Is cash king once again?

Heightened market risks may justify holding more cash today. But it should be accompanied by a willingness to redeploy cash into riskier asset classes when opportunities arise.

DeeperDive is a beta AI feature. Refer to full articles for the facts.

CASH can mean different things to different people. Most of us would associate its yield with that on a deposit, but this only partly captures the asset class. Many investors consider fixed income instruments up to 12 months in maturity as a proxy for cash, given that their yield tends to be closely associated with policy rates. Several factors, however, are common across various approaches to cash – perceived safety of the nominal value of principal, easy access to liquidity and, in return for these attributes, a lower yield than on most riskier asset classes.

The case for cash today

In today’s investment environment, a case can be made for a greater-than-usual allocation to cash.

- Yields are no longer zero. The yield on cash is key because it is often viewed as the threshold that other asset classes have to beat. If the cash yield is available with (perceived) certainty, the expected return on any other asset class has to be higher for an investor to take on the additional risks associated with that asset class.

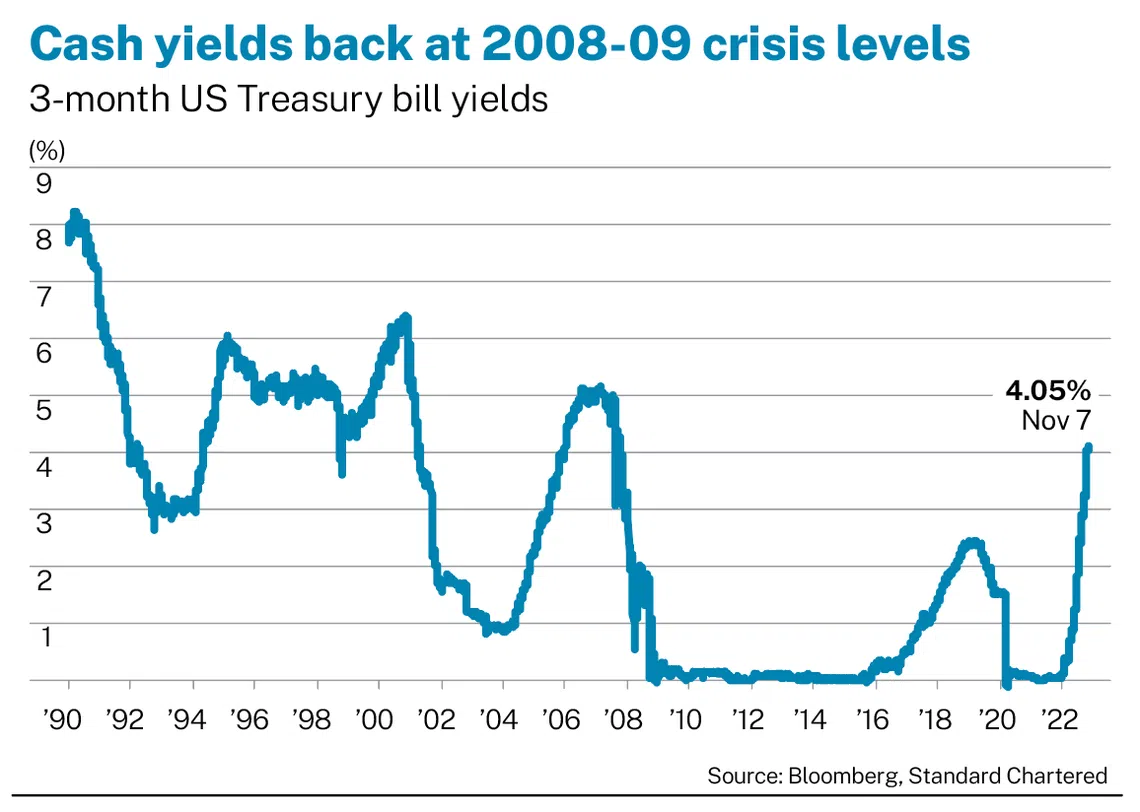

Since 2008 to 2009, this cash threshold was largely zero, which meant there was little reason to consider a significant allocation to cash for purely investment reasons (the Tina or “there is no alternative” argument for riskier assets such as equities). Today, however, the three-month US dollar yield is just above 3.5 per cent and could rise further until the Fed hiking cycle peaks. This significantly raises the threshold for other asset classes and starts to make a more attractive case for cash, relative to other major asset classes.

- Safe haven appeal: In current markets, cash can offer a safe haven amid concerns that the drawdowns in equities and bonds are not yet complete – especially if the S&P 500 takes another leg lower. This argument, of course, would hold regardless of the yield on cash.

The challenges of cash

Given the advantages of holding cash, why not hold much more? We see at least two reasons:

- Riskier asset classes usually pay a premium over cash over the long term: While it may not feel like it this year, over most longer periods, riskier asset classes do indeed pay a premium over cash. This premium can be negative during periods such as today when the market is adjusting to a higher yield on cash, but such periods have been transitory and are usually short-lived.

- Cash can be detrimental to maintaining real purchasing power. Following on from the first point, the yield on cash may be positive in nominal terms, but it remains very negative on real or inflation-adjusted terms. Riskier asset classes can offer a good chance of beating inflation over longer time horizons, but staying too long in cash reduces those chances significantly.

Today, we see a case for holding more cash than usual because of heightened risk of equity and bond market drawdowns, and because cash now pays a positive nominal yield. However, we remain mindful of the longer-term drawbacks of holding cash. Even today, global investment-grade corporate bonds yield around 5 per cent, versus about 3.5 per cent on cash. This is why our preference for cash is accompanied by an active willingness to redeploy into riskier asset classes at the soonest available opportunity.

The writer is chief investment officer for Africa, Middle East and Europe at Standard Chartered Bank’s wealth management unit.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.