Singapore dollar perpetuals soar amid global hunt for yield

Investors see them as access to credit-worthy names paying pretty high coupons

DeeperDive is a beta AI feature. Refer to full articles for the facts.

Singapore

PRICES of Singdollar (SGD) perpetuals have risen sharply and investors who kept faith earlier, when poor sentiment gripped the bond market as oil and gas issues collapsed, have been amply rewarded.

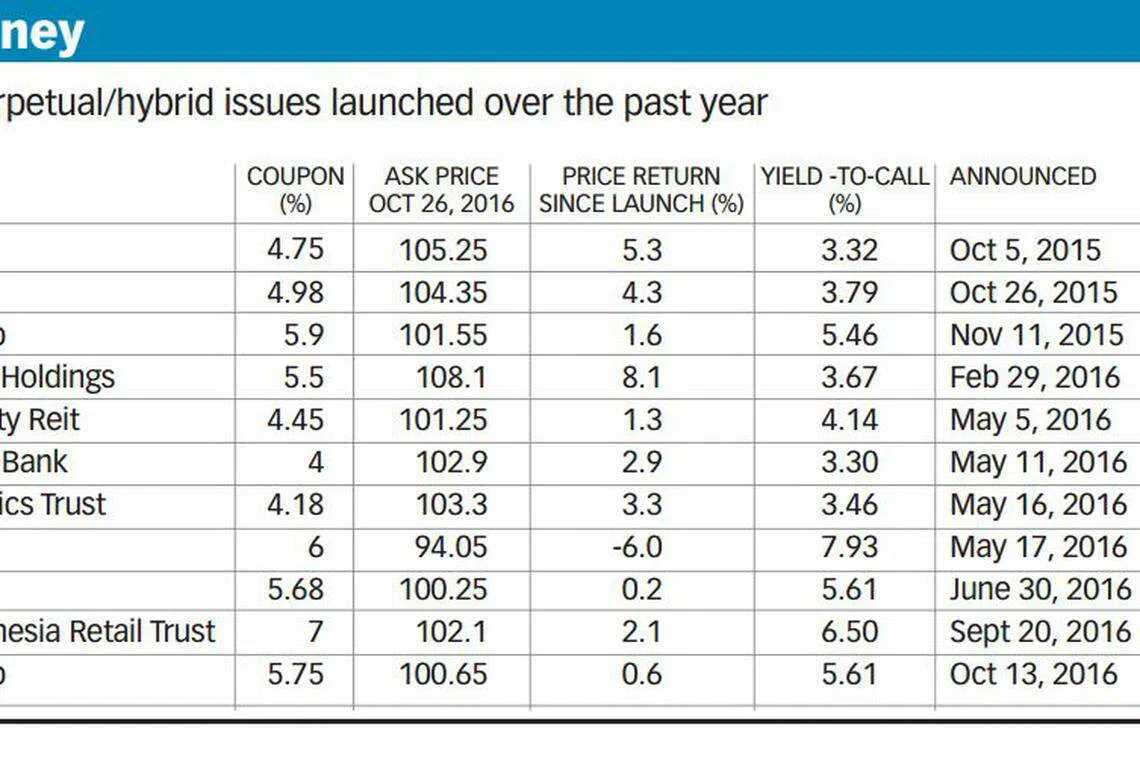

The top performer is AusNet Services 5.5 per cent S$200 million bonds whose price has soared - last week, it hit 108.1, giving a return of 8.1 per cent since its March sale. At current levels, the yield has fallen to 3.7 per cent.

Bonds are sold at 100 par; bond yields fall when prices rise and vice versa. Perpetuals are hybrid bonds with no fixed maturity though they typically have a call date when the issuer has the option to redeem the bond.

Strictly speaking, the AusNet deal is a long-tenure bond of 60.5 years with a call in 5.5 years, giving it perpetual-like features. That means the debt matures in September 2076 but it can also be called or redeemed by the issuer in September 2021.

AusNet Services counts Singapore Power and the State Grid Corp of China as its largest shareholders.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

At the time of its sale in Q1, financial markets were pretty choppy and AusNet's features were also a first time structure for the market, according to Clifford Lee, head of fixed income at DBS Bank. Orders were a modest S$280 million.

"The deal caught favour later," said Mr Lee.

"It's a cheaper way of getting access to high quality perpetuals," said Terence Lin, assistant director of bonds and portfolio management at fund researcher iFast.

Bonds are sold at S$250,000 a pop. By cheaper, Mr Lin was referring to the fact that investors are getting access to a credit-worthy name which pays pretty high coupons.

The overall SGD bond market has done well, in line with the global fixed income market but perpetuals have stood out with their outperformance.

The Markit iBoxx Singapore corporates return index hit a new high of 118.1959 on Oct 26, and is up about 4 per cent year-to-date.

Said Todd Schubert, Bank of Singapore head of fixed income research: "2016 has been one of the best years for bonds in quite some time and fixed income continues to perform well in the global hunt for yield; the Singapore bond market is no exception to this global phenomenon."

Most of the perps sold over the past year are strong credits with high yields, and several are also real estate investment trusts (Reits), which are seen as steady businesses.

SGD perps in particular offer several attributes, said Mr Schubert.

"They tend to offer incremental yield to other shorter maturity bonds and because of their larger denomination they tend to be issued either by systemically important Singapore domiciled companies or well-recognised foreign companies," he said.

Mr Lin said : "Perpetuals are back in favour for investors looking for big companies with steady business and wanting a bit more yield."

Perps sold by Reits which have done well include Ascendas Real Estate Investment Trust's 4.75 per cent and Keppel Reit's 4.98 per cent - both were sold in October last year and have returned about 5.3 per cent and 4.3 per cent over the past 12 months.

Last month, investors brave enough to venture into Lippo Malls Indonesia Retail Trust 7 per cent perps probably feel vindicated as the price rose to a high of 102.1.

The issuer - which owns shopping malls in Indonesia - sold its perps amid the poor sentiment that has continued to paralyse some segments of the bond market since August following the default of Swiber, an offshore and marine services provider.

"When they came out, sentiment was poor, so the price was generous," said Mr Lin.

The 7 per cent coupon for the Indonesian company is the highest paid so far this year for new issues.

One perp which has done badly is Hyflux 6 per cent, which is down some 6 per cent since its May sale.

Mr Lin reckons Hyflux is seen as less strong than the others, and the issuer is also more leveraged.

With the prospect of higher interest rates around the corner, is the bull run over?

Mr Lee said that there is a lot of caution surrounding smaller issuers but he noted the increasing liquidity in the market as redemptions so far this year have reached almost S$18 billion.

There will be more new issues before the end of the year, said Mr Lee.

"Market continues to be liquid and hunting for assets, and higher grade issues are favoured," he said.

Neel Gopalakrishnan, emerging markets bond analyst at Credit Suisse, said that investors should be selective when investing in perpetual bonds as the credit quality of the issuer and the structure of the bond are important considerations.

"As an example, in an environment where interest rates are rising, a perpetual bond with a fixed coupon for life, even if it is from a high quality issuer, could sell off materially if the current coupon rate is low."

READ MORE: After rally, emerging market bonds no longer cheap

Copyright SPH Media. All rights reserved.

TRENDING NOW

Ministry of Home Affairs Permanent Secretary Pang Kin Keong to retire

Shelving S$5 billion office redevelopment plan proved ‘wise’ as geopolitical risks mount: OCBC chairman

Richard Eu on how core values, customers keep Singapore’s TCM chain Eu Yan Sang relevant

China pips the US if Asean is forced to choose, but analysts warn against reading it like a sports result