🧸 Is it ever too early to start working on financial literacy?

Straight to your inbox. Money, career and life hacks to help young adults stay ahead.

- Find out more and sign up for thrive at bt.sg/thrive

🎹 Move aside, piano lessons

Should the usual childhood swimming, art or music enrichment classes be replaced with money management sessions and financial literacy camps 🧮?

That seems to be the approach parents such as mother-of-three Stella Hoh have taken when planning their children’s after-school lessons.

These classes focused on financial literacy are open to children as young as 10, teaching them skills such as budgeting and spending within their means.

And before you think that this is the work of tortuous tiger mums, more teenagers also recognise the need to be financially savvy earlier in life.

Take 16-year-old Matilda Poh, for example, who wrote to The Straits Times Forum section in April this year calling for schools and parents to do more to make young people financially aware amid the rising costs of living 📈.

Still, while financial literacy enrichment classes may be extreme to some, Lorna Tan, head of financial planning literacy at DBS Bank, tells thrive that starting on financial literacy earlier for young adults between the ages of 18 and 20 can allow for greater flexibility for course correction, if need be.

“If a young adult discovers that a particular financial approach doesn’t suit them early, they have ample time to adjust their strategies before reaching their 40s and beyond,” she explains.

At present, financial literacy education is infused as a component of Character and Citizenship Education (CCE) lessons in Singapore’s schools.

Additionally, MoneySense – the national financial education programme – and its partners have programmes and activities that are open for students to participate in.

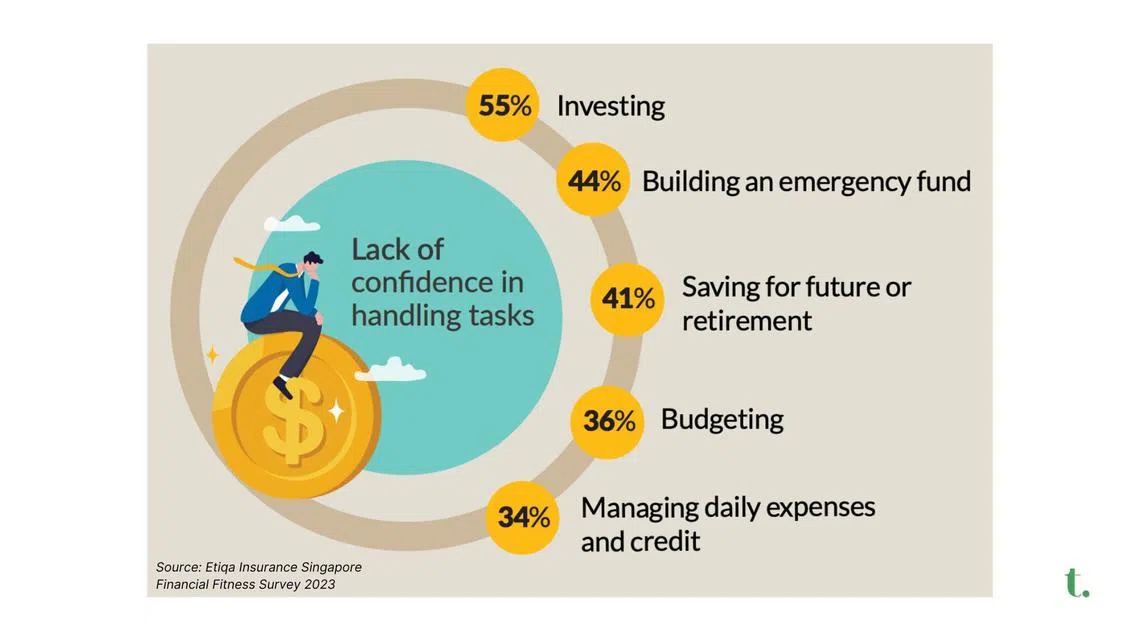

However, is that enough to help tertiary students become more financially prepared in today’s world? According to Etiqa’s Financial Fitness survey in 2023, one in three Gen Zs and millennials today do not feel confident in making sound financial decisions during times of economic stress.

The report also found young Singaporeans to have particularly low confidence in investing and building emergency funds.

In April 2023, Member of Parliament Gerald Giam proposed introducing financial literacy as a standalone subject in schools instead of addressing it in a “by-the-way” fashion in the CCE curriculum of schools.

Such a move would better allow students to build good financial habits consistently from young, according to Giam.

His critique of MoneySense as the city-state’s wider national financial education programme was that it mainly runs on an ad-hoc basis at present and is largely “campaign driven”.

“Age-appropriate modules in schools covering key topics such as credit use and investments could ensure all students have access to financial literacy skills,” Giam says in an interview with thrive.

Expanding the existing financial literacy curriculum to include knowledge on the Central Provident Fund (CPF), interest rates, and investing could also empower more young adults, says Tan.

“Early financial education with these aspects will allow young adults to gain a practical understanding of financial principles and their real-world implications,” she says.

Danielle (not her real name), 27, who currently works in Singapore’s sustainability sector, feels that it could have been helpful to be formally taught financial literacy in school earlier, possibly through an independent subject.

“It may be hard to see how financial literacy is relevant when you’re younger,” she admits.

“But things such as comparing insurance policies and understanding crucial fundamentals such as CPF or Housing Development Board (HDB) loans can feel daunting in your 20s without the right foundations in place.”

📏 Issue of standardisation

Creating a standardised curriculum on financial literacy across schools in Singapore, however, is not so simple, according to Lawrence Loh, professor and director of the Centre for Governance and Sustainability (CGS) at NUS Business School.

“A structured, systematic approach to financial literacy at a tertiary level would be achieved by embedding it formally into the curriculum,” he explains. “This means that the programme must fit the needs of the students at the time.”

However, Loh also notes how there is no one-size-fits-all approach to this topic. “Everyone comes from varying socio-economic backgrounds, and at such a young age, the needs and financial priorities of each student can look very different.”

He points out that the curriculum at a tertiary level is already rather dense as well, and that more content around financial literacy would mean that “something else will have to give”.

Even at a polytechnic or university level, Loh feels that efforts may be better spent to pique the interest of young people around financial literacy rather than mandating a course be taken.

“Fundamentally, if there is little to no interest (from the target audience) at the time, it may be difficult to put such a plan into motion,” he says.

📝 A necessary goal

Although a centralised approach to financial literacy education presents challenges, Tan stresses that it is still a necessary goal.

“Just as early health education promotes lifelong well-being, early financial education can set a valuable foundation for young adults,” she says.

To Giam, the earlier students understand the basics of financial literacy, the better prepared they’ll be to avoid financial pitfalls as adults.

There is evident value in exposing young people to financial literacy – be it in school, through an enrichment class, or via personal reading and research. Here are some basic concepts that could be helpful to get you started on your financial literacy journey 🔢:

- The power of compounding: Compounding occurs when an investment grows as the initial sum of money, and the accumulated interest or returns generate earnings over time. Money grows faster in this way as returns accumulate on both the initial sum and its returns. Starting early and regularly contributing to savings or investments can amplify the benefits of compounding over long periods of time.

- The interplay between investment risk and reward: Every investment carries a certain level of risk, and higher-risk investments can offer higher potential returns. Beginner investors should assess their risk tolerance, time horizon, and financial goals to create a balanced portfolio that aligns with their comfort level. These can range from low-risk options such as government bonds, to higher-risk assets such as technology stocks.

- Understanding CPF: CPF is Singapore’s mandatory savings scheme, with contributions from employees and employers. The funds are split across three accounts: Ordinary, Special, and MediSave, and they help citizens save for retirement, healthcare, and housing. CPF savings can also be invested through approved schemes.

- Learning how taxes work: Singapore has a progressive income tax system, with higher-income earners paying higher tax rates. In addition to personal income tax, other taxes include a goods and service tax (GST), property tax, and stamp duty.

No one’s telling you to become a day trader at 15 years old, but getting a head start on financial literacy reaps clear benefits. After all, trigonometry may not help you make sense of your first pay cheque 💵, but the concepts of budgeting, saving and investing will.

TL;DR

- Young adults today are expressing the desire to be more financially savvy and better prepared to handle the rising costs of living

- An early introduction to topics such as CPF, interest rates, taxes and housing loans could keep students in touch with the real-world applications of what they’re learning

- Establishing a standardised syllabus on financial literacy across tertiary institutions may prove difficult, as each school may have differing areas of emphasis within the course

- Regardless, getting young people started on financial literacy early – in whatever shape or form – is beneficial for their long-term financial planning

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.