Singapore’s inflation to slow but stay high in 2023 as firms pass on costs: MAS

Elysia Tan

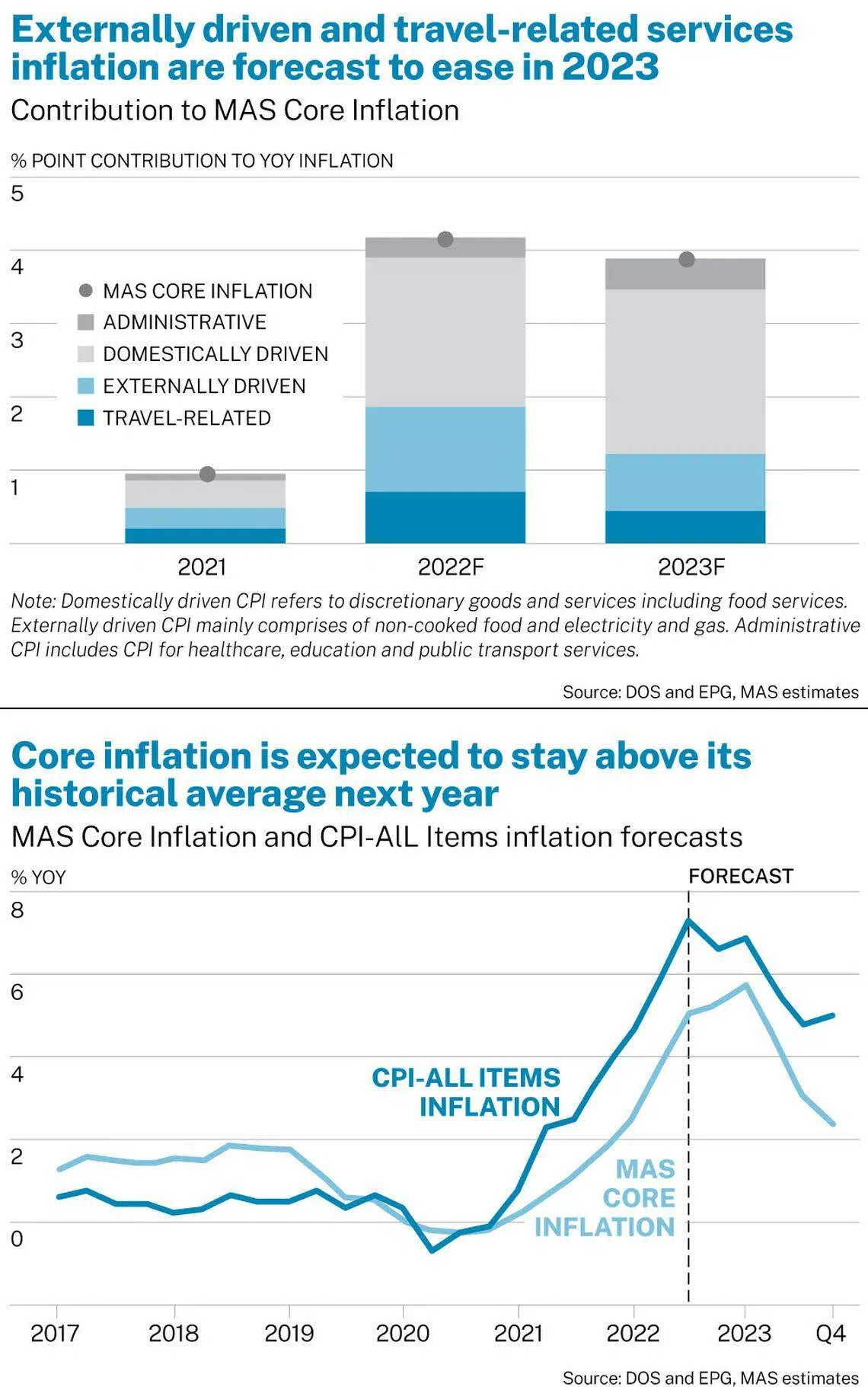

SINGAPORE’S core inflation is expected to be driven more by domestic than external pressures in 2023, with inflation slowing but staying high over the course of the year, according to the Monetary Authority of Singapore’s (MAS) latest half-yearly macroeconomic review on Thursday (Oct 27).

MAS said that domestic inflation is likely to persist at elevated rates for some time, “as firms adjust prices to catch up with the steep increases in input costs that have accumulated along production chains”. More domestic businesses are likely to renew contracts, such as those for electricity and wages, at higher rates.

In contrast, on the external front, easing supply constraints and weakening global demand should bring commodity prices down. Still, imported inflation will stay firm as “still-elevated” electricity and fuel costs and strong wage growth in major trading partners will “continue to filter through global supply chains”.

As for headline inflation, Maybank analyst Lee Ju Ye said rental costs will contribute to keeping it high, as rents rise with the return of non-resident workers, delays in property completions, and possibly higher demand from property sellers going through the 15-month HDB wait-out period.

MAS reiterated its 2023 projections for core inflation – which exclude accommodation and private transport costs – to average 3.5 to 4.5 per cent, and headline inflation to average 5.5 to 6.5 per cent.

Domestic wage growth – another contributor to inflation – is expected to slow but remain above pre-Covid levels in 2023, even after labour shortages ease in the second half of 2022. It takes about three quarters for the effects of labour market tightness to pass through fully to nominal wage growth, said MAS.

On a quarter-on-quarter seasonally adjusted basis, nominal resident wage growth was 1.5 per cent in Q2 2022, down from 1.7 per cent in Q1 and from the peak of 2.3 per cent in Q4 2021. But this was still almost double its historical norm.

Similarly, on the year, nominal resident wage growth stayed high at 6.8 per cent in Q2, though down from 7.8 per cent in Q1. Wages were 2.7 per cent above the level implied by the pre-Covid trend. Given high inflation, MAS expects “positive, but modest” growth in average resident real wages this year.

MAS also noted short-term boosts to wage growth. First, in pandemic-hit industries like travel, there remains room for wages to catch up to pre-Covid trends. Second, low-wage worker policies are estimated to boost average resident wage growth by about 0.2 percentage point.

Third, with the rising cost of living and expectations of permanent higher wage and price levels, workers are likely to seek and get above-average wage increments.

The risk of a wage-price spiral – where higher prices cause workers to demand higher wages, raising business costs and prompting further hikes – “is assessed to be low, primarily as the effect of price pressures on wage increases is empirically weak”, said MAS. But nominal resident wage growth “could remain somewhat elevated above pre-Covid averages if inflation expectations remain persistently high”, it added.

However, OCBC chief economist Selena Ling thinks employers could be cautious in view of heightened recession risks in major economies, adding that 2022 has already seen “relatively outsized wage adjustments”.

UOB senior economist Alvin Liew flagged that services inflation reached a new year-on-year high since data first became available from 2014. As a reflection of domestic wage pressures, this points to rising risks of a wage-price spiral, he said.

Another consideration for the inflation outlook is the hike in the goods and services tax (GST) in January. This will cause core inflation to rise in Q1 2023, but its impact should be temporary, said MAS. Excluding the effects of the GST increase, core and headline inflation are expected to average 2.5 to 3.5 per cent and 4.5 to 5.5 per cent respectively in 2023.

OCBC’s Ling expects significant pass-through of the GST increase, as businesses are more confident about passing on costs given local consumers’ continued willingness to spend.

Even if costs are passed on, purchasing power is unlikely to suffer significantly, said RHB senior economist Barnabas Gan and Maybank’s Lee, noting the cushioning impact of the S$6.6 billion GST Assurance Package.

Thursday’s report included a separate study on the effect of rising global input costs, which found that spikes in global energy and agriculture prices explain over two-thirds of core inflation pressures in Singapore over June 2021 to June 2022.

“In Singapore, most of the international price effects on the domestic sectors are transmitted via intermediary sectors located abroad,” the study said. This is in contrast to the United States and European Union, where global prices take effect via domestic supply chains.

Another study found oil price shocks had different impacts across Asean+3. The Asean-5 – Indonesia, Malaysia, Singapore, Thailand and the Philippines – were hit harder than China, Japan and South Korea, but less than the remaining Asean economies.

Oil price shocks have a smaller effect on inflation in net energy exporters than net importers, as well as in inflation-targeting regimes, said the study.

*Amendment note: An earlier version of this article carried an incorrectly labelled graphic. The error has been corrected.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.