Singapore’s projected data centre capacity growth lowest among Asia-Pacific: PwC report

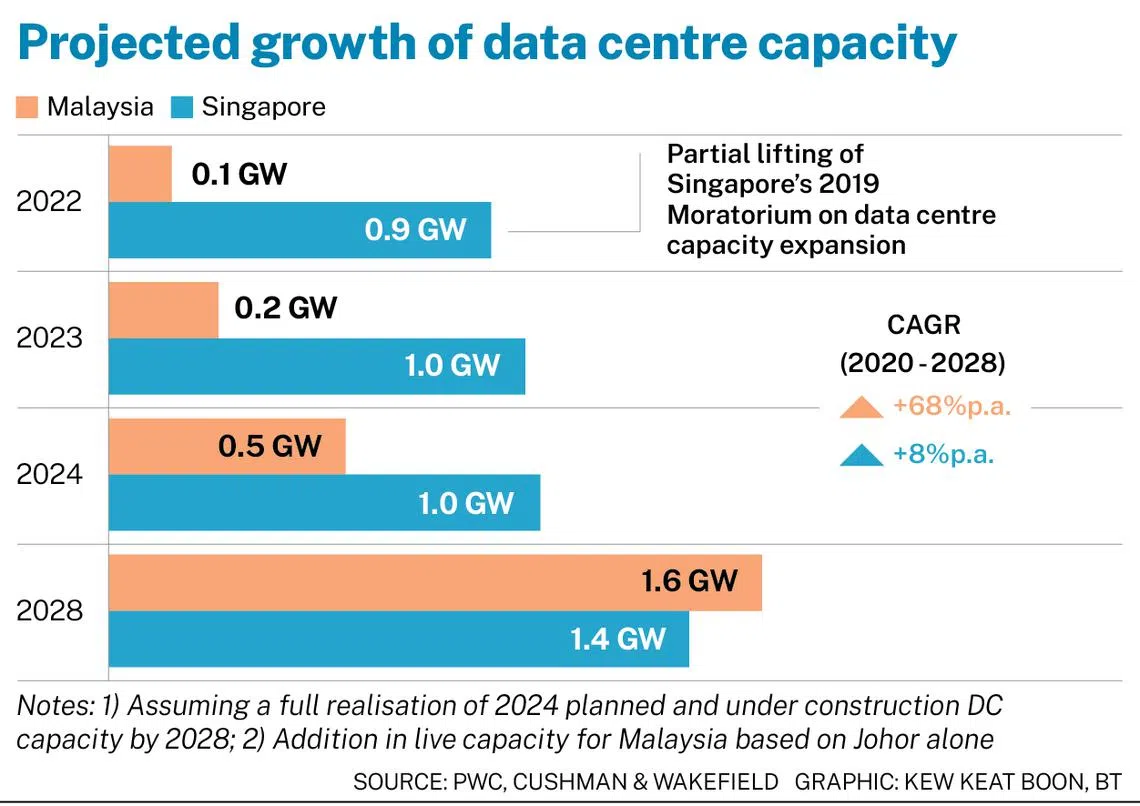

Republic’s data centre capacity is projected to have 8% CAGR between 2024 and 2028

[SINGAPORE] Land limitations, as well as policies that support green data centres in Singapore, have constrained the city-state’s data centre capacity growth, indicated a recent PwC report.

Singapore’s data centre capacity is projected to have an compound annual growth rate (CAGR) of 8 per cent between 2024 and 2028, the lowest rate out of 14 Asia-Pacific markets analysed in the report.

However, it highlighted that the Johor-Singapore Special Economic Zone (SEZ) could potentially be a model for data centre operators looking to set up their assets in dual locations.

While Singapore has limited land and sources of renewable energy, Johor presents a compelling value proposition with more affordable land, lower construction costs and reduced operating expenses.

This sets the stage for a dual-location strategy in which low-latency artificial intelligence (AI) applications can be hosted in Singapore, where robust digital infrastructure supports real-time responsiveness and minimises downtime, stated the report.

Meanwhile, high-latency training workloads can be located in Johor, where energy and space constraints are less severe.

“This allows corporations to conduct high-latency AI training with scale in these neighbouring regions while situating critical, last-mile, low-latency AI inference workloads in Singapore,” stated the report.

Low-latency computing supports AI applications that require near-instantaneous processing and response. Hence, it would be more beneficial for data centres that support these applications to be located closer to data sources for reduced response times and improved performance.

High-latency computing involves teaching a model to identify patterns or perform tasks by processing vast datasets. It is highly computer-intensive, hence, scale and power access become the primary considerations.

SEE ALSO

With strong subsea cable connectivity linking both markets to global hubs, as well as tax incentives and access to upgraded infrastructure being offered for companies establishing data centres in the region, the report noted that “the SEZ has the potential to serve as a model for regional data centre integration – enabling workload specialisation and shared benefits across neighbouring territories”.

Data centres in Asia-Pacific

Across Asia-Pacific, data centre capacity is expected to more than double from 12.2 gigawatts (GW) of live capacity at the end of 2024 to 26.1 GW by 2028, said the report.

The region’s AI-related data centre capacity is expected to grow at a CAGR of 21 per cent from 2.2 GW in 2024 to 4.8 GW in 2028.

Indonesia, Malaysia, India and Japan have emerged as the frontrunners in the report, with a forecasted CAGR of at least 30 per cent over the same period.

However, the report noted that access to energy continues to pose a growing concern for many territories.

“The energy demands of AI workloads are pushing data centre operators to seek locations with stable, high-capacity electricity supply and low risk of disruption. Energy costs and sustainability targets are also front of mind – prompting operators to favour areas with affordable electricity and access to renewable sources,” stated the report.

It also added that a more fundamental issue is access to the energy grid itself, as grid readiness will determine whether operators can reliably tap on imported energy easily.

Renewable energy alone is may not be enough sufficient to power the energy consumption demands of data centres.

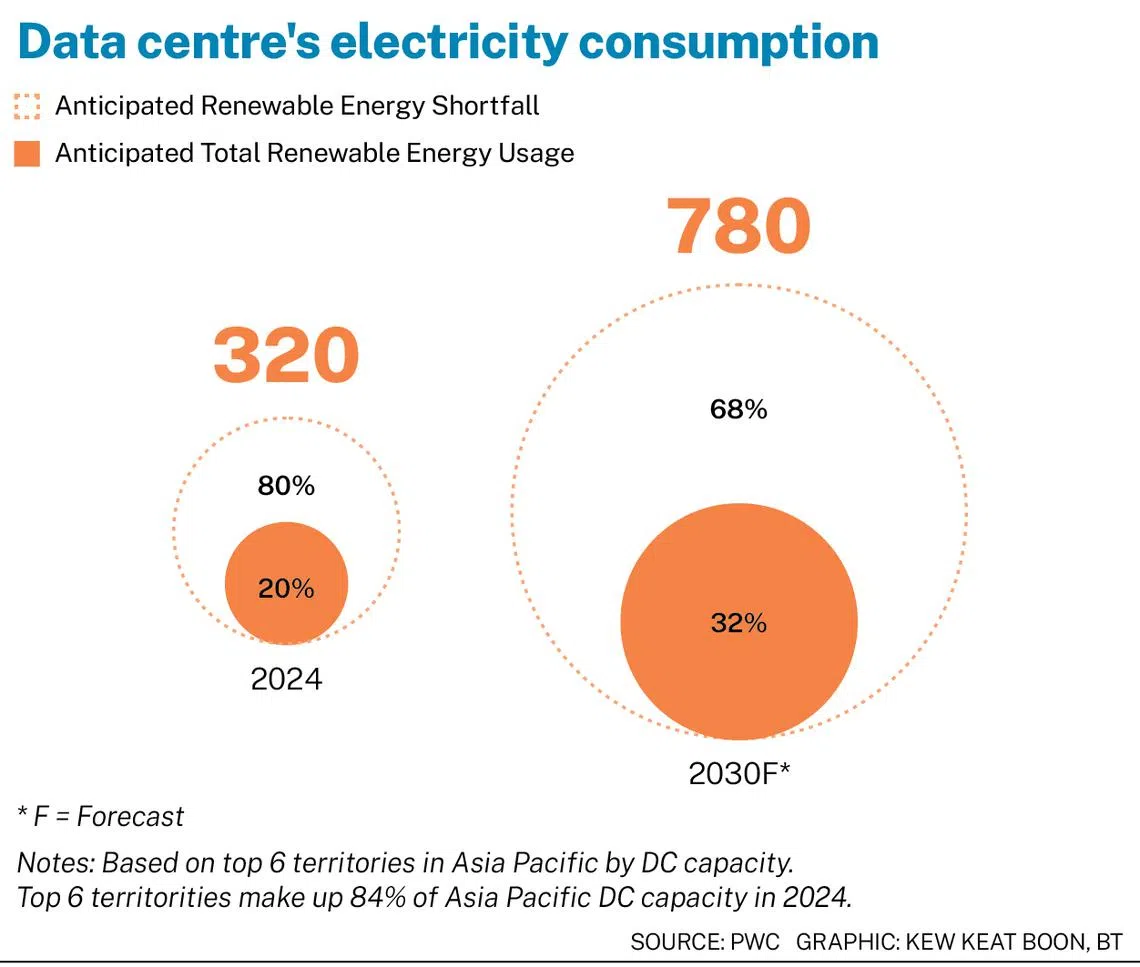

The electricity consumption of the top six Asia-Pacific territories by data centre capacity – China, Japan, Australia, India, Singapore and South Korea – is expected to grow by 16 per cent annually until 2030, reaching between 750 and 800 terawatt-hour (TWh).

Renewable energy generation capacity, however, is expected to increase at a lower pace of 13 per cent annually.

PwC analysis showed that the current renewable energy gap of between 200 and 300 TWh may widen to more than 500 TWh.

“So, while renewable energy remains central to powering data centres more sustainably, it’s unlikely to be enough to meet the region’s fast-growing energy demands alone. To close the widening gap, data centre operators are exploring alternative energy sources – including hydrogen, ammonia and nuclear power – while also investing in efficiency improvements and carbon offset strategies,” said the report.

Currently, data centre operators are purchasing carbon offsets or renewable energy certificates (REC) to meet sustainability goals.

However, the report said that operators are under growing pressure to contribute directly to emissions reduction, and not just offset them.

“While they may serve as a quick solution, they cannot be a permanent solution if data centres are to truly decarbonise,” said the report.

While having access to renewable energy is increasingly important for data centre operators, South-east Asia still lags in renewable energy adoption.

The shift from fossil fuel dependency to renewables in South-east Asia will require substantial investment in infrastructure. However, there is hesitation among governments in the region to increase public debt for infrastructure development, which often limits the speed of transition.

“Private investors must carefully navigate regulatory policies, political dynamics and licensing requirements when investing in or establishing renewable energy facilities. Players must adopt a localised perspective when evaluating the feasibility of renewable energy investments in different territories,” added the report.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.