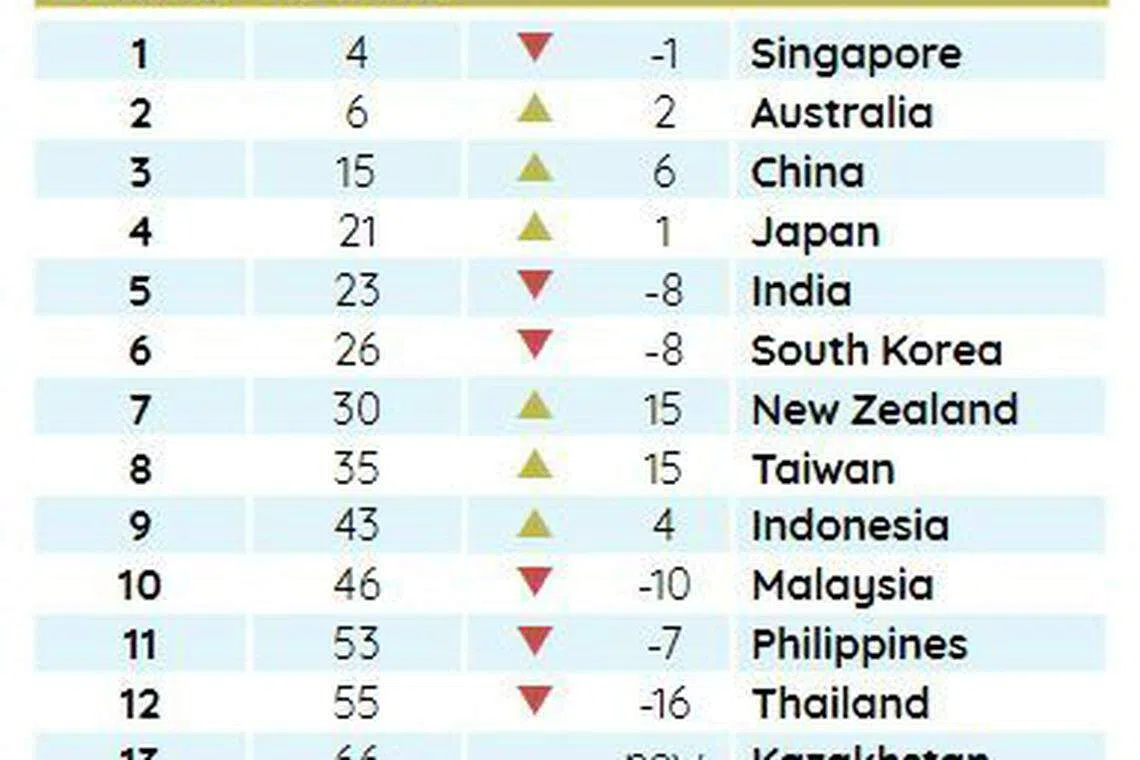

Singapore slips to fourth place in Global Fintech Rankings but retains top spot in Asia-Pacific

SINGAPORE has fallen one rung to fourth place in this year's Global Fintech Rankings. And while it still takes the top spot among countries in the Asia-Pacific, the Republic faces stiff competition from countries like Australia, China and Japan, which have moved up the leaderboard this year.

The second annual index, produced by fintech analytics provider findexable in partnership with cloud banking platform Mambu, looks at over 80 countries, 264 cities, and over 11,000 fintechs. The index scores each location for the quantity and quality of privately-owned fintech companies, as well as the local business environment.

When it comes to ranking of cities, Singapore fell six places to take the 10th spot. Eight of the top 10 cities have remained the same as in last year's inaugural index, while the top three - San Francisco, London and New York - are in the same order. Cities that have surpassed Singapore this year include Sao Paulo, Tel Aviv, Berlin and Boston.

Other cities in South-east Asian countries, like Jakarta, have moved up 27 places in the city rankings to number 32 globally, whereas Kuala Lumpur is up 11 places to the 67th spot.

Uneven funding is one of the pressing issues highlighted in the Global Fintech Rankings report. This is even as statistics reflected the first quarter of 2021 to be a record year for fundraising by venture capital-backed fintechs, with every continent seeing a higher number of deals, if not money raised, compared to a year ago.

According to CB Insights, the number of fintech unicorns have increased from 61 in April 2020 to 108 a year later, with combined valuation of these unicorns more than doubling to US$440 billion.

But while established fintechs have been able to raise money with ease and at growing valuations, newer innovators seeking seed capital to tackle new problems thrown up by the pandemic have found the picture less rosy.

As an example, the authors cited online brokerage platform Robinhood, which raised US$3.4 billion in less than a week early this year to help it ride out a trading frenzy in talked-up stocks like GameStop. On the other hand, Israeli entrepreneurs interviewed said it was tough to tap funding, with investors wanting more control.

The report's authors questioned: "The threat is a bifurcated industry... We need to ask if this is how we, an industry built to democratise access to finance, want capital markets to work?"

Part of the challenge is in building trust and rapport with investors amid a pandemic. This has led companies to gravitate towards established financial hubs, where they will be more likely to grab the attention of venture capitalists.

Karen Puah, president of the FinTech Association of Malaysia, was quoted as saying: "The pattern that we see is that foreign funding misses us and goes straight to Singapore, so then you see a pattern of companies establishing headquarters in Singapore, when they're actually building here."

That said, the report acknowledged a growing diversity in funding sources and global connectivity, including capital from sovereign wealth funds.

It also highlighted the changing role of the state, "from bystander to cheerleader and regulator".

Countries like Singapore have allowed for "structured experimentation" through regulatory sandboxes that allow fintech companies to launch products to a limited number of customers without clearing onerous licensing rules. The report quoted Ravi Menon, managing director of the Monetary Authority of Singapore, who said that sandboxes allow experiments even where it is not possible at the outset to anticipate every risk and meet every regulatory requirement.

Mr Menon also said that if such experiments fail, they fail "safely and cheaply within controlled boundaries, without widespread adverse consequences".

Singapore was also highlighted for its ability to develop the fintech talent pool. The report's authors noted that the Republic had in the mid-2010s committed US$170 million to incentivise global financial institutions to set up innovation labs in the city.

On Wednesday, the Singapore FinTech Association announced the launch of SG FinTech Club, aimed at deepening social engagement among local fintech professionals and corporates. There are some 1,400 fintechs in Singapore today, accounting for more than 10,000 employees.

Central bank digital currencies (CBDCs) is another fintech innovation featured in the report that straddles the developed and developing world, as well as regulators and the private sector. It noted these digital versions of fiat currencies hold out "very different sets of possibilities" for the wealthiest and the poorest countries.

For poorer countries with limited infrastructure and dispersed populations, CBDCs could be a shortcut to financial inclusion that does not run through an expansion of bank branches. Wealthier countries, on the other hand, could reap institutional benefits, such as the easing of foreign currency settlement and reduced costs of global trade.

Poorer countries, including the Bahamas, Cambodia and China, lead on the roll-out of retail CBDCs, whereas richer countries lead on "wholesale" CBDCs, which would be held only by financial institutions. Singapore came up third in a PwC study on project maturity for interbank and wholesale CBDC projects.

In developed countries where banking is near universal, CBDCs pose a more immediate challenge to banks, with risks of deposit flights. This is less of an issue in less wealthy countries, where banks are not as central to the economy, precisely because larger parts of populations cannot access them.

Another reason for the slower development of CBDCs in richer countries, the report noted, is because of the complexity of schemes. In particular, some countries are looking to develop CBDCs in parallel with governments in other jurisdictions.

"Ultimately, we will need one universally accepted CBDC. That is why you are seeing countries seek to be the first, and focus on exchangeability," said Sindhu Bhaskar of the Government Blockchain Association, an international non-profit that promotes blockchain solutions for governments.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

1 in 5 fresh graduates from autonomous universities still seeking employment: MOM

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Cold Storage moves into convenience retail with On The Go, to replace FairPrice at 58 Esso stations

Why copper is becoming Asia’s next AI bottleneck