Positioning for 2025: Take advantage of market corrections

Volatility will be the name of the game this year, so investors will need to be nimble with asset allocation

AS WE enter 2025, Donald Trump returns to the political stage, a new round of trade war is imminent, and inflation risks are re-emerging. What kind of world should we expect? How should investors position themselves?

The economic cycle has always had its ups and downs. Last year, the US was expected to fall into a recession from the higher rate environment. However, the economy successfully achieved a soft landing. Technology-related expenditures rose sharply, thanks to the boom in artificial intelligence (AI), which gave new impetus to the US economy. Furthermore, the expansionary policy in the US was also supportive.

Recession not on the cards for US

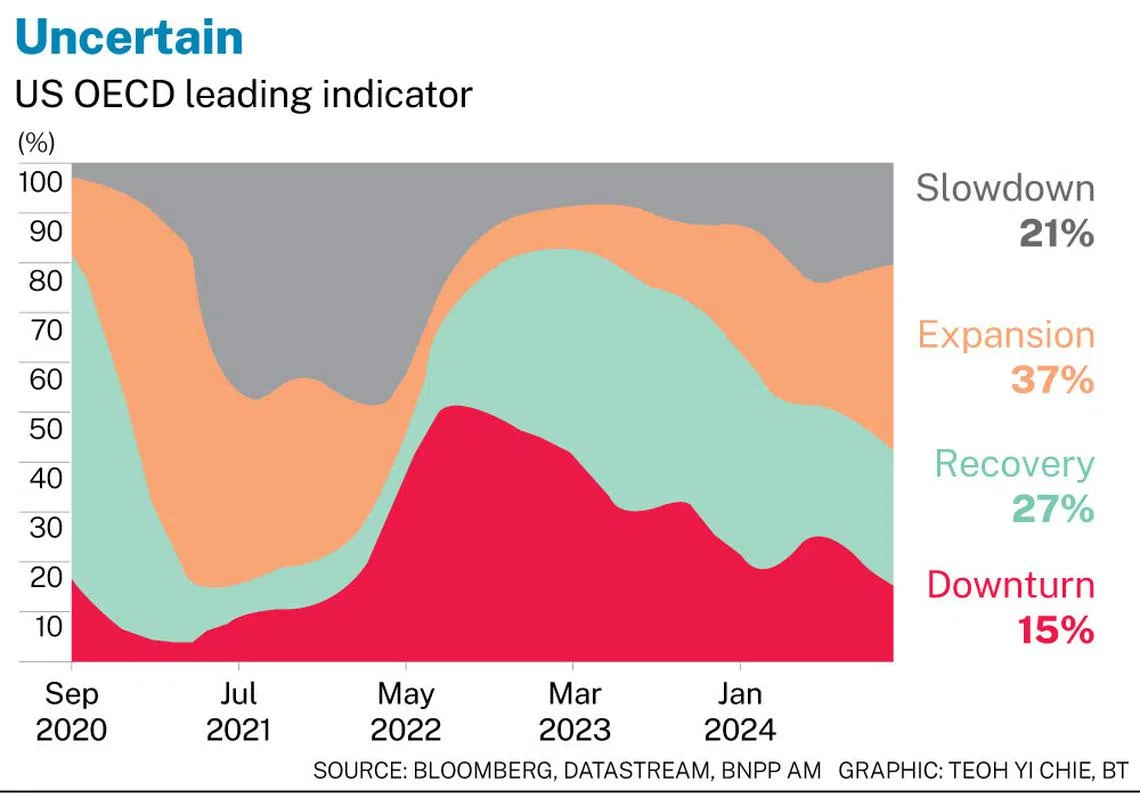

This year, the US OECD Leading Indicator, an index that flags early signals of inflection points in business cycles, reflects a rather mixed and uncertain situation. It seems that the probabilities of economic slowdown, expansion, recovery or downturn are all about the same. I believe that the US will most probably not experience a recession, but growth will slow.

AI spending may slow down, but its application has begun to penetrate different industries. The beneficiaries are not limited to technology giants, but would include companies of all sizes, bringing structural impetus to US productivity.

However, it is difficult to predict the direction of the US government’s fiscal spending. The current fiscal deficit in the US is as high as 6 per cent of GDP. Trump, soon to be inaugurated as president, is a populist leader who claims to help people alleviate cost-of-living pressures.

US Treasury Secretary-designate Scott Bessent, however, attaches great importance to fiscal discipline. He has proposed a “3-3-3” policy – lifting GDP growth rate to 3 per cent, increasing daily oil production by 3 million barrels, and keeping the budget deficit at 3 per cent of GDP. In other words, there will be some sort of tug-of-war between him and Trump.

The president-designate has also appointed the billionaire Elon Musk to lead the newly established Department of Government Efficiency (DOGE). This means that manpower in the public sector might be scaled back. This might impact the job market; recruitment activities in the past few months were, after all, driven by the public sector.

However, the US is likely to avoid a recession because the finances of US households remain quite healthy. Both the household debt-to-income ratio and interest burden are lower than before the epidemic. However, corporates may face some pressure.

In the next few years, US companies will need to confront a “maturity wall”, that is, the large amount of debt that is about to come due, and the interest rate-hike cycle of the past few years may affect the company’s future debt repayment ability. However, as long as the US consumers stay strong, we believe the overall problem will still be minor.

Tariffs: a dynamic game

Of course, Trump’s tariff policy remains the biggest concern for investors. I believe that the impact of tariffs on inflation and interest rates can be analysed from three perspectives. First, from the supply side, there is no doubt that raised tariffs will drag down the global economy. Coupled with Trump’s anti-immigration policies, they are likely to affect the supply side of the economy and fuel inflation.

Second, tariffs may also dampen consumer sentiment and even create a stagflation environment.

Third, Trump is a businessman and sees himself as a “master of deals”. Before taking office, he constantly threatened to impose additional tariffs, which may be just his first step in negotiations. It can be inferred that the US’ imposition of additional tariffs will inevitably trigger reactions from other countries. China is unlikely to accept it unconditionally.

You might have noticed that since last September, China has launched a series of measures to stimulate the economy and stabilise the financial market; its policy narrative has also undergone fundamental changes.

Beijing also recently sold off US Treasury bonds on a large scale. All these signs make us think that the trade war is not a “one-step” game, but a dynamic game that changes with the situation.

In terms of monetary policy, after the latest Federal Open Market Committee (FOMC) meeting, the market expected the Federal Reserve to turn from dovish to neutral. The chance of a major interest rate cut was reduced, and US bonds and stocks were also sharply sold off.

Stocks: optimistic about US and China

Instead of selling off with the herd, we took the opportunity to increase our holdings of some US assets on a tactical basis. In fact, the economic indicators for the US in the past few weeks have been quite good. For example, retail sales and business spending have improved, indicating healthy economic activity. The US economy seems to be slowing down rather than declining.

Therefore, taking advantage of the market correction and making corresponding arrangements may bring us more opportunities. For example, US financial stocks are expected to benefit from the prospect of rising inflation. Due to factors such as increased corporate merger and acquisition activities, earnings per share of the US financial industry will outperform the overall market.

It is worth noting that we have also become interested in Chinese stocks. Our analytical framework is based on four pillars – fundamentals, policies, market sentiment and valuation. In our view, China’s stock market is driven by policies and sentiment, both of which are currently supportive of forward returns.

The Chinese government has launched a number of stimulus measures, and the authorities have actively expressed support for the economy and financial markets. In fact, China’s stock market trading volume and the number of people opening accounts rose in recent months, which shows that market sentiment has greatly improved. I believe that the authorities do not want people who have entered the market in the past few months to suffer a negative wealth effect, which will subsequently affect market confidence.

In terms of fundamentals, China’s manufacturing purchasing managers’ index (PMI) and automobile sales have improved, and the real estate market has stabilised, although levels of activity are still very low. The current valuation of A-shares is at its lowest level in 10 years. From a risk-adjusted return perspective, it seems to be a good entry opportunity.

Although the market is worried about the trade friction between China and the US, we maintain a positive view on the Chinese stock markets, based on the above-mentioned favourable factors. However, we believe that China will fully launch fiscal stimulus measures only after announcing the results of its tariff negotiations with the US.

Gold supported by demand

In addition, I believe that the investment prospects of gold in 2025 are also quite attractive. In the face of an increasingly polarised world, as central banks strive to diversify their reserves, gold has become a reasonable alternative.

Furthermore, the worsening of the US fiscal deficit in recent years has caused the rest of the world to question the status and stability of the greenback as a major reserve currency. In view of this, many central banks have increased their purchases of gold in recent years.

In the face of continued geopolitical tensions, gold can serve as a hedge. Inflows into gold exchange-traded funds have been rising steadily over the past 10 years, showing that market demand continues to trend up. If Bessent as US Treasury Secretary really implements a tightening fiscal policy and reduces the fiscal deficit to 3 per cent, the US may need to devalue the US dollar to support the economy. This will further support gold, silver, and even gold-mining companies.

In conclusion, we think volatility in both macroeconomics and market prices will be a key feature of 2025. Investors need to be nimble in their asset allocation.

The writer is head of dynamic multi-asset, BNP Paribas Asset Management

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services

TRENDING NOW

What makes a good job? Feeling that you matter

DeepSeek founder Liang Wenfeng becomes the world’s richest AI model creator

When the disruptor gets disrupted: How Chinese open-source AI is eating its own industry

A new kind of ‘ceasefire’ between US and Iran where talks, strikes are part of the same process