Gold’s epicentre is shifting to Asia, with prices buoyed by regional demand: analysts

It is set to trade near US$4,100 an ounce in H2, unless new factors such as a weaker US dollar push it towards US$5,000

[SINGAPORE] Asia is emerging as the new centre of gravity for the global gold market, with resilient regional demand supporting bullion prices as Singapore and Hong Kong strengthen their gold trading infrastructure.

The shift is happening even as prices retreated by around 25 per cent from a record high of US$5,500 an ounce in January; the metal was trading at US$4,105.44 an ounce as at 6.18 pm in Singapore on Thursday (Jul 9), down around 7 per cent in the year to date.

As investors sold down to raise liquidity during the Middle East conflict, the price of gold came under pressure, but analysts said demand in Asia has propped up prices.

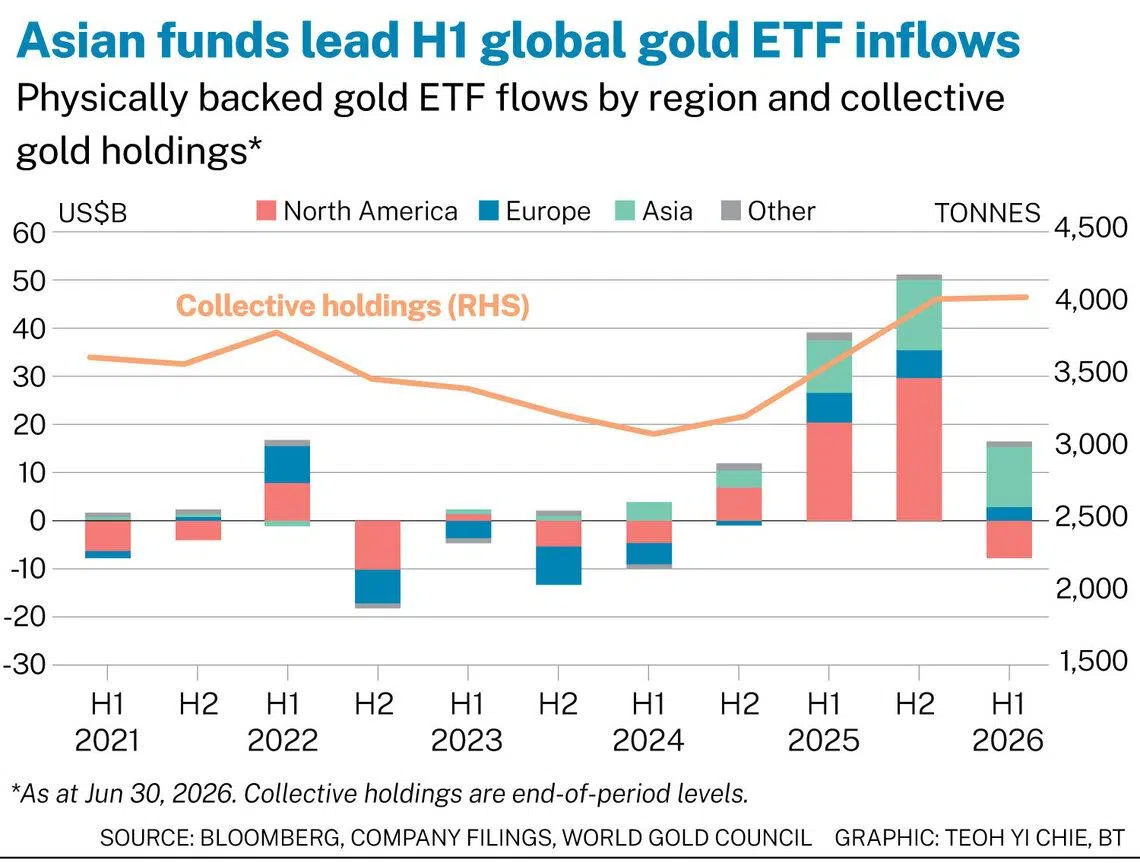

One proxy for this is physically backed gold exchange traded funds (ETFs). Asia led global inflows into gold-backed ETFs for the first half of the year, based on a World Gold Council (WGC) report published on Wednesday.

The region added a record US$12.4 billion over the period, and Europe, US$3.2 billion. North America recorded ETF outflows of US$7.7 billion – its weakest first half since H1 2013.

Growing relevance of Asian markets

In recent months, Singapore and Hong Kong have both unveiled measures to deepen their gold infrastructure in trading, vaulting, clearing and custody.

Industry observers told The Business Times that lower gold prices in the near-term are unlikely to derail those ambitions, given their long-term nature and the region’s resilient bullion demand.

“The regional development initiatives have been driven in part by growing physical demand in Asia and the need for timely price discovery rather than record-high prices,” said Suki Cooper, global head of commodities research at Standard Chartered.

Christopher Wong, precious metals strategist at OCBC, agreed, noting that a lower near-term gold price environment “should not be seen as a setback” for Singapore or Hong Kong’s gold-hub ambitions.

“These initiatives are not being built for one price cycle, but are infrastructure plays built around Asia’s longer-term role in bullion ownership, custody, trading and reserve diversification,” he added.

Marissa Salim, Asia-Pacific senior research lead at WGC, said: “Lower prices would be favourable for building up physical stock in line with vault capacity targets. Official sector vaulting decisions, on the other hand, are rather price agnostic.

“The multi-year infrastructural timelines of both gold hubs is unlikely to be redirected by a pullback, as the commitment to building the gold hubs rests on the structural shift of gold’s epicentre into Asia.”

Robin Tsui, Asia-Pacific gold strategist at State Street Investment Management, said: “Success will depend more on liquidity and market participation than on gold price levels, with the resilient demand for gold in Asia thus far this year continuing to support these initiatives.”

Price discovery in Asia

Based on intraday trading analysis, gold’s price rebounds generally happened during Asian hours, said WGC in its Gold Mid-Year Outlook 2026.

“This further highlights the increasingly relevant role that Asian investors (and consumers) play in price discovery and direction,” it noted.

Salim of WGC said that official-sector purchases and investment-related demand remain key drivers of Asian demand.

She added that the region’s private wealth sector is also a growing contributor.

In a nod to the region’s growing influence, the London Bullion Market Association (LBMA) announced at the Asia-Pacific Precious Metals Conference in June that it would consider shifting its morning auction hours earlier to better align with Asian trading activity.

Where are gold prices headed?

State Street’s Tsui pointed out that Asian retail investors and emerging market central banks “should remain key sources of gold demand”.

“Gold’s resilience above US$4,000 reflects strong Asian buying; any move back towards US$5,000 is likely to be driven by a weaker US dollar, lower real yields and a recovery in Western demand,” said Tsui.

He added that even at higher prices, Asian investors and central banks are expected to remain net buyers, given their long-term strategic allocation to gold, as was the case in the first quarter of 2026.

WGC noted that if current conditions do not materially change, gold may trade within a 5 per cent range of US$4,100 an ounce in the second half of the year.

A “clear catalyst” would be required for the yellow metal to resume its upward trend, said WGC.

Examples of catalysts that would give gold momentum again would be a worsening of economic or geopolitical conditions, a reversal in interest rate expectations and renewed long-term investor participation.

Cooper of Standard Chartered said that tactical headwinds are likely to ease in the coming months, but price levels and volatility are likely to play a greater role in the timing of retail demand recovery. “We continue to expect prices to search for a floor in the near term, but regain momentum before year-end,” she added.

Abhilash Narayan, investment strategist at HSBC Private Bank and Premier Wealth, said the bank remains “tactically overweight” on gold, given its role as a hedge against inflation, elevated geopolitical risks and the potential for renewed US dollar weakness.

“Lower oil prices and less pressure on foreign exchange reserves should bolster emerging market central bank demand for gold in the coming quarters, which, combined with continued retail investor diversification, should support gold prices over the next six to 12 months,” said Narayan.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.