Singapore’s ESG loan proceeds fall 41.2% in 2025: MAS

Nonethless, the Republic continues to be Asean’s largest market for labelled debt issuance

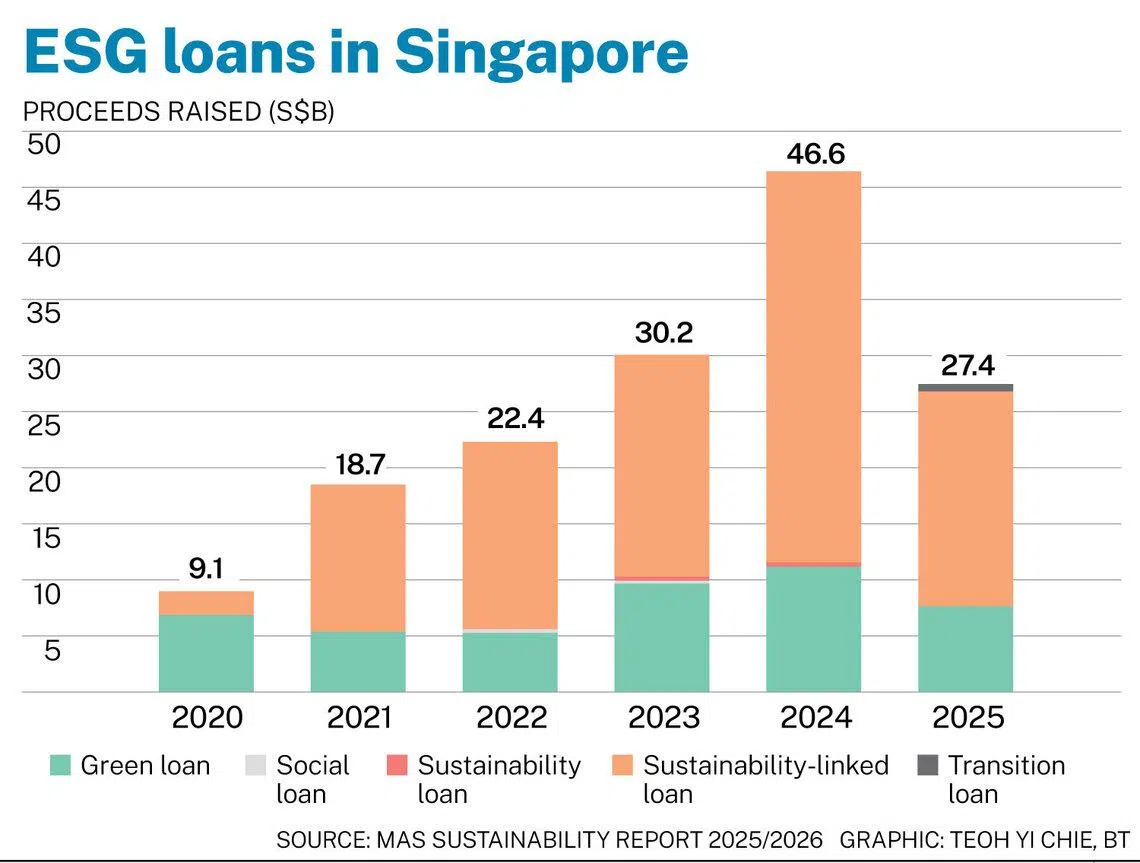

[SINGAPORE] Proceeds from loans tagged with an ESG label issued in Singapore declined 41.2 per cent to S$27.4 billion in 2025, compared with S$46.6 billion in 2024.

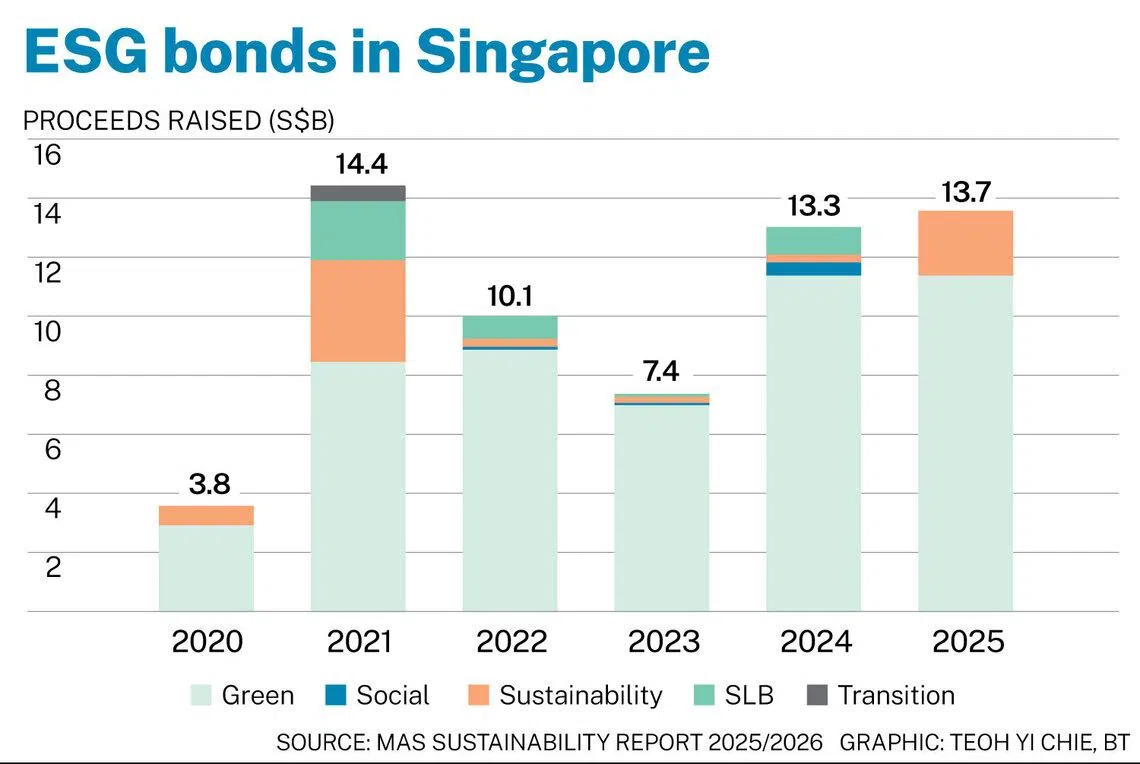

However, there was a slight uptick in ESG bond issuances in the city-state, going up 3 per cent to S$13.7 billion from S$13.3 billion over the same period, the Monetary Authority of Singapore’s (MAS) sustainability report released on Tuesday (Jul 14) indicated.

The report did not elaborate on the drivers behind the muted ESG-labelled debt market last year.

However, observers had previously told The Business Times that markets were hit with heightened risks and volatility due to tariffs imposed by the United States in the first half of 2025.

The pullback was felt beyond Singapore. Across South-east Asia, sustainable finance proceeds remained flat in 2025, compared with the year before, based on data previously provided by LSEG.

Proceeds from ESG bonds came in at US$20.3 billion for the year, marginally higher than US$20.2 billion in 2024, while ESG loans slipped 0.8 per cent year on year to US$43 billion, from US$43.3 billion.

Nonetheless, MAS’ report noted that Singapore continues to be Asean’s largest market for labelled debt issuance, accounting for more than half of the market.

Despite the lower ESG loan volumes, Singapore also saw the first transition-labelled loan brought to market last year.

MAS’ chief sustainability officer Abigail Ng said that demand for sustainable finance in Asia continues to be supported by underlying structural growth in areas such as clean energy and resilient infrastructure.

SEE ALSO

While capital tends to gravitate towards sectors with more established and bankable models, she noted that emerging areas such as adaptation, resilience and newer transition technologies face constraints from higher costs of capital, risk allocation challenges and limited project pipelines.

“The next phase of sustainable finance will depend on strengthening the conditions for capital to be mobilised at scale – through clearer regulatory guidance, more effective risk-sharing structures, and broader financing pathways,” she said.

Investment portfolio

MAS has fully transitioned its climate transition equities portfolio from passive to active management. The central bank had announced last year that it had begun this shift to an active strategy – where portfolio managers pick investments – as it allows them to be nimbler due to shifting geopolitical and climate policy uncertainties.

It is also extending the programme to its corporate bonds’ portfolio.

In FY2023, MAS had set aside about S$8 billion – around 2 per cent of its portfolio at that time – towards its climate transition programme.

A small portion of this allocation, which is from the equities portion of the central bank’s official foreign reserves, had initially gone into companies that are part of two climate indices.

The two indices are an off-the-shelf index and a bespoke product tailored to suit MAS’ requirements.

MAS may eventually consolidate to one long-term climate benchmark, or maintain both depending on implementation insights and scenario analysis.

The shift to an active management of its climate transition portfolio enables MAS to observe how portfolio managers navigate the trade-offs between financial performance and climate objectives.

“This includes having the flexibility to respond to short-term market dislocations, while maintaining alignment with longer-term transition goals,” the report indicated.

Emissions reductions

MAS had previously announced its target of reducing the weighted average carbon intensity of its equities portfolio by up to 50 per cent by the FY2030 from FY2018.

Since then, the carbon intensity of its developed markets equities portfolio has gone down by 52 per cent, while the emerging markets equities portfolio has reduced by 12 per cent.

The broad reduction reflects a structural shift away from carbon-intensive sectors such as energy, materials and utilities sectors towards less carbon-intensive growth sectors such as information technology and communication services, noted MAS.

However, the report stated that year-to-year carbon intensity movements may not follow a smooth path given idiosyncratic events and portfolio decisions by external fund managers in different market cycles.

The carbon intensity of its developed markets’ equities portfolio actually went up to 80 tonnes of carbon dioxide equivalent (tCO2e) for every US$1 million of revenue in FY2025, compared with 65 tCO2e the year before.

This was primarily driven by higher exposure to carbon-intensive sectors, whose valuations rose alongside higher global commodity prices, said MAS.

Nonetheless, the carbon intensity level remained below the benchmark.

This arose from active allocation decisions of external managers and targeted portfolio actions such as the climate transition programme and the exclusion of thermal coal mining and oil sands companies. They collectively tilted the portfolio towards less carbon-intensive companies.

For its emerging markets equities portfolio, the amount of carbon emissions out of US$1 million of revenue fell year on year to 235 tCO2e from 261 tCO2e the previous year.

As MAS started implementing its climate transition programme towards its corporate bonds portfolio last year, the carbon intensity of this investment pool has gone down to 114 tCO2e out of US$1 million in revenue, compared with 129 tCO2e previously.

MAS’ portfolio construction framework, which screens out debt securities with smaller issuance sizes that tend to be in more carbon intensive sectors, also contributed to the lower carbon intensity.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.