Asian utilities slow to confront climate risk

ASIA might need to grow up when it comes to protecting its power sector against climate-related loss and damage, a new report has suggested.

Eleven major power-sector players in Asia are currently losing US$6.3 billion a year to climate-related asset damages and business disruptions, says report authors MSCI and the Asia Investor Group on Climate Change (AIGCC). The annual cost could climb 33 per cent to US$8.4 billion by 2050.

A major theme in the report’s findings are “maturity gaps” in the level of preparedness among the utilities.

In essence, while there is generally acknowledgement of climate risks in the sector, most companies have yet to turn that recognition into more concrete action. These actions could include quantifying the risks, allocating resources towards addressing those risks, and developing systemic solutions.

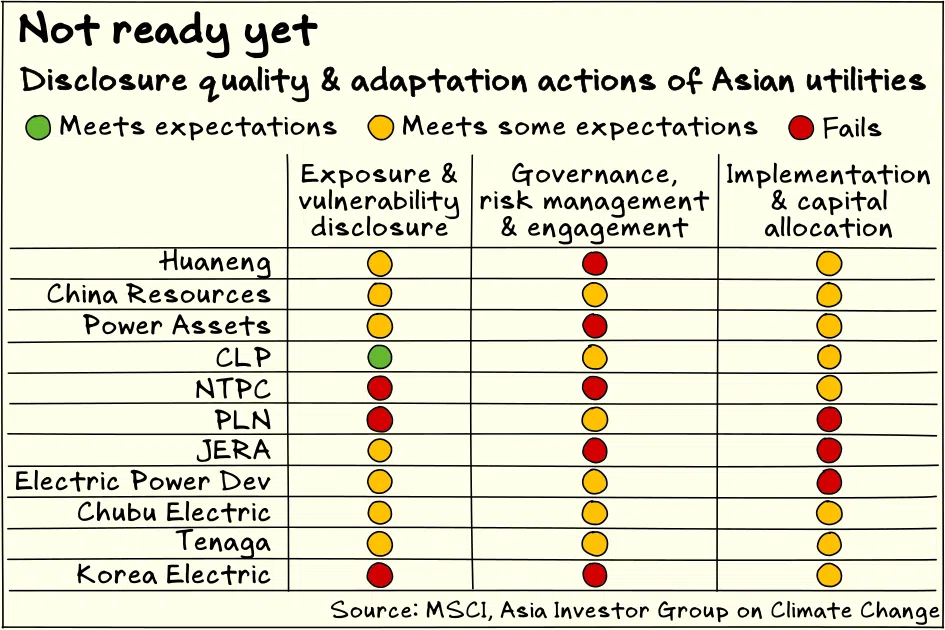

The report focuses its analysis on 2,422 power generation assets owned by 11 utilities: China’s Huaneng Power International Inc and China Resources Power Holdings; Hong Kong’s CLP Holdings and Power Assets Holdings; India’s NTPC; Indonesia’s PT PLN; Japan’s JERA, Electric Power Development and Chubu Electric Power; Malaysia’s Tenaga Nasional; and South Korea’s Korea Electric Power

Together, the analysed assets accounted for more than 550,000 megawatts of power generation capacity.

The estimates’ top drivers of damage are extreme heat and precipitation, with 69 per cent of the assets exposed to either or both of those risks by 2050. Extreme heat is expected to account for 55 per cent of total losses by 2050, while precipitation accounts for 21 per cent.

To assess readiness, the authors consider the companies’ practices under three pillars: how well they assess exposure and vulnerability, how well they set up governance and risk management to address the risks, and the strength of their implementation and capital allocation measures.

Using a traffic-light grading system where green reflects satisfactory performance, red reflects no evidence of the relevant practice and amber reflects only partial fulfilment of the criteria, the report rates most of the companies either amber or red on most of their assessment criteria.

The lack of capital allocation planning is particularly glaring, with every company lacking clear disclosures about adaptation capital and operational expenditures.

This is in spite of significantly better performance when it comes to assessing vulnerability and exposure, especially when it comes to scenario analyses. The gap between risk assessment and capital allocation strategies suggests that companies might be underestimating the potential costs and loss of business they face. That gap needs to close.

The report shares some key insights into how the utilities should improve.

Adaptation-mitigation interconnectedness

Climate action is typically classified as either adaptation or mitigation. Adaptation – and resilience – addresses risks, loss and damage from climate change, whereas mitigation aims to reduce the amount of carbon in the atmosphere, either by removing greenhouse gases or reducing the amount emitted.

However, climate adaptation and mitigation aren’t mutually exclusive when it comes to grid resilience.

For instance, many fossil fuel-based power plants are located to optimise access to their fuels and to cooling resources, which can place them close to water sources, on river banks and coasts, the report says. Hydropower plants are by necessity located on bodies of water.

The report notes that hydro, coal and gas power plants tend to cluster along major rivers in Japan, South Korea, South-east Asia and China. Unfortunately, clustering increases the risk of damage – and potentially catastrophic damage – from single extreme weather-related events.

On the other hand, solar power plants do not have to be co-located with water. Adding solar assets to a power system can therefore diversify the geographical risks in a grid, which would improve grid resilience as well as lower emissions in the power supply.

System solutions

Building grid resilience requires a system-wide approach. The report explains that Asia’s power sector requires both climate mitigation and adaptation, and it is therefore important to ensure that solutions for one objective don’t create hurdles for the other.

For example, climate-resilient infrastructure and adaptation investments should not “lock-in high-emissions or high-risk assets”, the report states.

The power sector also touches many parts of society, and the needs of various stakeholders must be considered to achieve and sustain progress.

For instance, phasing out a coal-fired power plant before its operational lifespan should be carried out in a way that addresses the livelihoods of displaced workers in the coal plants and supporting businesses, the cost of replacement power for affected communities, the ecological and land use impact of developing replacement power and so on, and not simply pay off coal plant investors and develop a new renewable power plant.

Market pressure

The fact that AIGCC, an institutional-investor-led coalition that includes prominent organisations such as GIC, is involved in the report should provide economic incentive to Asia’s power-sector companies to address climate risk.

AIGCC is a key driver behind two relevant investor-led corporate engagement initiatives: the Asian Utilities Engagement Program and Climate Action 100+.

Investors have five key expectations for utilities: governance, decarbonisation strategies and scenario analyses, transparency and disclosure, physical risk and resilience planning, and public policy. Of those, physical risk and resilience is underdeveloped, the report said.

“In particular, assessing the complex, location-specific nature of physical risks is still nascent and challenging to address systematically,” the report stated.

This article first appeared in BT’s ESG Insights newsletter on Dec 5.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.