What is a protected cell company and how could it benefit businesses?

This allows the parking of risk arrangements under one umbrella, while being legally ring-fenced from one another

[SINGAPORE] The Monetary Authority of Singapore (MAS) has proposed a new corporate structure aimed at making more sophisticated insurance and risk-financing solutions more accessible and cost-effective for companies.

Called a protected cell company (PCC), the structure allows multiple risk arrangements to be housed under one umbrella while being legally ring-fenced from one another.

Public consultation for the framework closes on Aug 7. The PCC Act is targeted to be implemented in 2028.

How does it work?

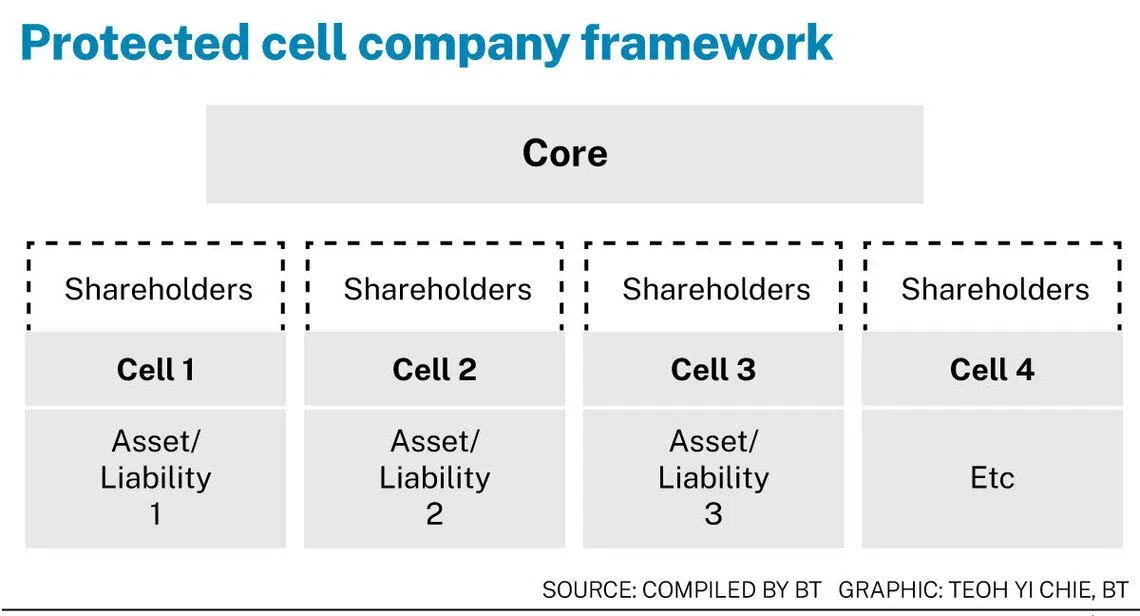

A PCC is made up of a central “core” and multiple protected “cells”.

The core provides centralised governance, management and administrative functions, while each cell holds its own assets and liabilities.

Because these cells are legally ring-fenced from each other, the arrangement lets multiple insurance or risk-transfer arrangements operate under one platform, reducing costs and improving operational efficiency.

This legal separation means that if one programme suffers heavy losses, creditors generally cannot access the assets held in other cells.

The structure was first introduced in the 1990s on the island of Guernsey, a self-governing British Crown Dependency. Since then, more than 40 jurisdictions have adopted some form of cell company structure, and a number have used it to grow their respective insurance industries.

Some jurisdictions with a similar PCC structure include the UK, Bermuda, Malta and Qatar.

SEE ALSO

Observers say PCCs are an established feature of several major captive and alternative risk transfer jurisdictions, and have shown to be a practical and scalable structure.

Why is Singapore introducing PCCs?

MAS expects the proposed framework will support the growth of alternative risk transfer solutions and deepen Singapore’s role as a risk management hub.

This comes as companies globally are seeking to retain greater control and flexibility in risk financing and retention or procure risk coverage to complement traditional insurance capacity, MAS said.

Singapore has had captive insurance legislation for over 40 years, although the number of captive insurers domiciled in Singapore “has not grown much”, said Simon Goh, head of the insurance and reinsurance practice at Rajah & Tann Singapore.

The move reflects growing demand for more sophisticated risk-financing solutions as organisations navigate an increasingly complex and interconnected risk environment, said George Ong, regional director of captive and insurance, global risk consulting at Aon.

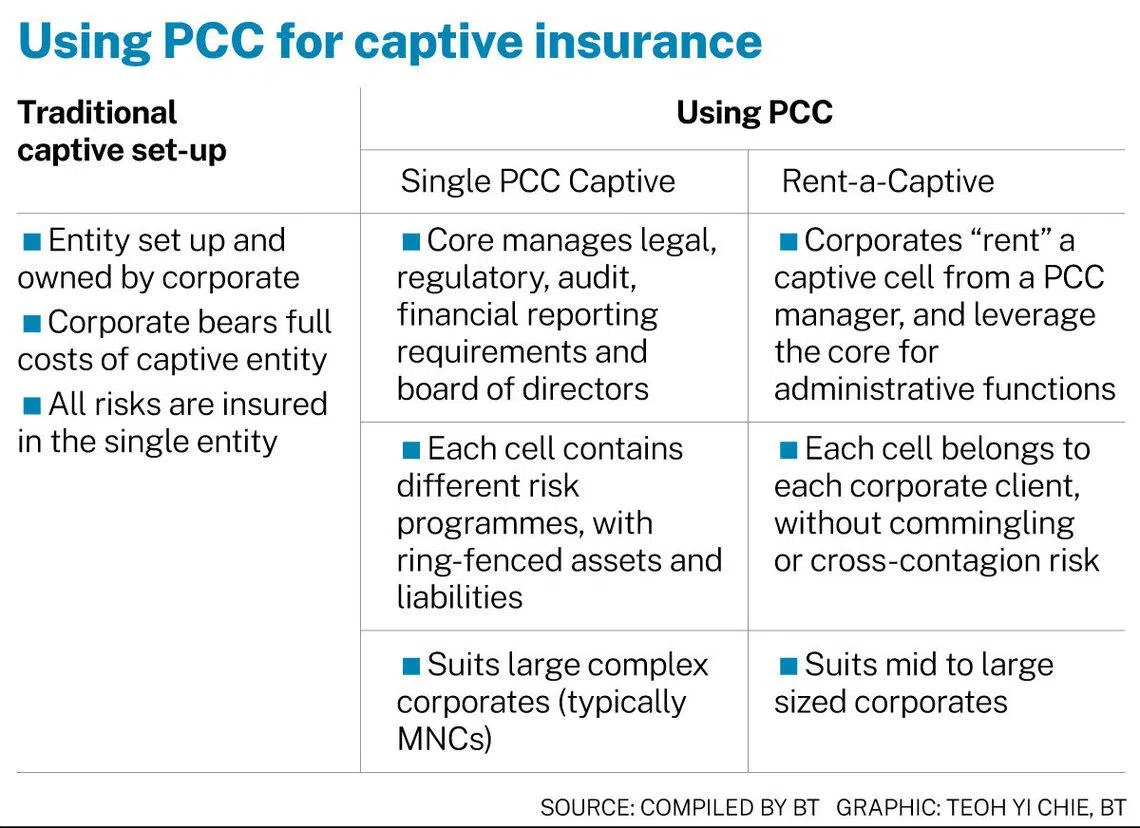

PCC use case 1: Captive insurance

One of the main applications of a PCC is captive insurance.

Captive insurance is a type of self-insurance programme created by a company to manage its risks and premium rate volatility arising from reliance on the commercial insurance market.

Traditionally, establishing a captive insurer requires significant capital and resources, which made the model largely viable only for larger companies.

Under the proposed framework, larger companies could establish dedicated risk programmes in separate cells under a common umbrella that will manage administrative functions. Each cell contains assets and liabilities ring-fenced from one another.

Smaller companies could “rent” a captive cell from a PCC manager to run their own risk programmes, while leveraging the core for administrative functions. Each cell belongs to one corporate client.

This reduces setup and operating costs, increasing accessibility of captive solutions that would otherwise be commercially unviable, particularly for smaller firms.

PCC use case 2: Insurance-linked securities

PCCs could also simplify the issuance of insurance-linked securities (ILS).

ILS are financial instruments that securitise insurance contracts, allowing insurers and reinsurers to transfer specific risks, such as catastrophe risks, to the capital markets.

Insurers can also issue ILS through separate cells within a PCC structure, without the need to establish a new special-purpose vehicle for each transaction.

This enables faster execution, lowers issuance costs, and makes smaller or more bespoke transactions more viable.

PCC use case 3: Sovereign risk pools

The framework could also support insurance facilities that pool risks among multiple countries or participants, such as disaster risk financing initiatives.

Sovereign risk pools are typically set up by multiple participating governments to collectively manage risks and secure insurance coverage against catastrophic events such as natural disasters or climate shocks.

A PCC would provide a common legal structure for these arrangements, so that various programmes or participating risks are housed in separate protected cells while sharing central governance and administration.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Wanted: 100 AI specialists, 100 wealth relationship managers at HSBC Singapore

China chipmaker CXMT jumps 472% in debut after US$9.8 billion IPO

Temasek should publicly state its position on the long-rumoured CapitaLand-Mapletree merger