Integrated Shield Plan lifetime premiums vary widely across insurers, MOH comparison shows

TWO people of the same age buying an Integrated Shield Plan (IP) for private hospital treatment can pay a difference of more than S$85,000 over their lifetimes – depending on which insurance company they are with.

An IP is optional health coverage provided by private insurance companies, typically to cover stays in A or B1-type wards in public hospitals or private hospitals. A total of 2.9 million people here, or more than 70 per cent, have signed up with one of seven insurers offering such coverage.

Data published for the first time by the Ministry of Health (MOH) shows that premiums can vary significantly, even for plans pegged to the same ward class, since both coverage and price are determined by the insurer.

MOH’s website shows the premiums that people have to pay for IPs from the time of birth to the age of 100, based on rates in effect on Apr 1.

Buying the most expensive private hospital IP by AIA can set a person back by S$323,900, the bulk of which has to be paid in cash. In contrast, the three cheapest, by Raffles, HSBC and Income, cost between S$234,400 and S$238,400.

For public hospital IPs, the difference between the most expensive and the cheapest is more than S$50,000 for Class A coverage, and about S$35,000 for Class B1. Both are private wards.

Choosing one’s IP wisely has been a common refrain from MOH in the past few years, and publishing premiums makes it easier for people to make an informed choice.

Wee Hwee Lin, director of the Centre for Health Interventions and Policy Evaluation Research at the NUS Saw Swee Hock School of Public Health, applauded the ministry for making such information transparent.

She said: “This is clearly useful for people to review their existing insurance policies but with caveats. It is not possible for people with existing medical conditions to switch providers.”

This is because most insurers will not provide full coverage to new policyholders who have pre-existing medical conditions.

Still, Wee said the information on premiums can help younger people choose their insurer.

Her colleague, Cynthia Chen, whose research areas include the economics of ageing and healthcare financing, said that when choosing an IP, “it helps to look at what they cover on top of MediShield Life for the increase in premium”.

She added: “Consider the pricing of premium, insurance coverage, family health. Also, individual preference for hospital wards and financial risk. IPs provide greater financial protection should an adverse event occur, compared to MediShield Life.”

But different insurers offer different coverage for the same medical problem.

Coverage for kidney dialysis for Class B1 plans, for example, ranges from S$24,000 a year to “as charged”. Similarly, coverage for community hospital care, which is capped at 45 days per admission for some plans and 90 days for others, is up to S$450 a day with one insurer, S$1,000 a day with another, and “as charged” with a third.

Similarly, some private hospital IPs provide for critical illness and others do not, while Class A coverage for psychiatric treatment varies from S$4,500 to S$7,000 a year, to coverage for up to a certain number of days.

To confuse matters further, the lowest coverage may not come from the insurer charging the lowest premiums.

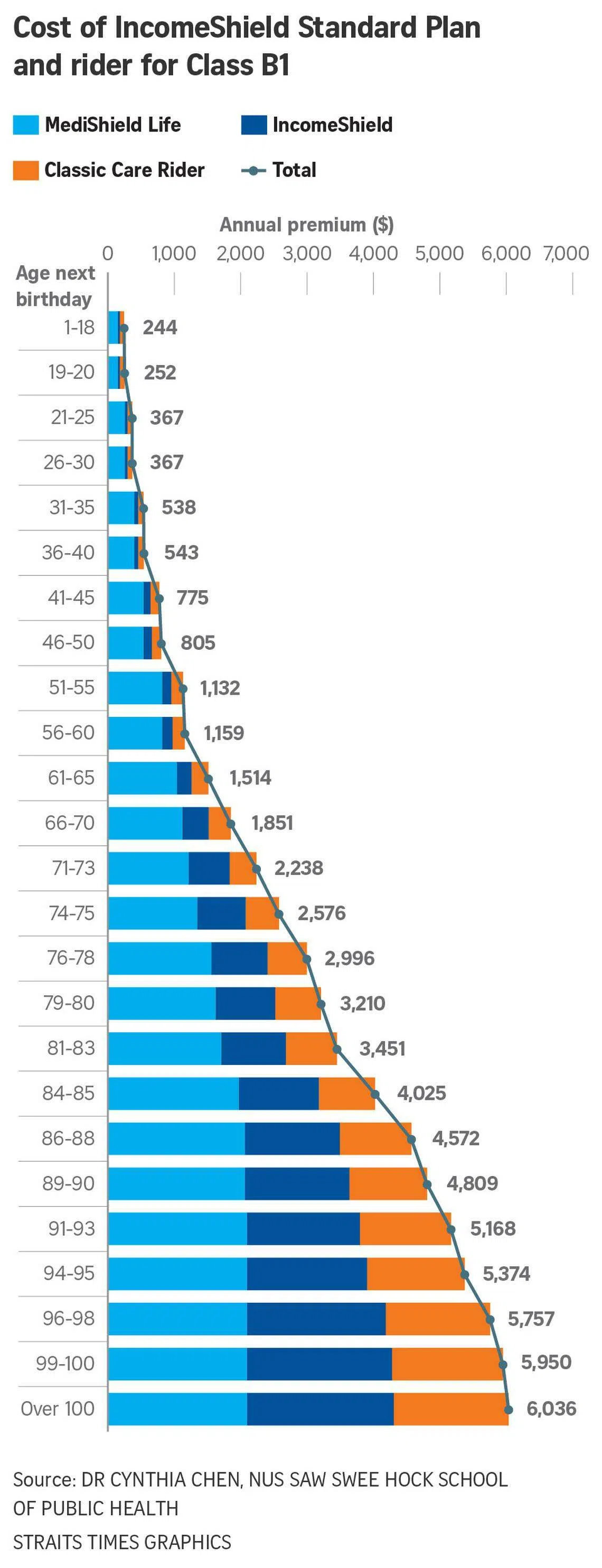

The only IPs where the coverage is identical across the board is the Standard IP for B1 wards, as the coverage is stipulated by MOH. In spite of that, the seven companies offering this charge different premiums, with more than S$22,000 difference between the most expensive and the cheapest, over a lifetime.

Wee said choosing an IP boils down to personal preferences and how one wishes to allocate one’s budget.

“Assuming that I am willing to put aside 10 per cent of my net income for healthcare, and assuming a median monthly salary of S$3,300, then annually, I am putting aside S$4,000, or S$180,000 over 45 years of working life,” she explained. Given the calculations made by the MOH, at best, she will be able to afford a Class A IP.

The ministry has also shown the proportion of premium that can be paid by MediSave, and the amount that has to be paid in cash.

The lifetime cash outlay for the most expensive private hospital IP at today’s rates exceeds S$260,000.

Chen said people must expect the cost of healthcare to go up, and likewise, insurance premiums.

MOH’s calculations do not take into account future premium increases that, historically, vary from insurer to insurer, and year to year.

In September 2022, Health Minister Ong Ye Kung said: “Private hospital IP premiums have already gone up by around 20 per cent over the past few years. At this rate of increase, in five years’ time, someone in their 50s will probably have to pay about S$300 more in annual premiums.”

Such expected increases must also be considered when choosing the class of IP to purchase.

Furthermore, significant numbers of people pay for the highest possible coverage, but choose a lower class ward when they actually need medical care.

From 2020 to 2022, 57 per cent of patients with IPs chose subsidised wards when they were hospitalised, according to the Central Provident Fund Board. Among those with private hospital IPs, less than half actually sought treatment at a private hospital.

More than one million people here also have riders to complement their IPs. IPs can pay a maximum of 90 per cent of the bills. The rest have to be paid using MediSave or cash. Having a rider can cap a patient’s outlay to 5 per cent of the bill, up to a maximum of S$3,000 a year. Premiums for riders have to be paid in cash.

Wee said that in choosing medical insurance, people should think of both affordability and the probability of their needing such coverage. They should also think of their desired comfort level and the trade-offs with reduced disposal income.

“For example, before getting a rider that covers cancer drugs not on the Cancer Drug List, think about the probability that you are going to need one of those drugs,” she said, referring to how IP coverage is limited to drugs on MOH’s list, but insurers are free to cover other cancer therapies with their riders. THE STRAITS TIMES

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services