Dollar-cost averaging and compounding: low-risk, easy strategies for new investors

For some of us, accumulating a S$1-million portfolio might seem rather far-fetched, but this is achievable following these two principles

Claudia Tan HS

MANY of us may not think twice about shelling out for a holiday. Yet when it comes to investing, we might be a tad more hesitant to part with the money.

Indeed, a Bali getaway brings about immediate gratification. Investments, on the other hand, do not guarantee returns right away. Plus, the thought of losing money - not cool.

But investing does not always have to be super risky, nor require lots of cash. If you do not have the confidence or financial means to immediately part with a lump sum to invest, the dollar-cost averaging strategy is an effective, conservative way to get started.

What is dollar-cost averaging?

It means investing a fixed sum into a chosen asset at regular intervals over a period of time. These purchases take place regardless of the price of the asset. The result? You end up with more shares when prices fall and fewer shares when they rise.

Dollar-cost averaging is typically used for investing consistently in the broad market, to smoothen out potential volatility and limit losses from an ill-timed investment.

If you use dollar-cost averaging to invest via a passive index fund, an exchange-traded fund or an actively-managed mutual fund, you also get to skip the work that goes into picking specific stocks. And you will reduce your risk. Some initial research is still required to pick the fund you want to invest in, but it is a more manageable process even for newbies.

How it works

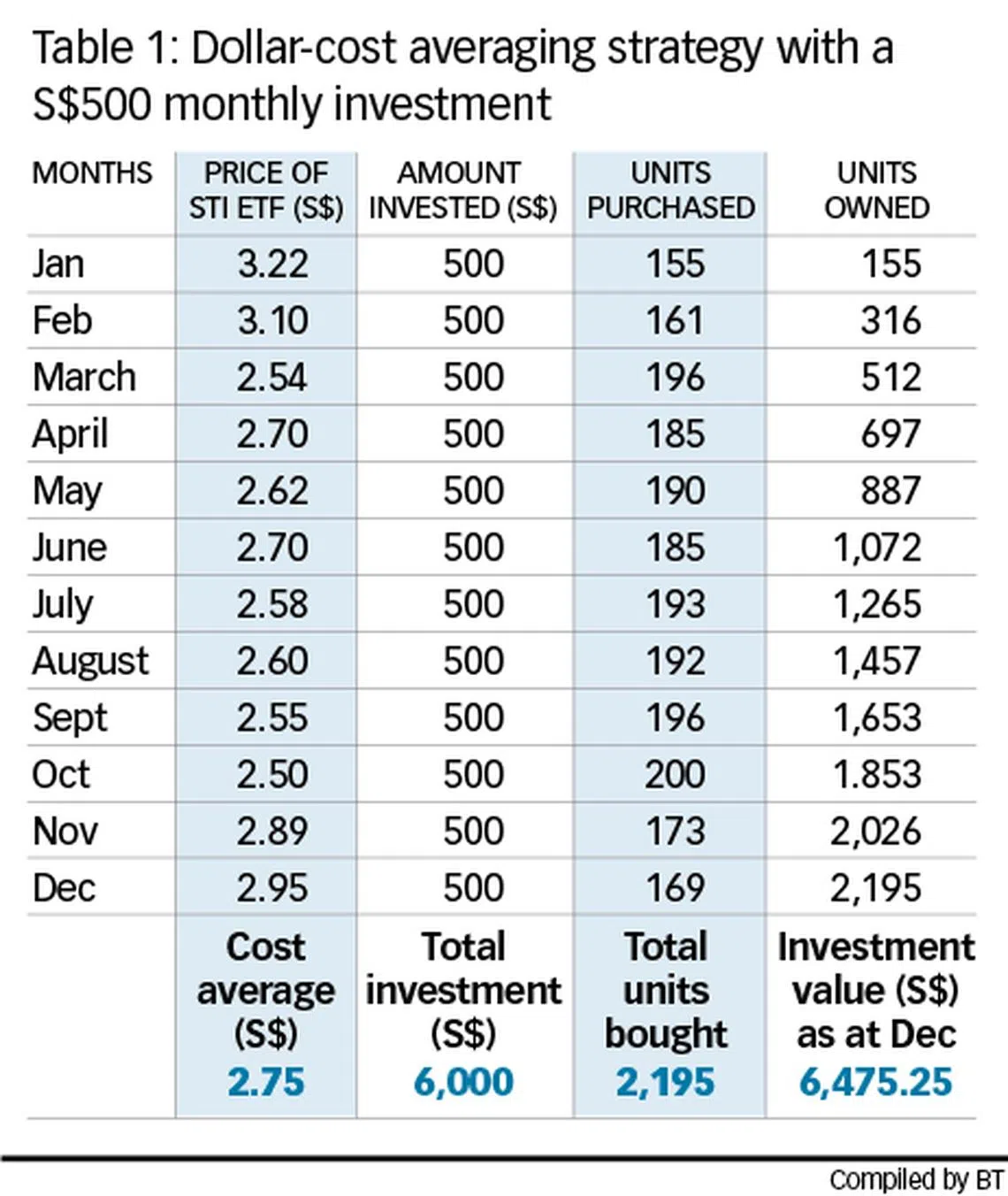

For example, instead of buying S$6,000 worth of shares or fund units at one go, you buy S$500 worth of shares or units every month over a period of 12 months - ideal for those who do not have a huge capital set aside for investments from the get-go.

The table illustrates how money could be put to work over a period of 12 months.

Based on the table, as long as the price of the fund increases over the 12 months, there will be a positive return on investment with dollar-cost averaging.

Meanwhile, if a lump-sum approach was used and all S$6,000 was invested in, say, January or February, there would be losses and it could be tempting to quickly sell off one's holdings to minimise losses.

Conversely, accurately timing the market and dumping a lump sum during the March-low would translate to much higher returns than the dollar-cost averaging strategy.

But in reality, that would have required much foresight and it is not always easy to stay invested when markets fall.

The power of compounding

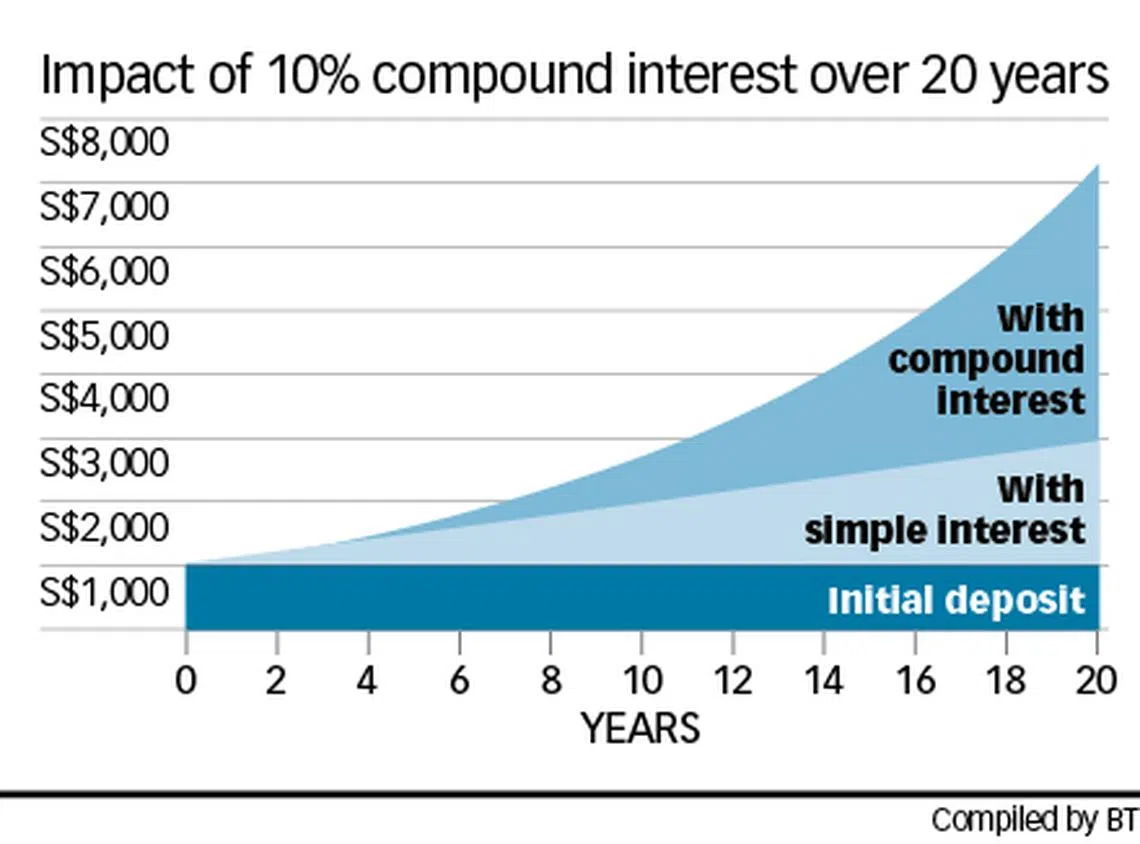

Setting aside a fixed amount to invest regularly will also help with compounding. Simply, it means generating additional returns from prior returns.

Such an effect can be observed from interest generated by deposits into your savings account. By leaving the earned interest in your account instead of withdrawing it, you will generate interest on that interest too. This can have a powerful effect on your savings.

The chart illustrates how compound interest will give your savings a boost in the long-run with a starting amount of S$1,000.

The same compounding power applies to investments. If you invest regularly, and reinvest the dividends from your investments, your portfolio will grow more quickly.

Consider, for instance, an investment in the S&P 500 Index ETF. Over the last 10 years, the index has gained 237 per cent. And if dividends were being reinvested, returns would rise to 313 per cent.

Putting the two together

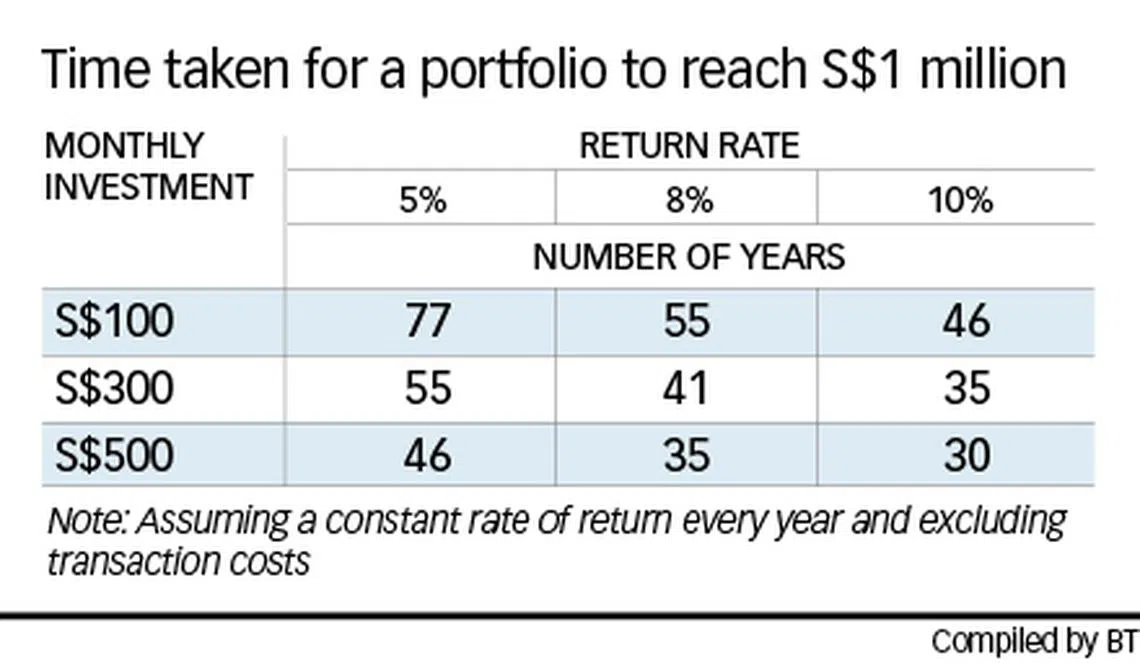

For some of us, accumulating a S$1-million portfolio might seem rather far-fetched. But this is in fact achievable with the principles of dollar-cost averaging and compounding.

If you start with S$300, and you invest S$300 monthly for 40 years, assuming a rate of return of 8 per cent every year and not taking into account transaction costs, you will end up with just under S$1 million - with a total investment of S$144,000.

For context, the average annual return of the S&P 500 over the last 40 years is nearly 12 per cent. The average annual return of the STI since its revamp in 2008 is close to 8 per cent.

If you can afford to invest more, a monthly investment of S$500 at the same rate of return would take a little over 34 years to hit S$1 million.

A conservative strategy

Dollar-cost averaging works well assuming that prices will eventually rise. But it is by no means a fool-proof method that guarantees returns. You may still wind up with losses if you do not do your due diligence in selecting an appropriate asset to invest in.

The dollar-cost averaging strategy might therefore work better on passively-managed index funds that track an entire market. If you're just starting out, with not a lot of savings to spare, dollar-cost averaging is a conservative strategy to kickstart your investing journey.

- This is the third instalment of Invest & Grow, a weekly 10-part series that aims to help new investors get started on their investment journey.

READ MORE:

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services

TRENDING NOW

Yeoh Pei Xien: YTL’s third-gen scion with a pastor’s heart

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Keppel H1 net profit drops 59% to S$155 million on impairments, M1 deal fallout; shares fall 4%

Singtel explores Nasdaq-SGX dual listing for data centre arm Nxera, local data centre Reit