Why investors should not ignore bonds in a rising-rate environment

THE US Federal Reserve is clearly in an inflation-fighting posture. In the June FOMC meeting, the Fed raised its target rate by 75 basis points, a move last made in 1994. Additionally, the latest Fed’s “dot-plot” also pointed to a quickened normalisation pace with policy rate expected to reach 3.375 per cent by the end of this year, and 3.75 per cent by 2023.

If we reference this with the widely accepted “neutral” rate of 2.5 per cent, which is the level of interest rate that neither accelerates nor restrains the economy, it is clear that monetary policy will definitively turn restrictive by September. On top of interest rate policy, the Fed will also be reducing the size of its balance sheet by US$95 billion a month, eventually trimming an aggregated US$1.5 trillion off its balance sheet by end-2023.

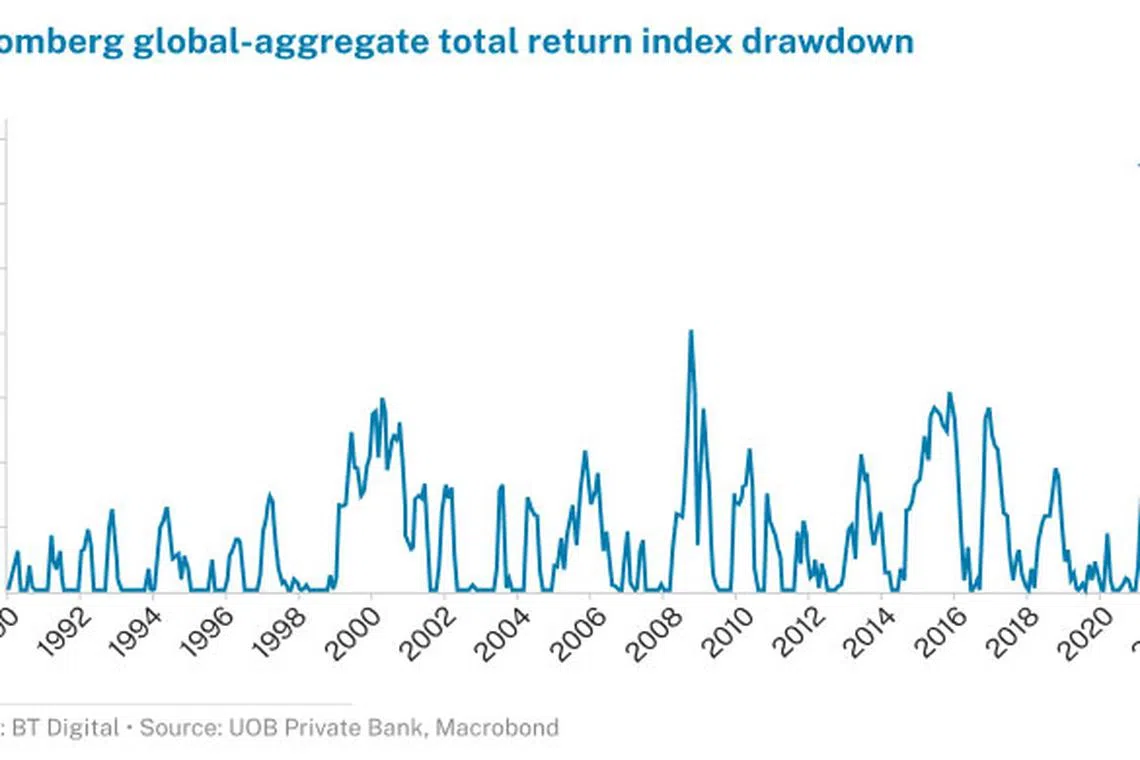

The Fed’s sudden pivot to become an inflation fighter has caused a rout in the bond market. The latest Bloomberg Global-Aggregate Total Return Index shows a 15 per cent drawdown of a broad global fixed income index, the highest level since its inception in 1990.

The May Consumer Price Index (CPI) was also of some concern to the Fed, given the 5.2 per cent surge in Owner Equivalent Rent (OER), a highly persistent and significant component of the CPI basket. As the Fed continues to be behind the curve, its last line of defense lies in anchoring inflationary expectations to preserve its credibility. The key implication is that the Fed will continue its hawkish rhetoric in the near term even in a softening economy. However, as soon as initial signs of a moderation in inflationary pressures surface, the Fed will also be quick to pivot in response to a slowdown.

Why should investors be looking at fixed income in an environment of rising interest rates?

Many sectors of the fixed income market have suffered a sell-off not seen in decades, and as prices fall, yields correspondingly rise. For example, the 5-year US Treasury yield has risen from 1.26 per cent at the start of the year to 3.2 per cent. Correspondingly, corporate bond spreads have also widened. For the same period, the yield-to-maturity for Asia investment-grade corporate bonds has risen from 3.2 to 5.2 per cent. With higher government risk-free yields, investors do not need to buy lower credit quality or longer maturity bonds to earn a reasonable level of yield, which was not the case just a year ago.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

Even as the Fed is projected to continue raising policy rates, long-term interest rates are likely to rise, but at a slower pace compared to short-term interest rates. As the US economy is already in late cycle, Fed tightening will slow the economy and reduce long-term inflationary risks, both of which will be reflected in long-term yields.

Notably, fixed income as an asset class plays an important role in an investor’s portfolio, as it generates regular cash flow. With lower volatility and correlation with other risky assets such as equities, high-quality bonds can reduce the overall volatility of the portfolio. In times of acute stress or recessions, high-quality bonds have a good track record of being an effective diversifier, with the 2008 global financial crisis being a good proof point as US Treasuries were one of the very few assets that rose during those turbulent times. Bonds also tend to recover faster. Historically, bond markets can have negative total returns for a year, but can turn positive in the next. Hence, having fixed income in one’s portfolio offers psychological comfort and liquidity during a volatile and uncertain market environment. When risky assets eventually bottom out, investors can rebalance their portfolios to pare down some bonds holdings to take advantage of market opportunities.

For investors who are concerned about rising interest rates, there are a few simple strategies that can be deployed to lessen the impact. First, investors can purchase short to intermediate duration bonds or bonds with floating rate or reset features, as the shorter maturity reduces sensitivity to rising interest rates. However, call features are usually at the issuer’s option, and will be exercised if it is in its self-interest, or based on economic or reputational reasons.

Second, investors can take some credit exposure which pays above the risk-free yield. The additional credit spread compensates investors for bearing credit risk that is not directly influenced by interest rates. However, as the economy slows or enters a recession, credit spreads can widen, translating to marked-to-market losses. Hence, given the prospect of a slowing global economy, investors should ensure that exposure to weaker credits and high yield should be limited. However, there are selected opportunities in Asia’s high yield market given the elevated level of spread (8.9 per cent). Investors could also include subordinated securities of well-capitalised financial institutions as part of a diversified credit exposure.

For credit exposure, particularly the riskier segments, investors should avoid taking concentration risk as credit defaults result in permanent value impairment. Investors should diversify or participate through a collective vehicle.

Finally, investors can ladder up their bond exposure. This entails having a portfolio of bonds with a mix of short, intermediate and longer maturities. As interest rates rise, the maturing bonds can then be re-invested into higher yielding ones.

While bond prices do fluctuate, as long as a bond pays its coupon on time and redeems its principal at maturity, the investor will receive the target returns known at the point of purchase. For income-driven investors, rather than being overly concerned with mark-to-market fluctuations, visibility of cash flow should be the key focus. That surely takes a lot of stress out of investments.

The writer is UOB Private Bank chief investment officer.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.