Little treats, big problems: When everyday luxuries creep up on you

Straight to your inbox. Money, career and life hacks to help young adults stay ahead.

[SINGAPORE] When I was an intern earning S$800 per month, coffee shop lunches kept me perfectly content. The idea of heading to a restaurant during lunch break never crossed my mind.

Eighteen-year-old me would be horrified to learn the price of the burrito I ordered on Foodpanda just because it was “too hot to go out”.

TikTok tells me that these are “little treats” – something to help me get through an oh-so-dreadful day of working from home.

The concept isn’t new. It went mainstream with Parks and Recreation’s “Treat Yo Self” catchphrase back in 2011.

What makes Gen Z different is how this habit has gained traction on social media at a time when they’re graduating into rising living costs and an uncertain job market.

There’s also an almost nihilistic tinge to the trend: If owning a home feels impossible, why can’t you let me enjoy that S$7 bubble tea or S$25 Labubu and call it joy?

⚖️ Why it matters

The danger of “treat-yo-self” behaviour lies when occasional treats become the norm.

Take travel. Economists would call it a luxury expense, yet 44 per cent of Gen Z travellers in Singapore say travel matters more than other financial goals, according to a recent survey by Skyscanner and Trust Bank.

That’s treat culture turning into lifestyle creep. Small decisions we justify as self-care or rewards become everyday habits, especially as salary grows.

On paper, you might still be diligently saving more than before.

But here’s what I realised a few years into working life as my salary grew: While the absolute amount I was saving went up, my savings rate (the percentage of my income I put aside) actually fell.

That’s a problem because your savings rate, not dollar amounts, can determine whether you can retire on time.

A person saving 80 per cent of his or her income can generally retire earlier than someone saving 20 per, regardless of what they earn. That’s because it usually means one of two things:

- The first person is living on less, so they won’t need as much for retirement, or

- The person saves more, and can reach his or her retirement target earlier

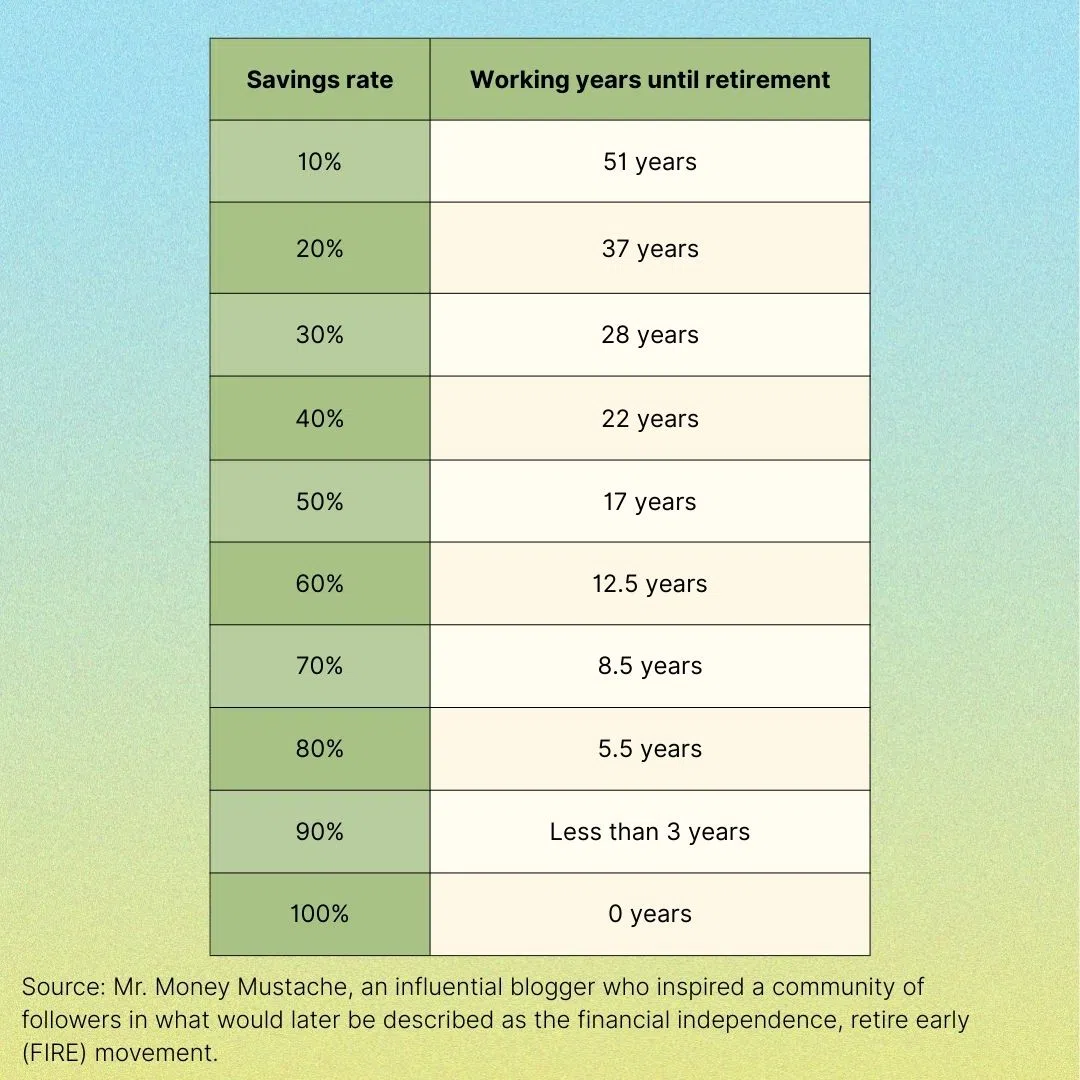

Here’s a popular chart that people in the FIRE (financial independence, retire early) communities like to use. It assumes you earn 5 per cent investment returns after inflation during your saving years and that during retirement, you spend based on the 4 per cent safe withdrawal rule.

By this logic, the person saving 80 per cent of their salary can retire in 5.5 years, provided the person does not change their spending habits throughout retirement. The person saving 20 per cent would take 37 years.

🛠️ How I keep it in check

As I’ve become more aware of lifestyle creep over the years, I’ve become more conscious of my spending habits.

Here’s what has worked for me:

- Check my savings rates regularly. I compare the percentage I saved this year versus last year. If it’s slipping, I know lifestyle creep is probably to blame.

- Scan my credit card bill. Whenever I’m paying my credit card bills, I briefly scan my statement to track how much I’m spending by category. The first time I saw how much I was spending on dining per month, I was shocked. Awareness alone curbed some of the excess.

- Automate my savings. I set up scheduled transfers from my bank to my investment brokerage the day my pay arrives. It’s easier to avoid spending that money when you don’t see it in your bank account. The hard part is remembering to increase the transfer amount whenever I get a pay raise.

- Budget for treats. Working out my savings rate gives me an idea of how much I can spend. To prevent impulse buying, I set myself a monthly budget for guilt-free spending on indulgences.

👻 When spending more can be justified

It’s worth saying that not every increase in spending is necessarily bad. For many of us, the first pay cheque one receives after years of living on student allowances feels like coming up for air.

Sometimes, liberating yourself from S$3 cai png and worn-out sneakers isn’t necessarily lifestyle creep. It can be seen as a correction, catching up to a baseline of comfort you couldn’t afford before.

In fact, it can even be healthy. Spending a bit more on nutritious food, exercise gear that’ll keep you motivated to work out, or skincare that keeps you confident are all part of taking better care of yourself.

The key is knowing whether you’re upgrading your lifestyle to a sustainable level, or just normalising luxuries that keep pushing the bar higher.

So yes, treat yourself. But watch out for lifestyle creep, and don’t let little treats turn into big problems.

TL;DR

- Little treats feel harmless, but when they become routine, they morph into lifestyle creep

- Gen Z has embraced treat culture on social media, celebrating small luxuries while big milestones feel out of reach

- Saving more in dollar terms isn’t enough if your savings rate is dropping

- Budget for treats, track spending and automate savings to stay on track

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Wanted: 100 AI specialists, 100 wealth relationship managers at HSBC Singapore

China chipmaker CXMT jumps 472% in debut after US$9.8 billion IPO

Temasek should publicly state its position on the long-rumoured CapitaLand-Mapletree merger