Fixed income portfolios in a new era: the prospect of real, positive income

They can appeal to investors who are looking for income generation, duration and diversification

MUCH has been written about the attractiveness of current bond yields and the potential for strong absolute returns as monetary policy becomes looser. However, not as much attention has been drawn to the long-term consequences of the sudden end of the low-yield era.

Currently, US government bonds pay a positive real (inflation-adjusted) yield, have a more symmetrical risk profile, can perform a wider range of functions and offer more opportunities in a diversified portfolio.

Indeed, fixed income is back – not just as a tactical investment in the coming quarters, but also as a strategic opportunity for investors. For the first time in 10 years, it can appeal to a wide range of institutional investors who are looking for income generation, duration and diversification.

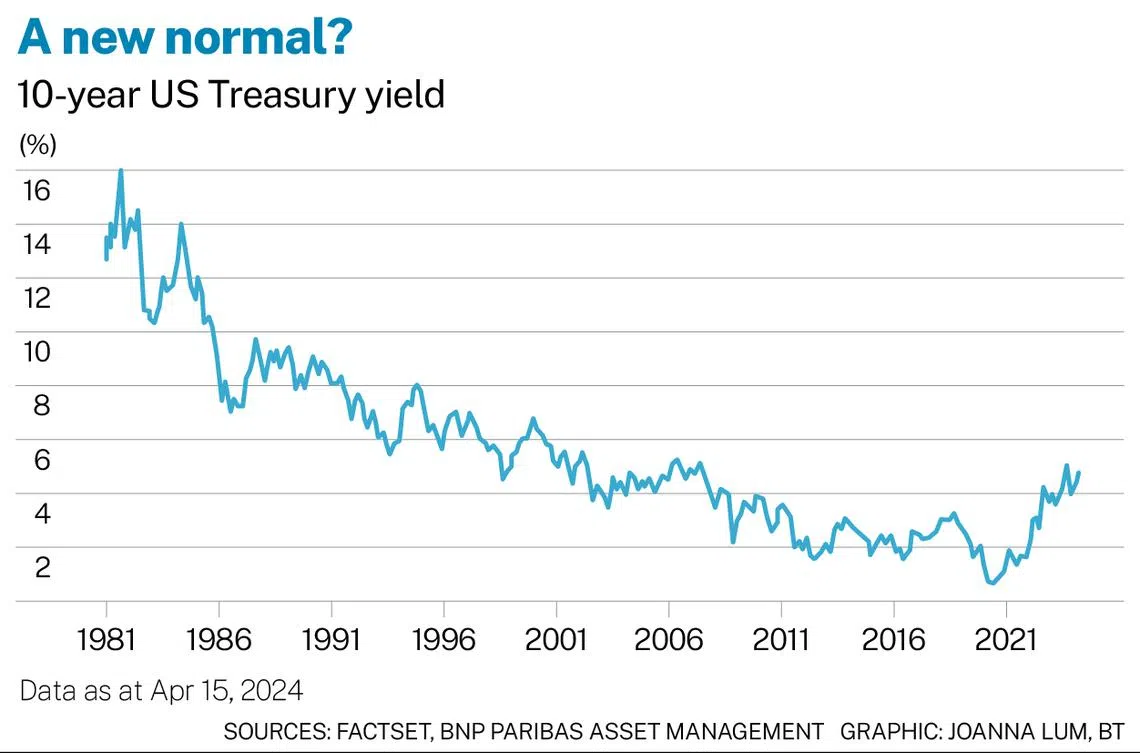

Fixed income from 1981 to 2021

Between 1981 and 2011, when active fixed income investment management began, and the modern notion of investing in a diversified fixed income and equity portfolio became widespread, bond yields rose and fell with each economic cycle.

Overall, they were on a steady downtrend. The yield on 10-year US Treasuries slowly fell from about 16 per cent in 1981 to just under 2 per cent in 2011.

Despite short-term fluctuations, these 30 years became the golden age of fixed income. Adding a large number of fixed income securities to a diversified portfolio became common sense.

However, between 2011 and 2021, both inflation and bond yields began to run out of room to fall. Japan was the first economy to set the policy interest rate at zero, an example followed around the world.

Numerous theories emerged on the reason why. Most were based on the idea of a “new normal” in which bond yields would remain low for some time, as deflationary trends were too potent and widespread. A consensus view emerged that central banks did not have sufficient capacity to create inflation, a problem exacerbated by the aftermath of the 2007 to 2008 global financial crisis.

Throughout these years, investors’ need for income generation did not change. While few questioned the idea that fixed income still offered diversification advantages, low returns led investors and companies to opt for riskier fixed income assets, complex structured products, or a combination of both.

Now that investors are wondering how fixed income may evolve from here, we believe that we should not consider either of these periods as “normal”. Nor should we think that the asset class must necessarily return to one or the other in the next 10 years.

Today’s high bond yields are the direct result of rapidly rising inflation – to levels unimaginable just five years ago – and central banks’ response with the fastest and most aggressive interest rate hikes in decades. However, even at the risk of stating the obvious, nothing else has changed.

Portfolio construction

In our view, we need to reassess the assumptions underlying the role of fixed income in a diversified portfolio. In other words, what is the optimal exposure to fixed income when yields are not in a downtrend and are not staying low for a long time?

To us, the answer is surprisingly simple once you accept that fixed income is not going to offer a steady capital appreciation, and that returns need not always be near or below zero. In the coming years, the performance of fixed income could look more like what is theoretically considered normal. They will be securities with a positive real return that will rise and fall with the economic cycle, and offer diversification from equities.

Moreover, if we are correct in thinking that central banks intend to maintain positive inflation, have the means to do so, and that markets will view the risk of higher inflation as a result of external shocks as a viable threat, real rates should remain positive in the foreseeable future.

Thus, the fixed income universe could once again offer real income to investors, savers and financial institutions, such as pension funds and insurance companies. These groups may no longer have to take on excessive credit or illiquidity risks to obtain a reasonable real income.

While the slopes of the yield curves for major developed countries are not trending upwards just yet, we think they will as the need for tight monetary policy diminishes. Thus, investors could once again access the roll-down effect, that is, the appreciation of capital as bonds approach their maturity date.

However, the outlook for fixed income may be more straightforward. A consistent feature in both the “golden age” of fixed income and the “lost decade” – and not something we expect to change in the next 10 years – is that yield is often the factor that mostly determines the return over the life of the bond.

The current yield on 10-year US Treasuries stands at around 4.6 per cent, making them attractive for both long-term (10 years) and short-term investment. Even considering the volatility around the long-term average expected return, we believe a long-term annual return above 4 per cent is attractive for government bond exposure.

Investing in the new era

It remains to be seen what the new normal will be. But we believe it will be characterised by an average return that is higher than that recorded in the past decade. We will not see the steady appreciation of capital that we saw in the previous 30 years.

Markets and experts have been focusing on the short-term opportunities offered by fixed income, but we think there is a danger that we are losing sight of a bigger issue: Many of us have spent the past decade thinking that central banks were entities working to create inflation, but, today, investors should start looking at central banks as entities that could, again, manage the level of inflation.

If we are right, a surprisingly wide range of investors could find much more conventional means of meeting their needs than by taking on more risk.

The writer is global head of fixed income, BNP Paribas Asset Management

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services