Plan ahead before joining the Great Resignation

Knowing how to grow and protect your wealth early is crucial in ensuring a comfortable life in your later years

Thinking more deeply about work-life balance and job satisfaction is a positive trend. But if job breaks are not properly planned for, they can cause unanticipated stress.

For instance, a rising number of those caught in the so-called Great Resignation wave also face difficulties when it comes to planning for retirement.

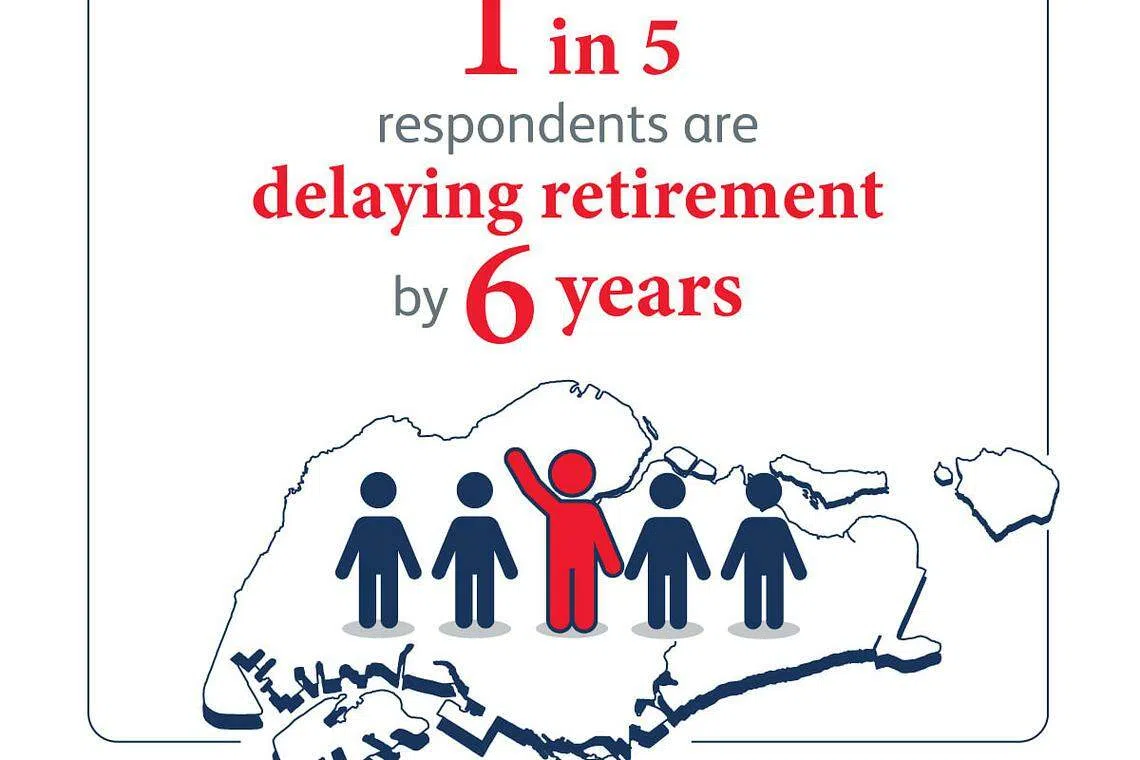

According to a poll commissioned by Prudential Singapore in April 2022, one in five respondents who had resigned or intended to resign said they have had to push back retirement by six years - from the originally planned age of 58 to 64.

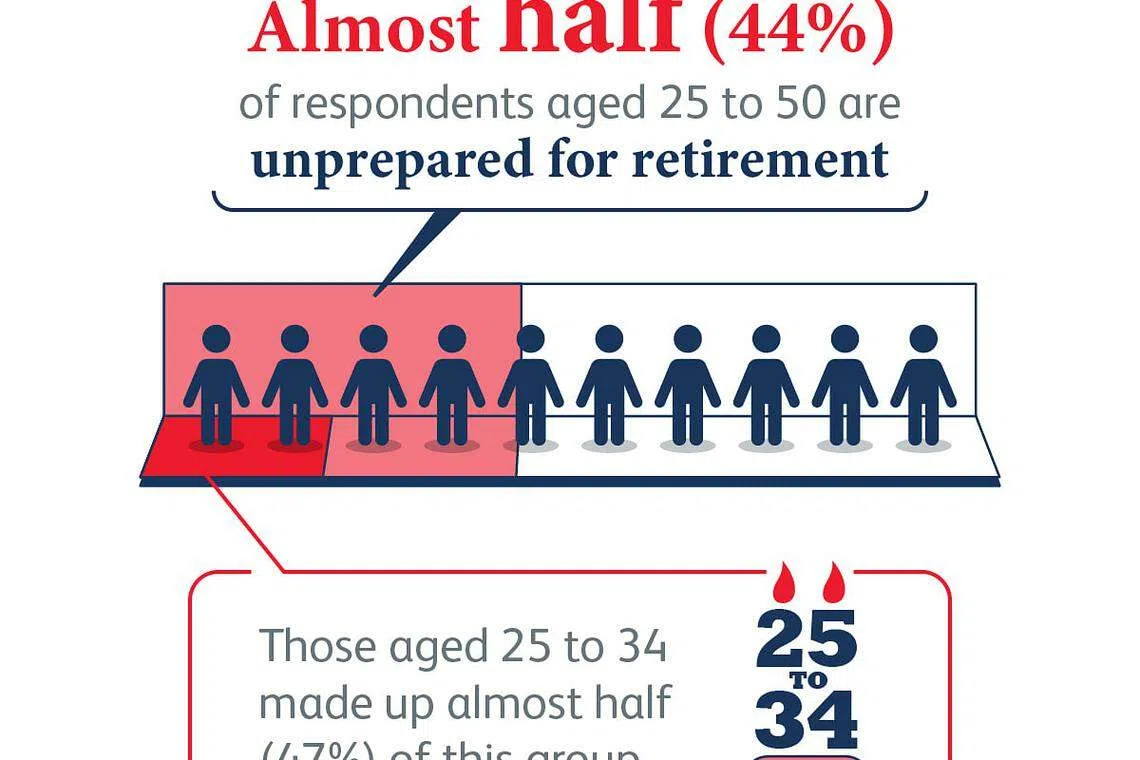

The poll also found that almost half, or 44 per cent, of the 1,000 respondents aged 25 to 50 are unprepared for retirement. Those between the ages 25 and 34 make up 47 per cent of this group.

More than eight in 10 respondents are worried about the rising cost of living due to inflation while 81 per cent are concerned by rising healthcare expenses.

"Many people leave their jobs to recharge and rejuvenate. However, without proper financial planning, a career break can result in greater stress and adversely impact one's retirement plans," says Mr Dennis Tan, Prudential Singapore's chief executive officer.

"It is concerning that nearly one in two respondents are unprepared for retirement. With rising lifespans, Singaporeans need to accumulate an even bigger nest-egg so as not to outlive their savings," he says.

Managing the financial impact

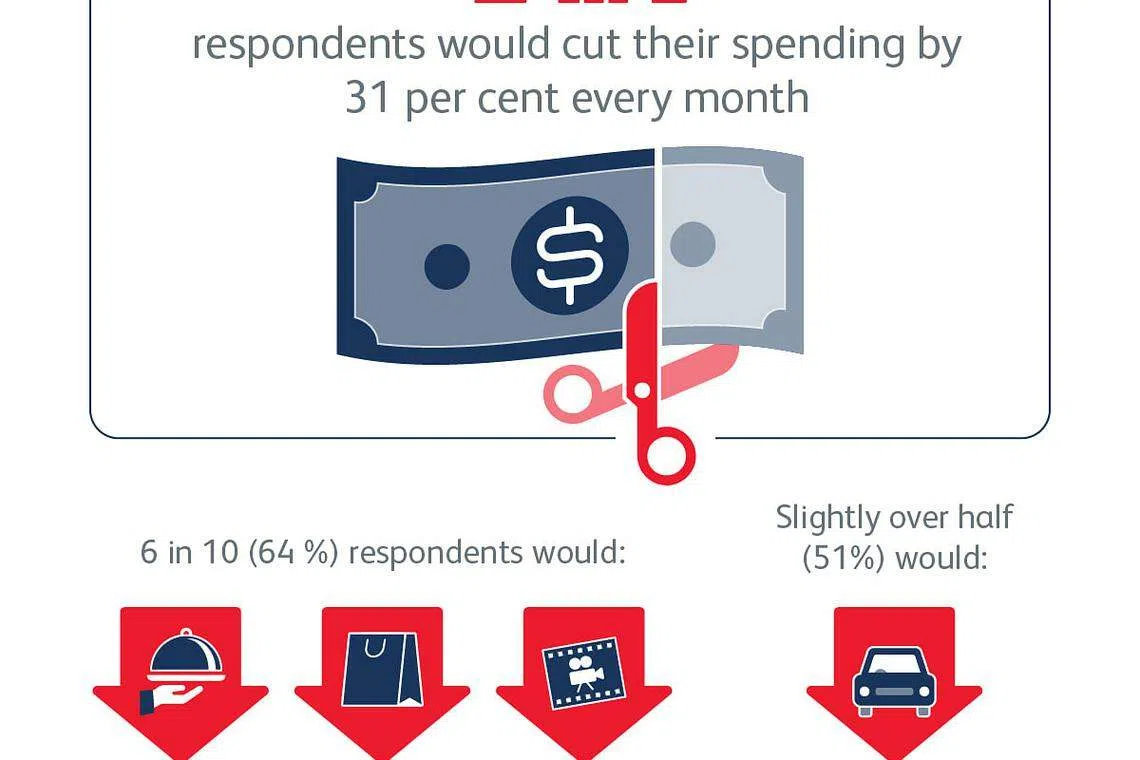

Half of those polled said they would shave monthly spending by about a third, or 31 per cent, to deal with the financial challenges that come with career breaks.

Sixty-four per cent adjusted their lifestyles by dining out, shopping, and watching movies less frequently, while slightly over half, or 51 per cent, of the respondents said they cut down on cab rides and opted instead for more affordable forms of transportation.

Despite the financial implications, 52 per cent of poll respondents who resigned said they no longer felt engaged at work, while 38 per cent were looking out for better career prospects.

Thirty-four per cent said they wanted a break for mental wellness, while the same proportion said they wanted to leave toxic work environments.

Diversify to make your nest egg more robust

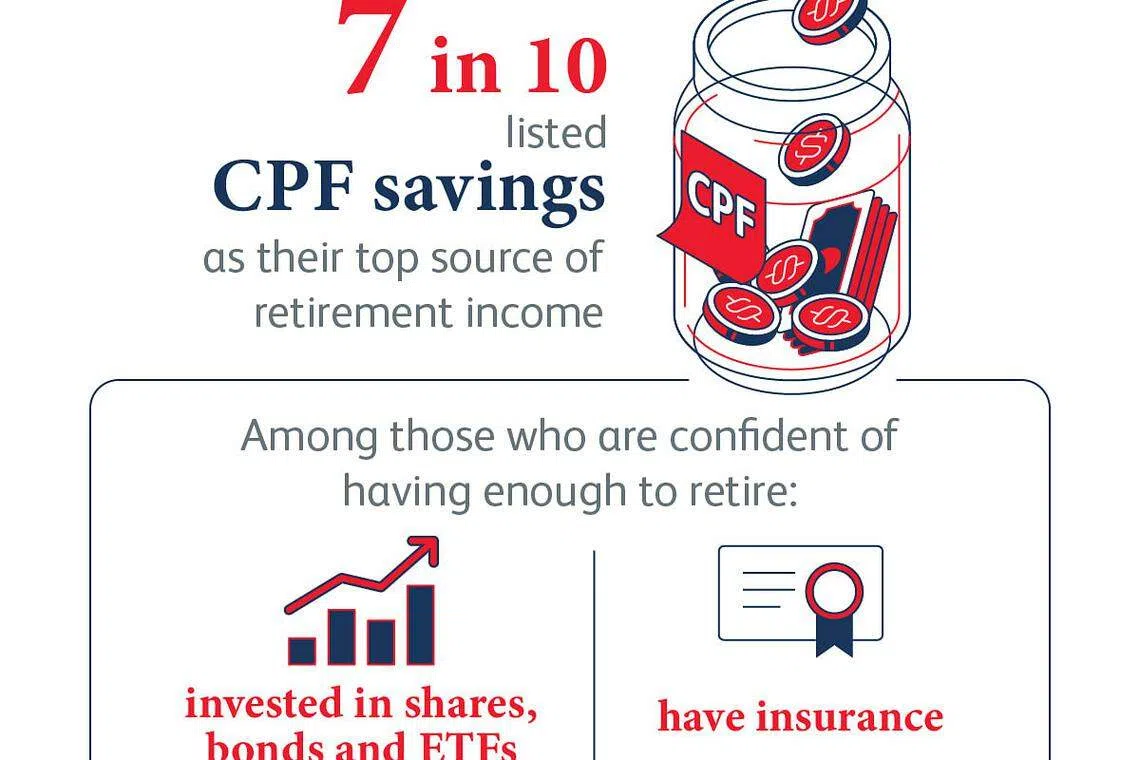

When it comes to funding their retirement, most Singaporeans depend on the Central Provident Fund (CPF) and bank savings, the poll found. Over seven in 10 respondents, or 73 per cent of them, listed CPF savings as their top source of retirement income.

But diversifying into other financial instruments have put some respondents in better stead for retirement.

Sixty-eight per cent of respondents who expressed confidence in having enough to retire said they invested in shares, bonds and exchange-traded funds (ETFs). Forty-six per cent of this group also have insurance.

On the other hand, only half of the people who felt unprepared for retirement have investments, while 36 per cent have insurance.

Mr Tan advised Singaporeans not to put all their eggs in one basket.

"Putting your money in different financial instruments, instead of only relying on savings, is important for retirement planning. Diversifying your portfolio also helps spread risk and smooth out volatilities during challenging market conditions," he says.

Make a plan

"Regardless of how you plan, it is important to start planning early so you have a longer runway to grow your retirement funds," he adds.

There is no "one size fits all" retirement plan. The first thing you need to determine is your desired retirement age, which will guide your decision regarding the duration of payouts you would like to receive, Prudential says.

Common options include retirement plans with regular payouts over a predetermined period, such as 10, 15 or 20 years. Such plans aim to provide a steady stream of retirement income. These plans may include customisable features, such as payout duration and the amount of income paid out monthly.

If you are looking to retire earlier, you will need a plan that offers payouts over a longer time period, to ensure you have a steady source of income during retirement.

Those who prefer higher yields can consider investment-linked policies, often known as ILPs, which have both a life insurance and investment component. Premiums paid for this policy would be invested in sub-funds. Some of the investment units will then be sold to pay for insurance.

Knowing your dependents' needs - such as parents' physical and financial health, as well as how you would like your children to be educated - will also help one choose financial products to better plan for future financial needs. For example, those who plan to spend on big-ticket items such as a retirement holiday or funding their children's overseas university education may consider plans with a lump sum payout.

Putting a wealth and retirement plan in place will help you make big decisions, including career breaks, with confidence and clarity.

Learn more about the wide range of annuity and retirement plans available to you here.

Disclaimer:

This article is for your information only and does not consider your specific investment objectives, financial situation or needs. We recommend that you seek advice from a Prudential Financial Consultant before making a commitment to purchase a policy. Information is correct as at Oct 6, 2022.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services