I tracked my dad’s expenses to find out how much retirement costs

Straight to your inbox. Money, career and life hacks to help young adults stay ahead.

[SINGAPORE] When I was about five, I promised my dad that when he retired, I’d buy him a pink Ferrari and fill his bank account with millions.

So when he had to stop working because of his health during my second year of university, the moment carried none of the fanfare we had imagined.

My dad now lives off a decent retirement fund, built over decades of saving consistently.

When I asked what’s a good number to retire on, my dad – who never saved for retirement with a specific goal in mind – didn’t have an exact answer.

Conventional wisdom, on the other hand, places that figure at around S$1 million.

Other estimates vary more widely. A DBS study estimated that Singaporeans may need S$550,000 for “conservative needs” and S$1.3 million for more “aspirational wants”. A separate HSBC report found that affluent Singaporeans may need US$1.39 million (S$1.77 million) for retirement.

So, I did a little experiment from home. For two weeks, I tracked my dad’s daily spending to find out how much one truly needs to fund their expenses in retirement.

Day in the life

For someone who spent his career designing menswear, you’d ironically spot my dad rotating between a few polo tees and bermuda shorts.

Splurging on material goods was never really his thing, and even less now in retirement. So, it wasn’t a surprise when his retail expenditure totalled zero during the two weeks I tracked him.

His largest outlay, however, was food. “When it comes to food, I am willing to splurge a little more,” my dad tells me.

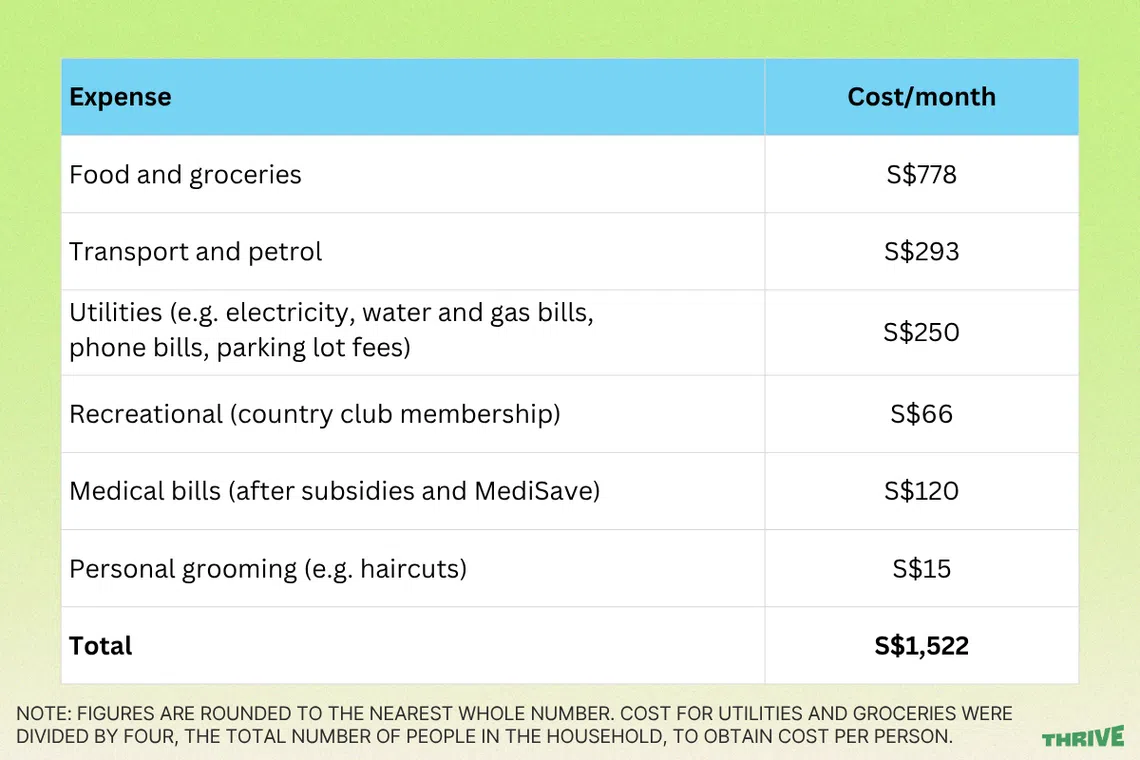

On average, he spends S$194.60 per week on meals and groceries, or about S$778 per month.

My dad often sticks to familiar favourites: bread and coffee for breakfast, and takeaways from hawker centres or home-cooked meals for lunch and dinner. Once a week, he dines out with friends or family.

For exercise, my dad swims and uses the gym at his country club, which costs about S$66 a month.

Other monthly expenses include utility bills, petrol and medical expenses. His car and the home are both fully paid off, which means he does not have to make monthly loan repayments.

All told, my dad’s monthly spending comes up to about S$1,522.

This excludes other big-ticket items such as travel, house repairs, or celebratory outings.

But there are still some less frequent expenses that recur over the year. Car servicing costs about S$1,800 every six months, and my dad goes on about two cruises a year, which cost around S$1,000 each.

Factoring these in, his estimated annual expenditure comes to S$23,864. Stretched across a 20-year retirement, that works out to S$477,280.

This is, by many benchmarks that I can find online, on the low end. My dad also acknowledges that his lifestyle skews modest.

How he funds retirement

The bulk of my dad’s retirement expenses comes from cash savings stored in his bank account.

Over the years, my dad also topped up his Central Provident Fund (CPF) Retirement Account regularly. Now, he receives monthly payouts of about S$500 from CPF Life – the national annuity scheme that provides payouts for life.

My dad’s only source of investment returns comes from an endowment plan, a hybrid insurance-savings product he bought years ago. It now pays him in small periodic disbursements.

“Even when I was younger, I was afraid of making risky investments,” my dad says.

My dad’s generation didn’t have easy access to financial education or resources, and his savings strategy reflects that: low-risk and not very diverse, but stable.

What I learnt

Although S$477,280 may seem like a small sum for retirement, it’s enough for a modest life with comfort and routine, without excessive splurging or deprivation.

This figure does, however, leave little room for, say, a medical crisis or a longer-than-expected retirement.

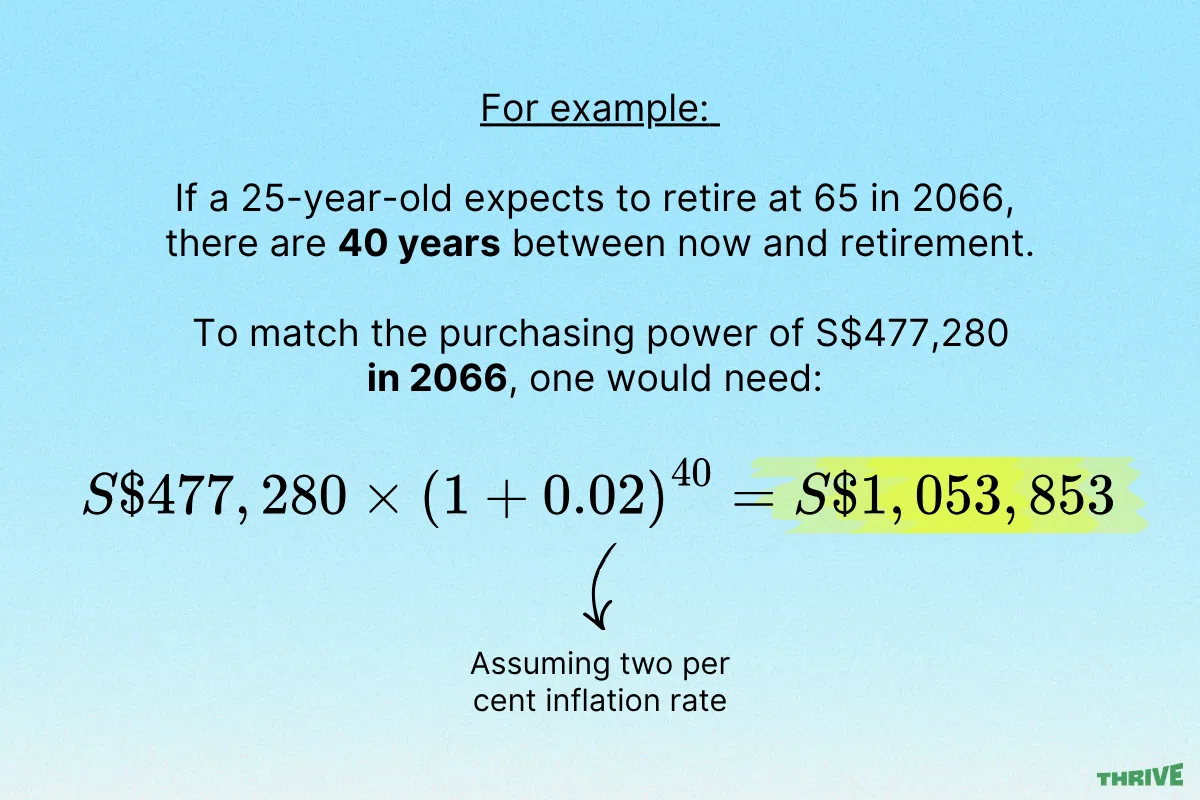

And while it may be a useful benchmark for someone retiring today with a lifestyle similar to my dad’s, that number will inevitably rise with inflation for someone younger like myself, who may retire in 2060 or later.

Assuming an inflation rate of 2 per cent, I would need about S$1.05 million to maintain a lifestyle similar to my dad’s.

That would mean saving roughly S$2,200 a month between now and age 65. But that figure also needs context.

My salary will likely rise over time. I also plan to invest, and returns from my investments should lighten the amount I need to set aside in cash. On top of that, a significant portion of my monthly income already goes into CPF, and CPF interest will help grow part of my retirement savings.

That said, my earlier calculations don’t quite capture one big uncertainty: healthcare costs. In Singapore, rising medical costs have been a growing concern, and the cost of living – and retiring – for our generation may look very different from our parents’.

But the biggest lesson I learnt is that I don’t need a fancy retirement strategy or sophisticated portfolio to build a decent retirement fund. Simply saving consistently can be substantial if I start early.

Retirement can feel too far away to think about seriously, but putting a rough number to it makes it easier to plan, save, and hopefully avoid falling short.

More than that, it makes the goal feel more achievable and less abstract.

And with fewer qualms about my nest egg, perhaps between now and retirement, I’ll also have enough to buy a new car (perhaps not a Ferrari) for my dad to enjoy in his retirement.

This article also appears in Switching Lanes, a column exploring the diverse realities of life after a full-time career, and redefining what it means to retire well.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

UOB to sell asset management arm to Allianz Global Investors for S$555 million, sharpen wealth advisory focus

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

1 in 5 fresh graduates from autonomous universities still seeking employment: MOM

Yeoh Pei Xien: YTL’s third-gen scion with a pastor’s heart