When bigger is better in life insurance (Amended)

Returns filed show bigger players perform better than their smaller peers in average investment returns for par funds by duration

Singapore

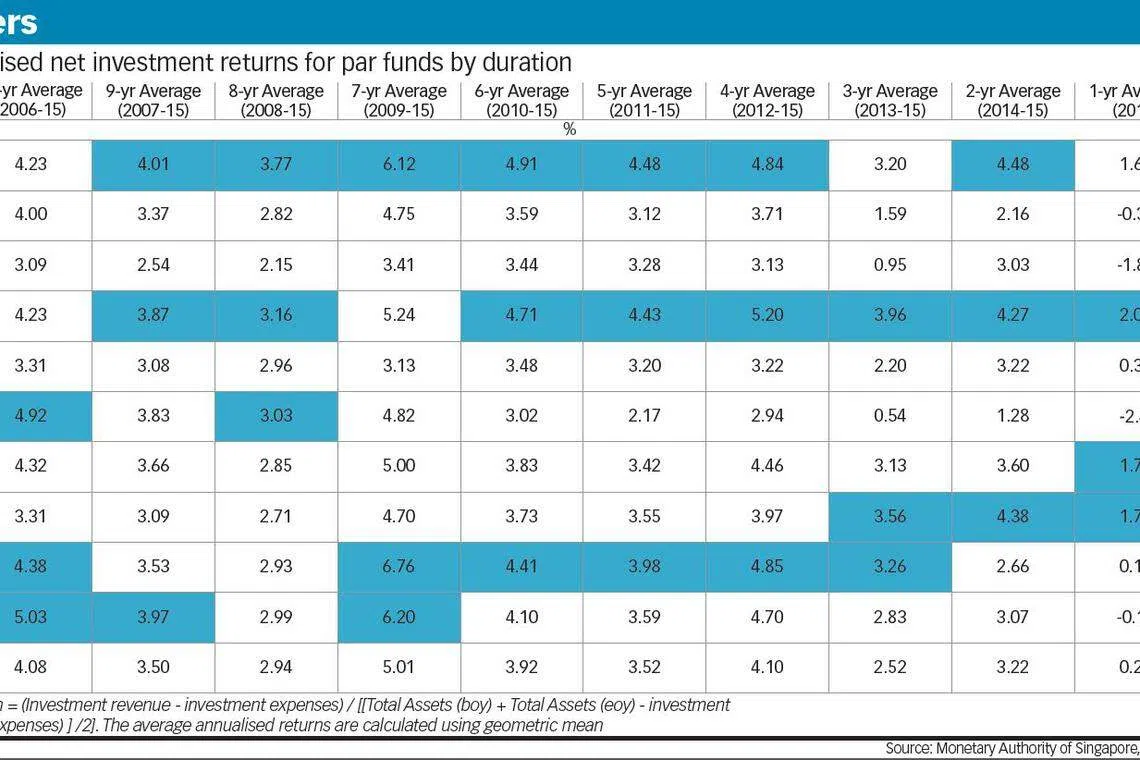

IT seems size does matter when it comes to Singapore's life insurance industry's investment performance for participating (par) funds. Based on the returns filed, the bigger players had better showing in terms of their average investment returns by duration, compared to their smaller peers.

Over a 10-year period from 2006 to 2015, the average annualised net investment returns showed that AIA Singapore, Great Eastern Life and Prudential Singapore had the most number of top quartiles (top 25 per cent) of the 10 major life players in the market.

The calculations, based on a standardised approach, remove differences in formulae used by insurers for their published returns, as well as the anomalous use of the investment returns on selected sub-funds instead of total par funds by some players. Actuarial sources added that it is a comparable reflection of insurers' judgment on how much they allocate to each asset class.

Leading the pack with eight top quartiles over the one-year to 10-year averages was Great Eastern, followed by AIA with seven and Prudential with six.

And the smaller players - AXA Singapore and HSBC Insurance Singapore - paled in comparison.

When contacted, AXA said while it is becoming increasingly challenging to generate higher returns under the prevailing low-growth environment, it is "actively reviewing the investment performance of the par fund, challenging our investment and asset managers to help achieve higher returns".

"We will continue to review and adapt our investment strategies to ensure returns to our policyholders remain sustainable amid an uncertain global economic climate," it added.

Ian Martin, chief executive of HSBC Insurance Singapore, said: "Despite volatile financial market conditions and the prolonged low interest rate environment, HSBC Insurance has maintained a largely consistent rate of investment returns over the past decade, as well as sustaining the 2015 guaranteed bonus rates for our policyholders. In fact, on a risk-adjusted basis, our investment returns and guaranteed benefits have shown to be among the highest in the industry."

Insurers which offer whole life or endowment plans usually direct the premiums collected into a common pool known as par funds. They invest the funds and the investment yields are then distributed to par policyholders in the form of non-guaranteed bonuses.

The level of non-guaranteed bonuses declared by the insurers depends on the value of the assets backing the policies, which in turn relies primarily on investment performance. The level of expenses incurred or allocated to the par fund, as well as the amounts paid out to meet death or sickness claims, are also factors, but typically to a lesser extent, industry sources said, adding that those who do not meet their long-term investment yield targets might be closer to cutting non-guaranteed bonuses in future.

Given the long-term nature of par funds, market sources noted that the average returns calculated over a longer period are more meaningful.

They also pointed out that in the past, the smaller insurers' investment performances were better as a smaller-size fund is nimble and can do stock pickings to beat the market. Once the fund size gets too big, it is harder to do so. Currently, the two projected investment rates of returns shown in the benefit illustration of par products are 3.25 and 4.75 per cent per annum. Of all the industry averages by duration (see table), only six of the 10 were higher than the 3.25 per cent projection but only the seven-year average was higher than the 4.75 per cent.

Against these two projections set by the Life Insurance Association Singapore (LIA Singapore), AIA's and Great Eastern's investments consistently outperformed industry average.

On this, a Great Eastern spokeswoman said the insurer adopts a top-down investment outlook that balances risks and returns via a diversified multi-assets portfolio. "Given the current macroeconomic environment, we expect markets to remain volatile. However, periods of market volatility will likely present opportunities for our tactical asset allocation."

Manulife Singapore, whose new business market share has grown aggressively this year to be among the top three here following its bancassurance tie-up with DBS Bank, recorded strong showing for the longer-term averages. But it also had the weakest investment performance for the one-year to six-year averages.

Said Manulife: "Our investment strategy in recent years had been Singapore-focused and recent returns were impacted due to the underperformance of the Singapore equity market in the last few years. In particular, the Straits Times Index fell by about 15 per cent in 2015, ending the year as one of the worst-performing stock markets in Asia."

It added that it is committed to "maximising our long-term returns and are reviewing our investment strategy regularly to consider both local and overseas investments".

In Singapore, par products account for more than 50 per cent of new business sales.

Wen Research, the firm that compiled the data, said: "Insurers must achieve good investment returns for their par funds consistently in order to deliver the projected returns promised to their par policyholders in the long run. However, high returns may not necessarily translate into high bonus rates for par policyholders and insurers are not required to publicly disclose their bonus distribution methodology."

Amendment note: In an earlier table, under the 1-year column, Manulife's investment returns was stated as 2.40%. It should be -2.40%. The current table has been edited to reflect this.

Share with us your feedback on BT's products and services

TRENDING NOW

Hong Leong, GuocoLand JV sole bidder for condo plot on former Keppel Club site

Nvidia will soon face a chip limit, warns Huawei’s top scientist

Yeoh Pei Xien: YTL’s third-gen scion with a pastor’s heart

Lower consent hurdle among changes proposed for en bloc sales to spur redevelopment, protect minority owners