Retail space rents in central region of Singapore edge up 0.6% in Q4, rise 0.5% for 2024

Retail asset prices down 1.3% in the quarter: URA

Bapat Sara Manish

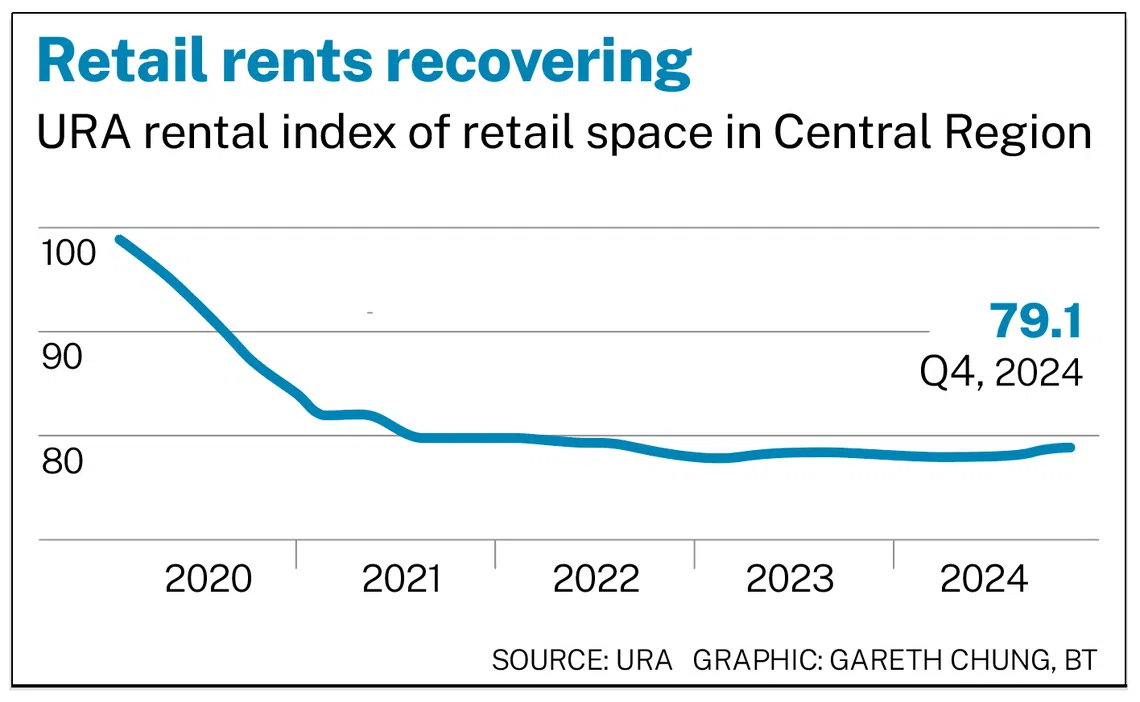

RETAIL space rents in Singapore’s central region rose 0.6 per cent in the fourth quarter of 2024, edging up from a 0.3 per cent increase in Q3.

For the whole of 2024, rents increased by 0.5 per cent, slightly higher than the 0.4 per cent increase in 2023, data released by the Urban Redevelopment Authority (URA) on Friday (Jan 24) showed.

This marks the second straight year of growth after central region rents nosedived in 2020, before flattening out from 2022.

Retail rents have been moving up despite a challenging operating environment marked by high labour, material and occupational costs, Knight Frank Singapore head of research Leonard Tay observed.

Occupancy improved slightly in the last quarter. Islandwide, the retail vacancy rate decreased to 6.2 per cent in Q4, from 6.5 per cent in Q3.

Tricia Song, CBRE’s head of research for Singapore and South-east Asia, noted: “All sub-markets experienced positive net absorption in Q4 2024, with the exception of the fringe area, which saw no net absorption.”

The Downtown Core sub-market outperformed in the quarter, she added.

In 2024, islandwide vacancy rates fell by 0.3 percentage point to the lowest levels in 10 years since Q4 2014.

Angelia Phua, JLL’s consulting director for research and consultancy, cited resilient occupier demand as the reason for improved occupancy, as well as the entry of new-to-market brands and the expansion of existing brands.

Tay of Knight Frank also noted that many foreign brands prefer central locations. French sports brand Salomon opened outlets at Ngee Ann City and Orchard Central, while Finnish lifestyle brand Marimekko is opening its second store in Ngee Ann City.

Other fashion and sports brands, including Burberry, Tom Ford, Li-Ning and Decathlon, also increased their presence during the quarter.

Wong Xian Yang, Cushman and Wakefield’s head of research for Singapore and South-east Asia, said that notably, net demand in the Orchard Road area was very positive – an additional 140,000 sq ft of space was taken up, outstripping the 65,000 sq ft of supply that was taken off the market.

According to CBRE, landlords “sustained a rise in prime floor rents amid strong demand for retail spaces in Q4 2024”. Some food and beverage operators expanded their footprint, “although the fine dining scene continued to witness closures (including those of) Sushi Kimura, Voyage, and Chef Kang’s”, said Song.

In Q4, the amount of occupied retail space rose by 47,000 sq m of net lettable area (NLA), up from the NLA increase of 17,000 sq m in the prior quarter, the URA data showed.

Retail stock increased by 24,000 sq m of NLA in Q4, also greater than the 14,000 sq m NLA increase in Q3.

Caution ahead

While rents appear to be on an upward trajectory, retail asset prices fell 1.3 per cent in Q4, reversing from a 1.7 per cent increase in the previous quarter.

JLL’s Phua said that investors likely turned more cautious, amid a potentially higher-for-longer interest rate environment under the Donald Trump administration in the US.

Despite this, year on year, prices climbed 1 per cent, making 2024 the second consecutive year of price increases.

As at end-Q4, the total retail space pipeline supply stood at about 545,000 sq m of gross floor area, down slightly from the 552,000 sq m of such supply in Q3.

Market watchers expect rents to rise between 1 and 3 per cent in 2025.

Sustained domestic consumption, a positive tourism outlook, and Singapore’s draw as a business and events hub will continue to spur retail expansion in Singapore, said Phua.

CBRE Research expects overall prime retail rents to recover to pre-pandemic levels in 2025.

Still, several challenges continue to dog the retail sector. Knight Frank’s Tay said: “The strong Singapore dollar, coupled with inflationary pressures, have resulted in many local consumers taking their spending to other countries where retail and recreation costs are more affordable.”

Such “leakage”, as well as retailers’ sensitivity to rent hikes, could cap rent growth potential, said Phua.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services