Issue 58: Incentivising EV adoption; an ESG bond falls out of favour

DeeperDive is a beta AI feature. Refer to full articles for the facts.

In this issue: Improving electric vehicle adoption isn’t just about incentives, but also infrastructure, while the market cools for the once-hot sustainability-linked bonds.

Singapore

Driving adoption of EVs

Two incentive schemes for electric vehicles will expire at the end of this year, and the question is whether those incentives should be continued.

The first scheme is the Enhanced Vehicular Emissions Scheme, which assigns rebates or penalties to vehicles depending on their tailpipe emissions. Only electric vehicles can receive the maximum rebate of S$25,000.

The second scheme is the Early Adoption Incentive, which discounts electric vehicles’ Additional Registration Fee by 45 per cent, capped at S$20,000.

The Singapore Ministry of Transport has yet to reveal its plans for these incentives.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

Incentives are distortionary and can have unintended consequences, which is why there’s a natural policy reluctance to keep incentive schemes around for too long.

For example, providing rebates and discounts to buyers of electric vehicles could lead dealerships to increase the prices of electric vehicles, which would allow dealerships to keep the benefits of the incentives instead of passing them down to buyers.

There is also a natural incentive to buy lower emissions vehicles, which is that the cost of fuel is lower. Vehicle buyers are, therefore, even without additional incentives, already better off buying an electric vehicle even if it costs slightly more than an internal combustion engine vehicle.

SEE ALSO

But with electric vehicles still making up only 14 per cent of new car registrations, Singapore is still far from its goal of having an entirely clean vehicle fleet by 2040. Removing incentives now might make it even harder to reach that target.

Perhaps a larger factor in hindering the rate of adoption of electric vehicles is charging infrastructure. Most people in Singapore live and work in high-rises, and their cars are therefore parked in shared spaces. Until there is greater availability of charging stations, vehicle buyers might not be so keen to switch to electric vehicles.

The Land Transport Authority is aiming to make every HDB township “EV-ready” by 2025, with charging points in almost 2,000 housing board car parks. How well that plan is carried out will be a key factor in the greening of the country’s vehicle fleet.

Other Singapore reads

- Keppel and consortium break ground for Singapore’s first hydrogen-ready co-generation plant

- Chinese EV giant BYD to assemble Singapore electric scooter

South-east Asia

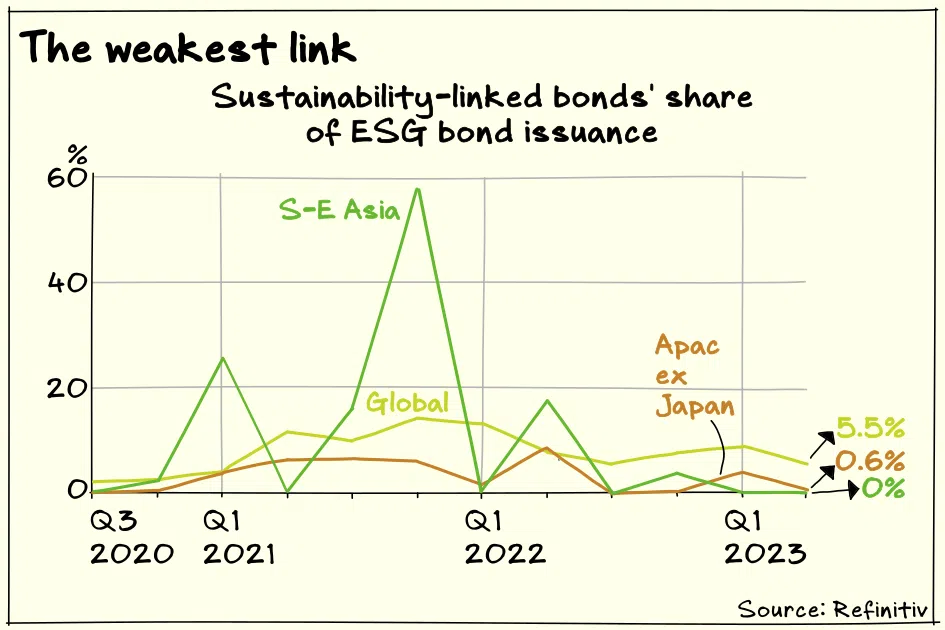

Sustainability-linked bonds lose their shine

From the end of 2020, through all of 2021 and then the first half of 2022, sustainability-linked bonds (SLBs) were all the rage. In the fourth quarter of 2021, SLBs made up more than half of new ESG bond issuance in South-east Asia, according to Refinitiv data.

But just like that, SLB volumes have dried up. There were no new SLBs issued in South-east Asia in the first half of 2023. Their share of the ESG bond market in the rest of the world has also declined.

It’s what happens when enough people have played with the shiny new toy and realised that it’s not as awesome as it looked in the commercials and in the hands of that kid on the bus. SLBs have become the fidget spinners of ESG bonds.

There are generally two classes of ESG bonds. The first are use-of-proceeds bonds, which get the “green”, “social” or “sustainability” bond labels only if the proceeds will be applied to activities that meet “green”, “social” or “sustainability” standards.

SLBs form the second class. The proceeds of SLBs can be used for pretty much anything. However, the borrower is subject to sustainability-related targets that affect the interest that the borrower has to pay on the bond. As an example, Singtel subsidiary Optus has a 4.577 per cent SLB due 2028. If Optus fails to meet an emissions target by 2025, the coupon on the SLB will step up by 25 basis points.

The first SLB was launched in 2019 by energy group Enel. It was only around the end of 2020 that it really started to take off in South-east Asia.

Folks were excited about SLBs because they seemed to have the potential to induce decarbonisation at an entity level. A green bond might help a coal power company to build a solar farm, but the company could still continue to run its coal plants. With an SLB, however, the same company would need to lower its overall emissions to benefit from the structure.

In South-east Asia, in particular, that was an enticing prospect, because of the need to decarbonise vast swathes of the economy. Not every business in Indonesia is going to build a solar plant, but many of them could decarbonise by switching to renewable energy, reducing waste and consumption and various other measures.

The market has become more cautious with regards to SLBs. One major criticism has been with the KPIs, many of which in the early days had questionable levels of ambition. The industry has been trying to move towards science-based targets, but adoption has been slow.

A recent study by BloombergNEF also found that a quarter of SLBs allow borrowers to redeem the bonds before penalties are triggered. This would mean that borrowers who are about to miss their targets have an escape route.

It’s not surprising that a relatively new structure like the SLB will have some growing pains. Unlike fidget spinners, however, SLBs are still valuable because of their ability to generate entity-level impact. One indicator of this is that sustainability-linked loans, which also apply target-linked margin adjustment mechanisms, are still getting done despite somewhat similar concerns about targets. SLBs could yet stage a comeback if the industry can address the early criticisms.

Other South-east Asia reads

- Vietnam approves 750 trillion dong plan to expand fuel storage capacity by 2030

- Vietnam EV maker VinFast to start construction of US factory next week

Other good reads

- Singapore needs both quality and quantity to win the carbon-trading race

- Is the EU’s green edge under threat?

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

Air India asks Tata, Singapore Airlines for funds after US$2.4 billion loss

‘Boring’ is the new black: The stars are aligning for a Singapore stock market revival

From 1MDB to ‘corporate mafia’: Is Malaysia facing a new governance test?

South-east Asian markets account for 8.8% of global capital inflows from 2021 to 2024: report