Private-sector economists lower Singapore 2019 growth forecast to 0.6%

Janice Heng

DeeperDive is a beta AI feature. Refer to full articles for the facts.

PRIVATE-SECTOR economists have sharply lowered their full-year growth forecast for Singapore to 0.6 per cent, down from an earlier 2.1 per cent prediction in June, in the Monetary Authority of Singapore's (MAS) quarterly survey of professional forecasters on Wednesday.

The downgrade is "hardly surprising given the escalation of the US-China trade conflict since the last survey", combined with much weaker than expected Q2 numbers, said Maybank Kim Eng economist Lee Ju Ye.

The lower forecast is also in line with the government's official forecast range of growth between zero and 1 per cent, which was lowered in August from the previous range of 1.5 to 2.5 per cent.

For the third quarter, the economists expect year-on-year growth to be 0.3 per cent. Maybank's Ms Lee and senior economist Chua Hak Bin believe Singapore "may have narrowly dodged a technical recession in the third quarter", as the manufacturing downturn eases on front-loading of trade orders - in anticipation of higher US tariffs - and services performance is bolstered by hospitality and finance.

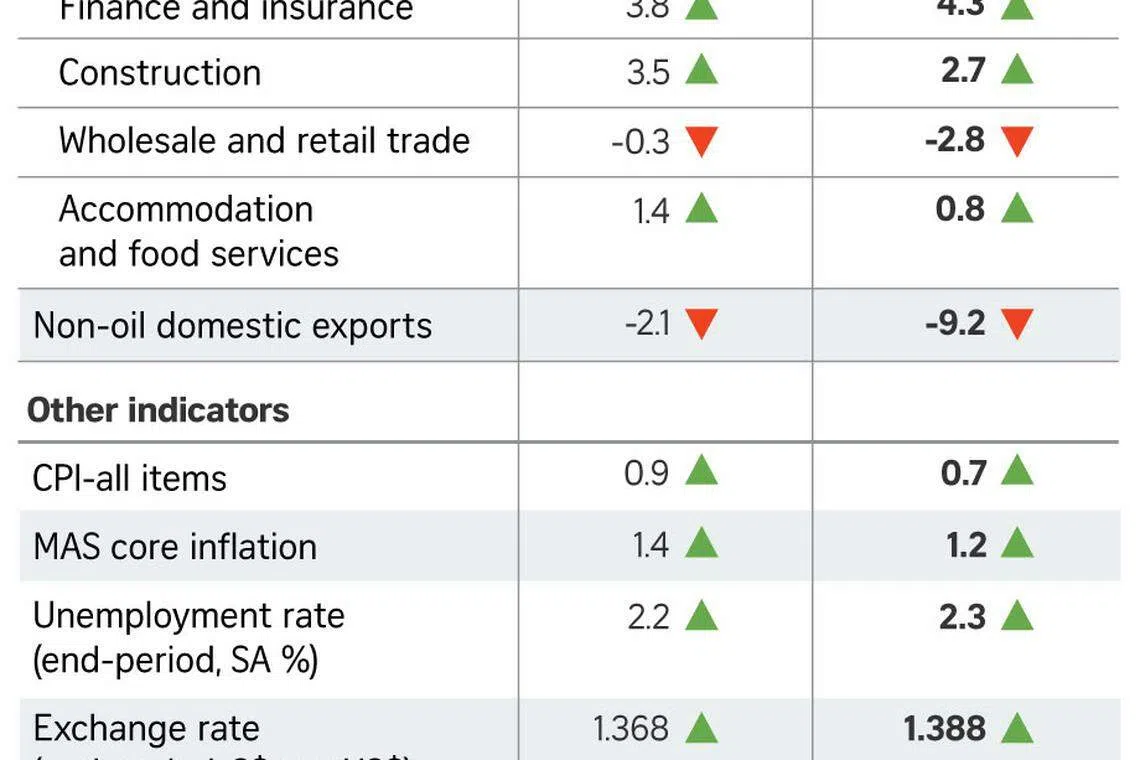

Sent out in August, the survey received responses from 23 economists and analysts. It does not represent MAS's views or forecasts.

Based on economists' expectations, the most likely range for full-year growth is between 0.5 and 0.9 per cent, with a better-than-one-in-three chance (37.3 per cent) assigned to this. Coming second is the range of zero to 0.4 per cent, with a probability of around 30 per cent.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

Compared to the June survey, growth predictions worsened for almost all sectors: manufacturing (-2.4 per cent, down from -0.2 per cent previously), construction (2.7 per cent, down from 3.5 per cent), wholesale and retail trade (-2.8 per cent, down from -0.3 per cent), accommodation and food services (0.8 per cent, down from 1.4 per cent).

Non-oil domestic exports is expected to shrink 9.2 per cent, worsening from an earlier predicted fall of 2.1 per cent.

The only improved expectations were for finance and insurance - expected to grow 4.3 per cent, up from 3.8 per cent - and private consumption, predicted at 3.4 per cent, up from 2.5 per cent.

Expectations have fallen for both core and headline inflation. Core inflation is now expected at 1.2 per cent, down from 1.4 per cent, and headline inflation at 0.7 per cent, down from 0.9 per cent.

As for the labour market, respondents expect 2.3 per cent unemployment, up marginally from 2.2 per cent previously.

While growth is expected to recover in 2020, economists' expectations have also moderated from the June survey. Full-year 2020 growth is now expected at 1.6 per cent, down from 2.3 per cent. The likely range is 1 to 1.9 per cent, down from the earlier predicted range of 2 to 2.4 per cent.

Further escalation of trade tensions and a slowdown in China remain the top two downside risks identified by respondents. Geopolitical risks in place such as Hong Kong and the Persian Gulf have also come to the fore, cited by nearly two in five respondents, up from just 5.9 per cent in June.

Easing of trade tensions remains the top upside risk, but fewer respondents now see that as likely, compared to June. Fiscal stimulus was the second most likely upside risk, cited by more than two in five, up from 17.6 per cent previously.

Copyright SPH Media. All rights reserved.

TRENDING NOW

Shelving S$5 billion office redevelopment plan proved ‘wise’ as geopolitical risks mount: OCBC chairman

Eurokars Group introduces rental car franchises Enterprise Rent-A-Car, National Car Rental, and Alamo to Singapore

20 photos that show how dramatically Singapore has changed in two decades

Singapore’s key exports up 15.3% in March from electronics surge, exceeding forecasts