Singapore hotels remain an attractive asset class for investment as recovery takes hold

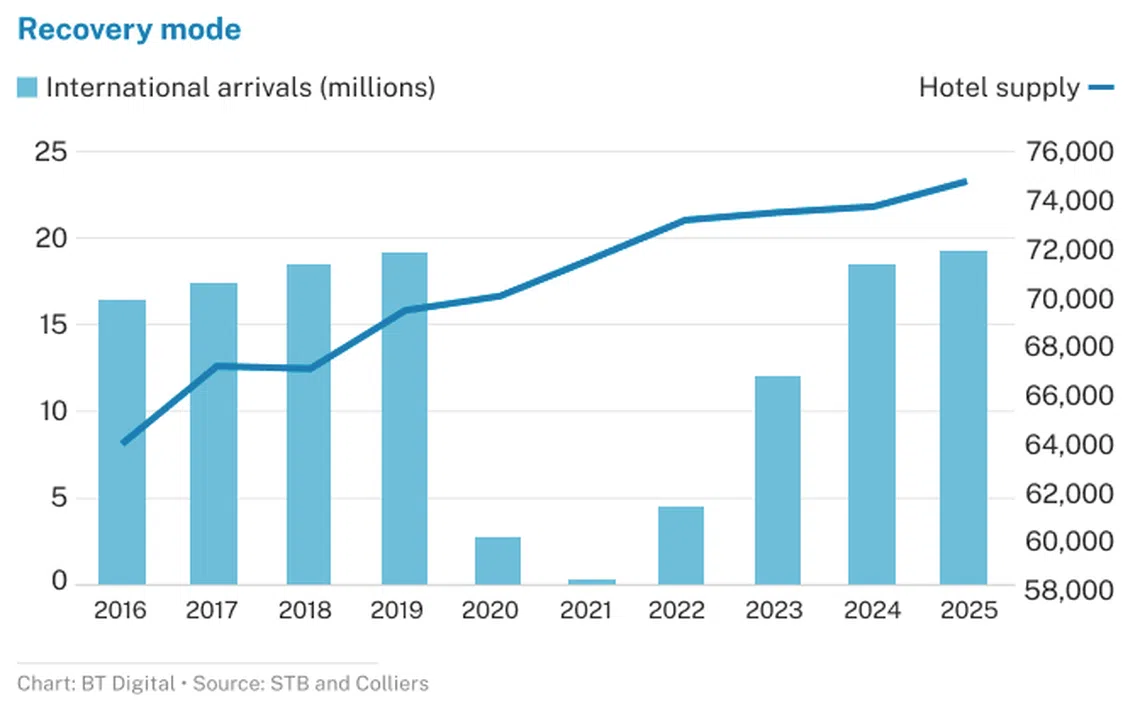

HOTELS in Singapore are witnessing a rapid bounce-back in performance, as travel rebounds with the full reopening of international borders in late April.

Despite the continued absence of the key mainland China source market, Singapore has experienced an influx of international visitors in recent months. Somewhat expectedly, for the year to July 2022, neighbouring countries such as Indonesia and Malaysia contributed over a quarter of all arrivals at 18 per cent and 9 per cent, respectively. Visitors from India made a significant contribution at 13.2 per cent, filling some of the void left by the lack of travellers from mainland China.

The effect on Singapore hotels has been pronounced, as in the year to July 2022, revenue per available room (RevPAR) performance doubled, achieving a near 20-per-cent year-on-year increase in occupancy rate. While there remains some way to go before the market returns to full pre-Covid level, it was a distinct improvement from December 2021’s performance – with RevPAR growth at 67.3 per cent and occupancy up by 12.8 percentage points, underpinned by strong Average Daily Rate (ADR) growth – as hoteliers pass on inflationary costs to consumers.

This uptick was reflected in the mid-year results of major domestic hospitality trusts and Reits with lodging assets in Singapore. Following two years of heavy reliance on domestic stays and government-based quarantine programmes, the strong results seen for the hotel market are reflective of the swift rebound in performance, which accelerated significantly with the easing of restrictions on international arrivals in the second quarter.

However, this “new age” of post-Covid hospitality has not dawned without its own challenges. Reduced airlift capacity – with ramifications on ticket pricing – across all geographical destinations and travel classes has become a primary barrier to a more marked return to travel, as the cost of airfare and flight availability are not as they once were. A shortage of labour across the sector – from airline staff to infrastructure workers to trained hotel professionals – has put pressure on the existing workforce.

Until more staff are recruited and trained, the situation will impede and prevent operators from reaching their optimum performance. If any benefit could be derived from China’s notable absence from the travel market, it has to be the allowance of time for travel bodies and hoteliers to progressively scale up their operations. Singapore and its airport could well have witnessed and been caught in a similar chaotic and negative situation as experienced by travellers in Europe and the UK during the northern hemisphere’s summer season.

Perhaps the most significant contrast to 2021 is the rising demand for “escape”, as Singapore residents embarked on their initial “post-Covid” journeys beyond the city-state, despite the high airfares. Many opted to travel to regional destinations, reducing the staycation business that has acted as a key contributor to Singapore’s resorts and upper-tier hotels over the last 2 years. With the return of international travel, the hospitality industry will continue to pivot away from the domestic market.

The final months of 2022 will produce an uneven recovery for the domestic hotel industry as mainland China’s outbound travel is likely to remain dormant in the near term, albeit offset by the Formula 1 Singapore Grand Prix returning in late September after a two-year hiatus.

Year 2023 may bring with it economic headwinds triggered by the Russia-Ukraine conflict, together with global inflationary pressures, which may well prove to be dampeners on consumer and business confidence, hence slowing the recovery. Despite the International Air Transport Association’s forecast of a rebound for international arrivals in the first quarter of 2024 on the back of the return of China’s travellers, it is still a big “if”. With the current situation in China, the outlook remains bleak and outbound travel could well recover only in 2024, with Hong Kong, Macau and Thailand being the early benefactors.

Looking ahead, the market will benefit from the country’s return to its standing as a key transit hub, a home cruise port and a regional centre for business and meetings, incentives, conferences and exhibitions (Mice) in South-east Asia. Hong Kong’s ongoing Covid-19 protocols for arrivals continue to hinder its attractiveness as an Asia-Pacific centre for business. Singapore has, most noticeably, benefited as the premier regional economic hub in the short-to mid-term as a result, attracting executive talent and experiencing a recovering Mice sector, as well as an improved number of corporate and social events. This will drive demand for rooms and re-engage a food and beverage sector that was decimated by 2 years of social restrictions and arrival limitations from abroad.

New room supply growth in Singapore is expected to be muted at a compound annual growth rate (CAGR) of 2.4 per cent, down from the 3.3 per cent between 2015 and 2019. In the next three years to 2025, approximately 5,415 new hotel rooms are projected to open, including the two white sites in Marina View and River Valley that have been listed on the government land sales reserve list, which, together, can potentially house around 1,070 rooms.

With rising demand for accommodation under a controlled global Covid-19 situation, coupled with restrained future supply, there is optimism for the future of Singapore’s hospitality industry.

Singapore’s hotels still present good value for money

Following a number of years of relative inactivity, with the view that the hotel sector would be well on its way to recovering to pre-Covid performance levels in early 2023, it is not surprising that there have been more investments in recent months. The path to recovery has become less opaque, despite global economic and geopolitical headwinds.

To date, the domestic market has recorded almost S$1.2 billion in transactions, led by the sale of 28 and 30 Bideford Road at effectively S$1.3 million per key, and SO/Singapore effectively at S$1.2 million per key.

While the average price per key seemingly fell between 2019 and the year to July 2022, it is more a reflection of the type and quality of assets traded over the period, rather than a drop in asset value. In 2019, more internationally-branded “upscale-and-above” hotels were traded than in the intervening period, which was marked by smaller, independent hotels in less well-located areas.

Despite the impact of rising operational and finance costs globally, Singapore remains on the wish-list of most investment groups. Domestic asset sales in 2019 totalled almost S$4 billion, which may seem unattainable given the cataclysmic effect of the pandemic on the industry. However, as Singapore cements its reputation as a preferred safe haven for capital, coupled with the ability of the market to provide a positive and stable performance outlook, the country’s hotels, serviced-apartment complexes and co-living assets will continue to attract investments.

Apart from a smattering of forced sales in the region, the distress story in hospitality has yet to materialise here. The weight of capital looking to secure assets that would normally not be for sale creates competition, hence lifting price levels. Being tightly held and with a strong trading outlook, Singapore’s hotels are rarely traded on yields. In reality, yields are tightening on hotels relative to real net operating income, particularly for well-located freehold assets.

While there is expectation for value to increase as the recovery unfolds, much of this is already priced into existing values. Higher bond yields are likely to push cap rates out; however, this will be mitigated by increased earnings, especially when this asset class allows the passing on of inflationary increases to consumers. The real impact may well be felt if, and when, interest rates start to rise significantly, which will counter the ability for hotels to pass on inflationary pricing.

The writer is executive director of hotels & leisure (Asia) at Colliers.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services

TRENDING NOW

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Wanted: 100 AI specialists, 100 wealth relationship managers at HSBC Singapore

China chipmaker CXMT jumps 472% in debut after US$9.8 billion IPO

Temasek should publicly state its position on the long-rumoured CapitaLand-Mapletree merger