Singapore banks could see biggest losses on Indonesia loans among regional peers due to climate risks

The study conducted by NUS’s SGFIN, analyses data on the probability of default for carbon-intensive sectors

[SINGAPORE] Among domestic and foreign lenders, Singapore banks could book the highest estimated loss intensity from climate transition risks on their loan portfolios exposed to carbon-intensive sectors in Indonesia.

These were the findings of a study conducted by the National University of Singapore’s Sustainable and Green Finance Institute (SGFIN), which screened the lending patterns of South-east Asia’s largest economy, as well as exposure to both domestic and international banks, including DBS , OCBC and UOB .

The findings were derived by analysing data on the probability of default for carbon-intensive sectors in the country between 2015 and 2025, then increasing the probability of default to capture rare but plausible shock events.

This is known as applying two standard deviations in statistics; the method is often used in bank stress-testing.

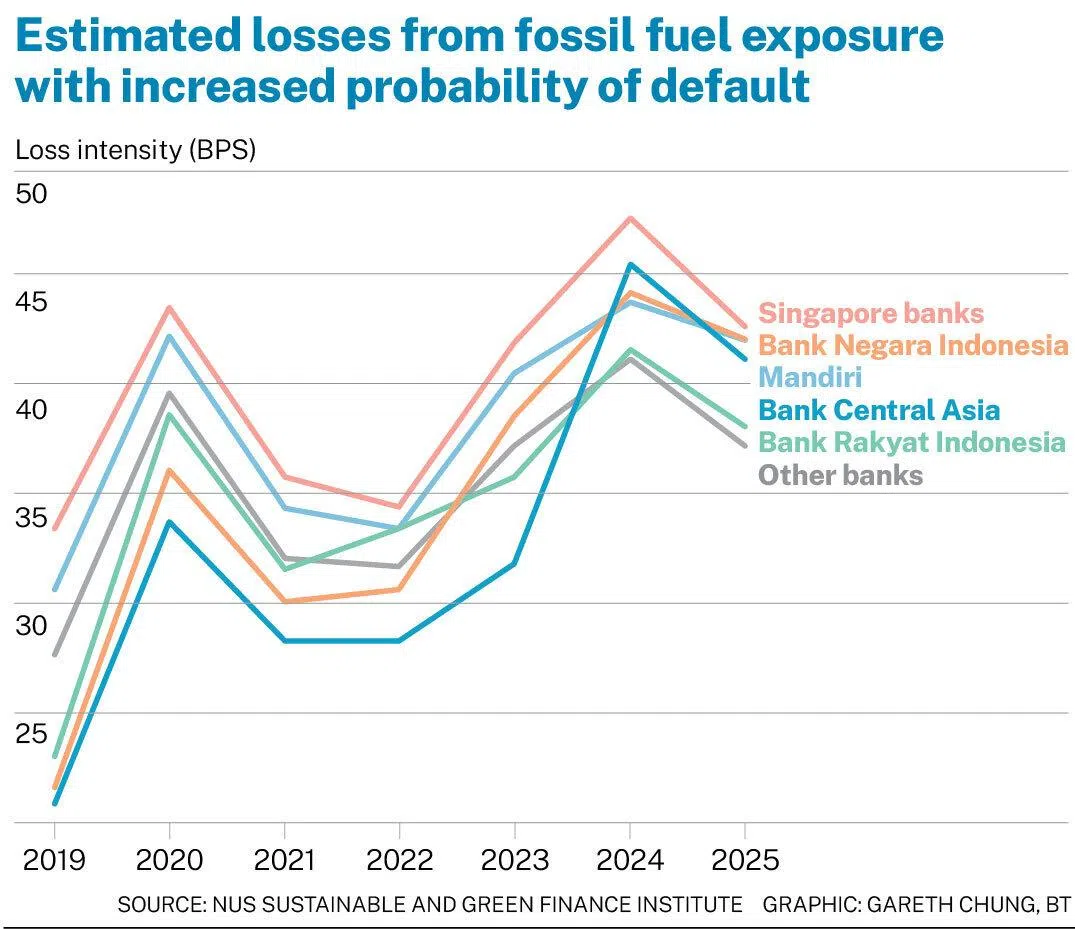

The loss intensity, which refers to the loss per dollar out of the total outstanding loans to these Indonesian companies, was estimated to be around 43 basis points for 2025 for the Singapore banks, according to the report, which was released on Thursday (Mar 12) at a conference organised by SGFIN.

This is between one and two basis points higher than the expected loss intensities for two of Indonesia’s largest domestic banks, Mandiri and Bank Negara Indonesia (BNI).

It is also between five and six basis points higher than that for Bank Rakyat Indonesia (BRI) and other banks assessed in the study.

Across all banks, the 2025 expected loss intensity came in at around 20 basis points based on actual levels of default. That rose to 27 basis points when the probability of default was increased for carbon-intensive sectors.

While Singapore banks displayed moderate expected losses in the baseline scenario over the last 10 years, the additional expected loss was shown to rise over time when tail risk was taken into account.

SEE ALSO

This indicates an increasing contribution of carbon-intensive sector exposures to expected losses as regional project finance and cross-border lending expanded, the report noted.

The assumption behind the study was that sectors with higher exposure to fossil-based input costs, global commodity cycles and operational rigidity tend to exhibit greater volatility in probability of default when faced with market or cost shocks.

As borrowers in carbon-intensive sectors – such as coal, oil and gas, electricity, and metal mining – face materially higher exposures to shifts in technology costs, carbon pricing policies and regulations, export-market requirements and investor risk appetites, the transition risks facing these sectors could lead to additional default risks.

The stress-test results show that transition-related shocks can reshape banks’ credit risk profiles, read the report.

“Historical data cannot predict future outcomes of decarbonisation, but it nonetheless offers useful insights on how banks’ credit risk, and hence expected losses, may evolve as transition policies tighten around the world and portfolio exposures shift in the future,” it added.

By taking into account rare but extreme shock events, the researchers noted that it could be interpreted as a plausible stress point for the banks, illustrating how losses could escalate if transition dynamics move into more adverse territory for Indonesia’s fossil-fuel-dependent economy.

While the report did not directly explain the reason behind Singapore banks potentially incurring a higher loss intensity than others, it noted that the three banks are more exposed to mining-related borrowers, excluding coal.

As at January 2025, DBS, OCBC and UOB made up a total of about 8 per cent of Indonesia’s total corporate loan exposures.

Japanese banks exhibit a higher concentration in the electricity sector. Indonesia’s four largest local banks – Mandiri, BNI, BRI and Bank Central Asia – had portfolios reflecting a relatively balanced distribution across electricity, mining, manufacturing and construction.

Coal financing remains largely concentrated among domestic banks as international banks are gradually reducing their exposure to the fossil fuel.

Physical risks

While Singapore banks are potentially the most affected by transition risks, the report found that their projected losses from flood risks are comparable with those of Indonesian domestic banks, at 0.4 per cent.

Across all banks, borrowers’ asset values are projected to book a weighted-average annual loss of 0.45 per cent due to flooding hazards by 2060.

This is based on a “middle-of-the-road” scenario developed by the United Nations’ Intergovernmental Panel on Climate Change, where temperatures are expected to rise by 3 degrees Celsius by 2100.

However, Singapore banks also exhibit higher dispersions than their large Indonesian peers.

“This indicates that the Singaporean banks’ portfolios tend to include a small number of highly exposed borrowers along with a broader set of relatively less exposed ones,” read the report. “As a result, the underlying loss distribution can be more uneven.”

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.