deliberate refresh” of its stock selection.

RHB analysts said three broad pillars underpin this year’s list: international and regional growth, the technology value chain, and domestic structural trends. They added that every stock featured in the report exhibits at least one key fundamental characteristic, including compelling valuations, strong balance sheets, cash-generation capabilities, growth potential or event-driven catalysts.

The picks also provide exposure to the property, construction, oil and gas, and healthcare sectors.

The following are some of RHB’s top small-cap picks:

Industrials

Civmec : The engineering company’s order book for H1 FY2026 stood at A$1.4 billion (S$1.2 billion), up 8 per cent year on year from about A$1.3 billion, after it won more tenders in the first half of this year.

RHB analysts noted that Civmec is also “well-positioned” to win large-scale defence and naval shipbuilding contracts under the Henderson Defence Precinct project, a proposed multi-billion dollar investment project by the Australian government in Perth, Australia.

Tai Sin Electric : The electrical manufacturing and solutions group is likely to benefit from domestic construction demand in Singapore. More structural shifts in the data-centre landscape also offer “significant earnings uplift potential” for the group, said the analysts.

The group is also diversifying its revenue streams by acquiring new energy businesses, such as solar equipment distributor BayWare Solar System.

Skylink Holdings : The commercial vehicle leasing company stands to grow from Singapore’s push for greater EV adoption.

The company can bolster its EV fleet through government grants, and reap better rental margins and returns on its assets. Amid high oil prices, Skylink has transitioned 16 of its existing customers to EVs. It also deployed 43 new EV units in Q4 FY2026.

Tech selections

Frencken Group : The integrated technology solutions firm is expected to benefit from the global surge in semiconductor sales. The analysts said: “We expect customer inventory to clear up by H1 this year, followed by a restocking of orders that will see earnings accelerate into H2.” The group also continues to support key customers in Europe, and customers which have moved their production to Asia.

Valuetronics : RHB noted that the company’s earnings are recovering to their pre-Covid-19 levels, backed by a strong net cash balance sheet. Valuetronics’ growth is led by new customers, higher-margin businesses and increased manufacturing capacity, said the analysts. For example, its Vietnam factory can cater to customers that are diversifying their production away from China.

RHB also expects Valuetronics to post better margins as it phases out its low-margin businesses, such as legacy consumer electronic products.

CSE Global : The global systems integrator is expected to benefit from data-centre deployment in Singapore and the US. RHB believes CSE has a strong earnings outlook, backed by Amazon’s US$1.5 billion in project orders.

The company is also expanding its market presence and strengthening its engineering and technology capabilities through acquisitions.

SGX debutantes

Toku : The customer-experience software company, which listed on the Catalist board in January, offers exposure to growth in the global contact solutions market, said RHB.

Toku also plans to grow beyond the Asia-Pacific; it entered Latin America and the Middle East markets in 2025, and four European countries in early 2026.

Coliwoo Holdings : The company, which listed on the SGX in November 2025, is likely to benefit from the Middle East conflict. The potential influx of expatriates and students into Singapore as a result of the conflict could push up rental demand.

Coliwoo’s core net profit for H1 FY2026 stood at S$8.6 million, up 14 per cent year on year. RHB is positive on the group’s recent plan to divest its mature assets and engage in strategic acquisitions.

Info-Tech Systems : The group’s key strength lies in its ability to build and maintain a locally compliant, integrated payroll engine in four markets – Singapore, Malaysia, Hong Kong and India, said the RHB analysts. It is expected to outperform, delivering a higher revenue compound annual growth rate of 10.5 per cent, driven by scalable platform architecture and attractive pricing.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

UOB to sell asset management arm to Allianz Global Investors for S$555 million, sharpen wealth advisory focus

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

1 in 5 fresh graduates from autonomous universities still seeking employment: MOM

Yeoh Pei Xien: YTL’s third-gen scion with a pastor’s heart