Why gold did not explode when war began

GOLD’S muted reaction to the Iran war is not a failure of the safe-haven trade; it reflects the first phase of an energy shock, where inflation expectations strengthen the US dollar and delay gold’s rally. In theory, gold should have surged when the Iran war started. Understanding why it did not is more important than the price action itself.

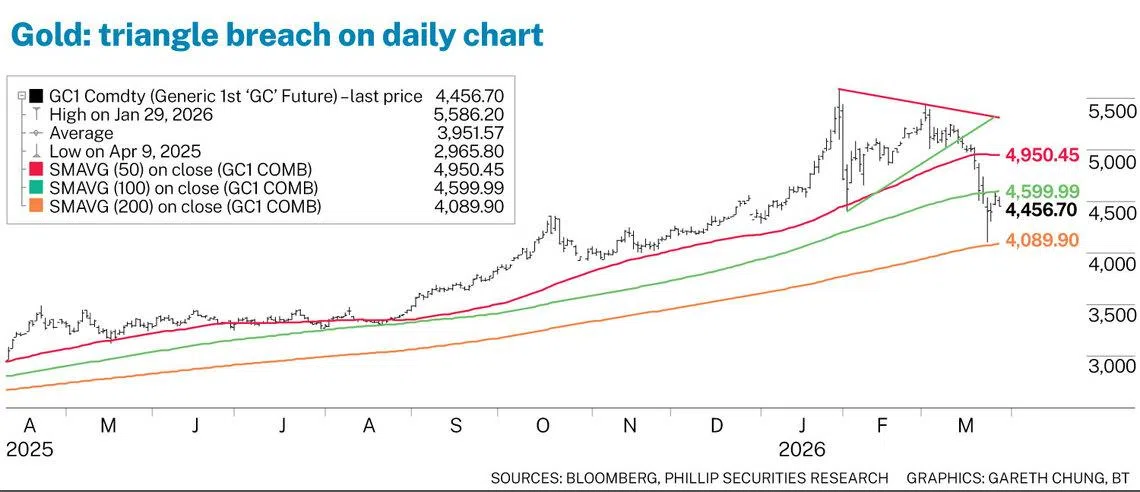

On Feb 28, following US-Israeli strikes on Iran, gold futures spiked to an intraday high of US$5,434. However, by Mar 24, three weeks into the conflict, gold futures dropped to an intraday low of US$4,128.

At the time of writing on Mar 26, gold hovers around the US$4,500 mark, despite significant geopolitical escalation.

In contrast, Brent crude surged to a whopping US$120 a barrel on Mar 8, an almost 100 per cent year to date gain, with soaring jet fuel prices weighing heavily on global transport and travel demand.

The key question for institutional investors is: Why not gold? The answer lies in the US dollar.

When oil rallies beyond US$100 a barrel on the back of war premium, the immediate impact is not increased demand for safe-haven gold but inflation expectations that strengthen the dollar and tighten real yields, conditions under which gold historically underperforms.

Past market trends show that financial markets have proven resilient to setbacks, except during waves of energy shocks, where a two-phase response can be expected.

In the first phase of an inflation shock, gold is being temporarily outbid by the dollar. In the second phase, when economic damage becomes more visible and recession risks rise, the dollar weakens, and gold begins to rally.

These two phases have played out in sequence in every major energy-driven geopolitical crisis.

In 1973, the second phase took roughly six months and resulted in a 73 per cent gain in gold prices. During the 2022 Russia-Ukraine war, the cycle was shorter because the conflict was geographically contained, and the Federal Reserve provided a quicker response.

However, gold has already surged 184 per cent over the last three years. In 2026, the relevant question is whether the war’s duration would extend into the second-phase window, and when.

Markets are currently pricing in one to three months of prolonged escalation with material damage to oil infrastructure. And that can sway the projections of gold in a blink. The key variable is the duration of the war and whether it extends long enough to trigger the second phase of the cycle.

Gold Comex futures have breached below the US$4,400 mark and found support at the 200-day moving average (DMA) near US$4,130, reinforcing this as a key long-term technical level. The rebound that followed, triggered by the US hinting at possible “peace negotiations”, lifted gold sharply towards the 100 DMA at US$4,633, which was tested on Mar 25.

As at Mar 26, sideways consolidation between the 100 DMA and 200 DMA appears most probable in the short term, with risks tilted slightly to the downside.

However, the US$4,000 mark presents an attractive zone for staggered long-term accumulation, particularly given the strong support from sustained central bank buying around this level. Gold prices had already registered record highs, above US$5,000, in January this year, well before the war.

Global markets are in turmoil, and we are almost four weeks into “war chaos”. The US has hinted at “peace”, but Israel’s agenda, “regime change”, is still unrealised. What Iran is fighting is an “existential war” and shouldn’t be overlooked.

The narrative has changed from nuclear disarmament to securing tankers’ movement in the Strait of Hormuz. And given the global energy shortages, it will take just a few more weeks before securing oil and gas becomes a nightmare, triggering another battle: inflation.

While the US appears willing to seek an exit from the conflict, the broader geopolitical backdrop remains uncertain, with Israel and Iran likely to continue tensions. Unless markets receive clear confirmation of de-escalation and a full resumption of supply routes through the Strait of Hormuz, caution is expected to prevail.

That said, the bullish long-term outlook could face temporary headwinds if the macro backdrop shifts towards further rate hikes by the Fed, especially in response to a renewed surge in inflation driven by war-related disruptions.

The writer is senior market analyst at Phillip Nova

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services