Should you sacrifice some CPF Life income in favour of ILPs? Tread carefully

Consumers should educate themselves about the Retirement Sum Scheme and CPF Life, and view how these fit into their retirement plan

[SINGAPORE] AFTER covering personal finance for The Business Times for many years, I like to think that mis-selling of investment and insurance products would be few and far between.

But it seems this may not be so. In the Money Wisdom column in BT on May 22, Providend chief executive Christopher Tan recounted a pitch by a financial adviser (FA) representative to someone he knew, that she should fulfil only the Basic Retirement Sum (BRS) in her Central Provident Fund (CPF) account.

The balance that would have gone to fulfil the Full Retirement Sum (FRS) was to be invested in an investment-linked policy (ILP).

This would result in a relatively lower CPF Life income payout, which would then be supplemented by a supposedly higher income from the ILP.

That pitch was disturbing on some levels, which I’ll get to shortly. But the crux is this: How comparable is CPF Life’s payout to the distribution from an ILP?

Should you forgo the some of the income from CPF Life in favour of an ILP – or any other market investment?

CPF Life vs ILP

CPF Life is an annuity scheme that is better by far than any insurance annuity in the private sector.

This is because there are no distribution charges, no recurring fees and best of all, it pays a fixed income for life.

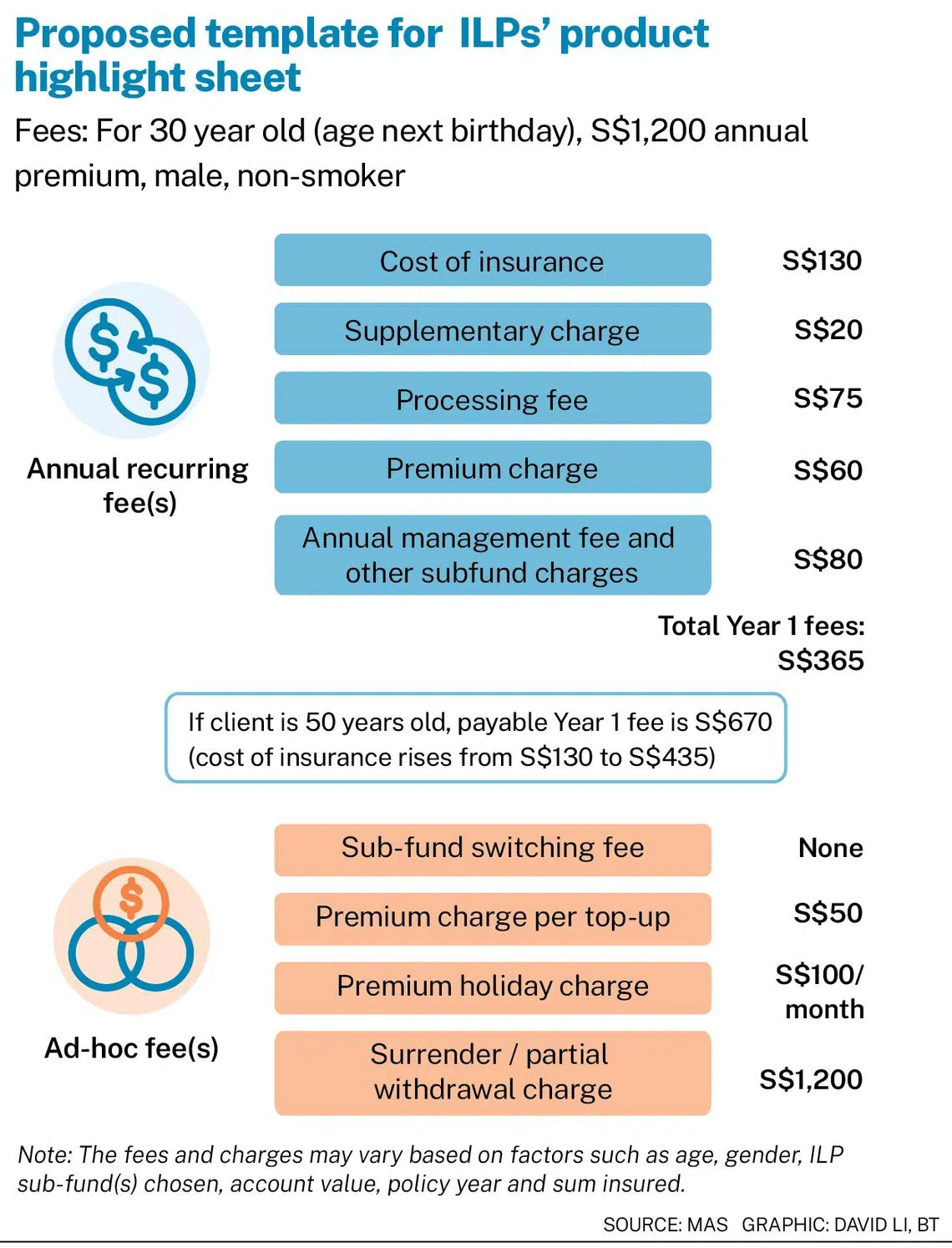

ILPs, in contrast, are investments wrapped in a high-cost structure. Exposure to market volatility introduces uncertainty in the income payouts. This plus the costs could greatly compromise retirement security, especially if you are counting on it for a steady income.

Longevity risk is one that looms for all of us. In retirement planning, CPF Life provides a “safe income retirement floor”, as MoneyOwl chief executive Chuin Ting Weber has said. High-net-worth individuals may not need CPF Life. But for most of us, it is a bulwark against the uncertainty of market investments.

Tan said that the BRS may be sufficient “for one who lives alone and belongs to the second quintile group in monthly expenditure”. This assumes the person has his own home, and the CPF Life income would meet monthly expenses.

“If this person does not own a property, he needs to set aside an amount equivalent to his cohort’s FRS in his Retirement Account at age 55 to ensure that he will not just have enough for monthly expenses, but also to rent a room when he turns 65.”

In planning for income for essential expenses in retirement, investors should look to “financial instruments that produce a reliable income stream with certainty regardless of financial markets”, said Tan. These include annuities and investment-grade bonds.

“For someone who has other sources of such type of income to meet essential expenses, then setting aside BRS is justifiable. Otherwise, one may need to have the FRS or even the ERS (Enhanced Retirement Sum) to meet this need,” he added.

“The issue is less whether it is right or wrong to ask someone to only set aside BRS. The issue is misrepresentation by the rep and to compare a market-based instrument with a government-backed, insurance-based annuity.”

MoneyOwl’s Weber said: “While some people may have valid liquidity needs to have to withdraw more of their CPF, I struggle to think of a case where an adviser might think it is better for a CPF member to give up the FRS and replace it with a commercial product that comes with substantial risk.

“After all, the industry has been selling products on the basis that CPF may be insufficient. FRS should be maintained as a safe retirement income floor for life, given that it is a modest payout.”

The Life Insurance Association has also weighed in.

Executive director Chan Wai Kit said: “Retirement planning should take into account an individual’s retirement needs, financial circumstances, affordability, risk appetite and protection objectives, alongside an understanding of the role that nationwide schemes play.

“CPF Life and the CPF Retirement Sum Scheme serve important roles in providing monthly retirement payouts for Singaporeans… Other financial tools such as savings, insurance and investment products may complement – but not substitute – these nationwide schemes.”

To be sure, the insurance industry does offer retirement products that promise an annuity income. Some products pay for a lifetime, or up to age 120. The products tend to be costly, and the payouts may not be fully guaranteed.

A questionable proposition

To recap, Tan’s column narrated the case of a FA representative who sought to persuade a prospective client that she would be better off investing in an ILP, instead of funding her Retirement Account up to the FRS.

The client is to fund the RA only up to the BRS, and the balance that would have gone towards the FRS would be invested in an ILP.

Based on the forward projections by the representative, the future income payout from the ILP would be more than 25 per cent higher than the CPF Life payout, with a S$200,000 “bequest” to boot.

The pitch made several questionable claims:

- That ILP investors are better off because the product provides a “bequest”, or is “capital guaranteed upon death”. ILPs do have a guaranteed sum assured, but to say it is capital guaranteed upon death is wrong, and a ploy to appeal to consumers’ preference for safe assets. It’s also untrue, as the Monetary Authority of Singapore and LIA have said. In any case, to project a substantial so-called bequest when the guaranteed death benefit may be as minimal as just 101 per cent of premiums is a misrepresentation.

- The ILP’s income payout was described as “dividends for life”; this is misleading. ILPs’ income payouts are not guaranteed, and may disappoint should markets experience a downturn and fund distributions decline. Note too that some funds make distributions out of capital and not from underlying portfolio dividends, profits or coupon payments, in order to satisfy a high headline distribution rate. For retirees, this suggests their fund capital may decline over time, unless there is a strong bull market trend.

- In the marketing material that Tan cited, the client was shown the strong historical annualised returns of two funds over the past 10 years to support the ILP proposition. The juxtaposition of these historical returns against the large projected future lump sum and income suggests that those returns could be repeated in the future. This is of course false; we’re always told the past is no indication of the future. In any case, the past 10 years have been highly rewarding for equities. This may not be so going forward as higher inflation begins to bite, and interest rates may rise instead of declining.

Guarding against mis-selling

How can a consumer guard against mis-selling? An independent financial adviser helps, of course. But absent that, it would help if you are familiar with the Retirement Sum Scheme and CPF Life, and how they fit into your retirement plan.

Use the CPF Life as a basic layer of retirement income, which you can supplement with other assets as your resources allow. Be wary of pitches that dangle high income but are not explicit on where risks lurk.

Weber believes regulators and industry associations play a role. “To prevent mis-selling, (they) may wish to adopt an advisory standard to not sell retirement products to persons without the FRS, except accredited investors with a significant amount of assets.”

Tan believes that consumer education itself is a safeguard.

“When more consumers are more financially literate, the better they can guard against errant advisers trying to mis-sell to them. It is sad that consumers have to tell the industry what to do, but my experience and history tell us this is the case,” he said.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.