|

|

|

|

|

|

| FRI, MAR 6, 2026 | |

Kenneth Lim

Columnist

|

|

This week in ESG |

|

Sustainable investing |

Renewables and oil prices: It’s complicated |

|

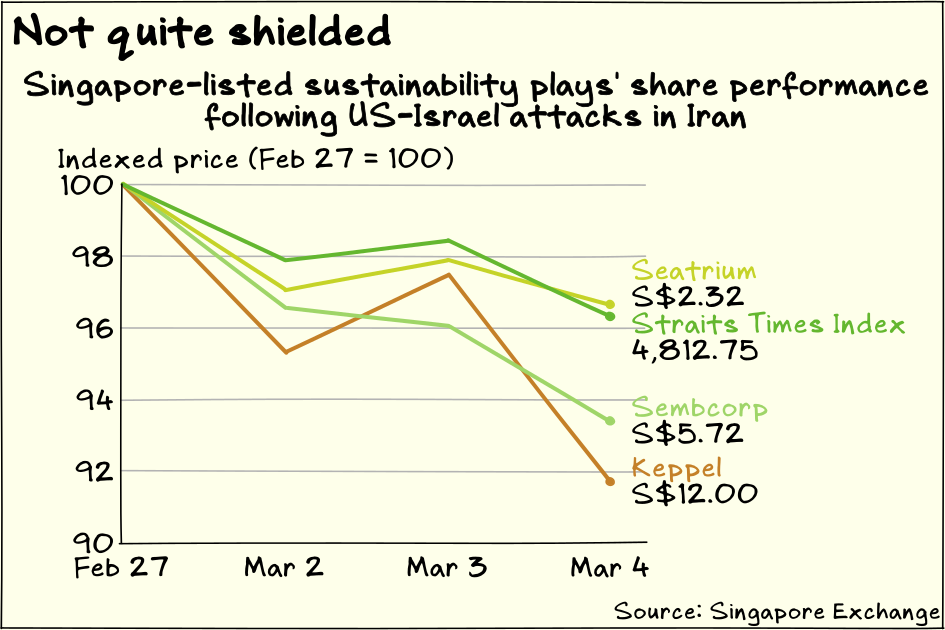

Investors looking to sustainability plays for immediate shelter from the oil price hikes of the US-Israeli war in Iran may want to tread with caution. Shares of the purest renewable energy plays on the Singapore Exchange have not fared well in the first few days of trading after the US and Israel launched their attacks on Feb 28. Sembcorp Industries, a renewable energy developer, closed at S$5.72 on Wednesday, down 6.5 per cent from before the weekend. The Straits Times Index, the Singapore market benchmark, declined by a more modest 3.7 per cent over the same period. Keppel Corp, an asset manager with significant sustainability-related investments, also underperformed the market with an 8.3 per cent retreat since the attacks to end at S$12 on Wednesday. Shares of Seatrium, a shipbuilder for both the oil and gas and offshore wind sectors, decreased 3.3 per cent to head out at S$2.32 on Wednesday. Why doesn’t a surge in oil prices and the prospect of those prices staying elevated for a prolonged period translate into higher optimism for renewable energy players? Shouldn’t the burden of higher oil prices shift demand towards renewable energy alternatives? A possible answer is that consumption demand and investment interest in renewable energy are driven by more than just oil prices, and it’s the multivariate complexity that makes it challenging to draw a clear relationship between oil prices and renewables. For example, a 2024 working paper by researchers at the International Monetary Fund finds insufficient evidence to show that renewable adoption reduces the impact of fossil fuel price changes on energy inflation rates. The inconclusive relationship could be a result of difficulties in controlling for national energy policies, threshold effects or trade linkage spillovers, the researchers explain. Whatever the reasons, the uncertainty reduces the confidence in renewable energy as a shield against oil price spikes. Markets are also highly idiosyncratic, which means that tendencies in one geography can be irrelevant in others. A 2025 paper by Chinese and Spanish researchers finds mixed impact of energy-related uncertainty on US renewable energy demand. On one hand, energy-related uncertainty spurs efforts to seek sustainable alternatives and accelerate renewable deployment, while greater renewable usage tends to reduce energy-related uncertainty. On the other hand, higher uncertainty about energy prices inhibits investment in renewables. But this study focuses on US data, and the findings may not apply to other markets. Another study by South Korean researchers suggests that renewable energy consumption can mitigate the risk of oil prices, while higher oil prices can raise concerns about external risks and drive greater investments in renewable energy. But the research focuses only on oil-importing countries. Those studies illustrate how challenging it can be to model with confidence how the current situation in the Middle East will affect sustainability players. For a country like Singapore, which imports all of its fuel and relies heavily on natural gas for electricity, higher oil and gas prices could provide greater impetus to diversify the fuel and energy mix. But for a country like Indonesia, which has domestic supplies of oil and gas and coal, higher fossil fuel prices could drive greater investments into domestic extraction and energy activities. Adjacent to the energy sector, in the transportation arena higher fossil fuel prices might not necessarily drive up demand for electric vehicles. In markets where electricity is primarily produced by fossil fuels, higher oil and gas prices could also raise electricity prices. Furthermore, immediate demand for electric vehicles is highly dependent on the level of access to charging infrastructure. Probably the most significant impact from attacks in Iran is that it becomes more difficult to predict the future prospects for renewable players, which can chill investment interest. Without a good idea of how long the war might last, much less the objectives of the campaign, it’s difficult to use that as a decision input for assessing renewable investments, some of which can be long-term infrastructure projects. What are sustainable investors to do in these times? Heightened short-term uncertainties could be a time to stick with higher-confidence long-term structural trends. For instance, a rather popular thesis – often used in scenario analyses as a potential future – is that the inevitable physical impact of climate change and slow-to-act policymakers will drive increased disorderly transition risks. That scenario may not change much even if there is a war in the Middle East. In fact, some of the potential beneficiaries of this long-term trend – renewable energy players, infrastructure developers and green real estate players, for example – could be bargain pick-ups in the current market turmoil. |

Climate policy |

Singapore to craft national adaptation strategy |

|

The immense scale and potential severity of global warming mean that a national climate adaptation plan could become one of Singapore’s most critical long-term policies. Sustainability and Environment Minister Grace Fu told Parliament that Singapore will make climate adaptation planning a priority in 2026, with the aim of producing a national adaptation plan by 2027. The plan will address resilience in key areas such as heat, coastal and flood impact, and water and food, Fu said in her ministry’s Committee of Supply debate. The national adaptation plan will complement Singapore’s climate mitigation strategy, which is mainly aimed at cutting Singapore’s greenhouse gas emissions. The world is now widely expected to miss the Paris Agreement goal of limiting global warming to 1.5 deg C above pre-industrial levels by 2100. Climate Action Tracker estimated in November that the best case scenario – which assumes that all national targets, commitments and pledges are met – would lead to warming of 2.2 deg C by the end of the century. Actual policies currently will lead to 2.6 deg C of warming. Fu told Parliament that Singapore must prepare for a “climate-impaired future”. Public policy must take the lead in building resilience to that sort of future because of the scale and longevity of the problems. The entire island is affected when sea levels rise, temperatures climb, and food and water become scarcer. In many cases, the optimal solutions require solutions at similar scales. Creating barrier islands like the planned Long Island project off the eastern coastline cannot be achieved without public-sector commitments and funding. District cooling infrastructure and building standards to mandate cooler designs must be incorporated into city planning. Food and water supply chain strategies need national coordination. Many of these are long-term solutions, where the private sector can sometimes be structurally ill-suited to tackle. It is encouraging that the government is planning a series of engagements to inform the drafting of the plan. It is imperative that the adaptation plan has a strong scientific basis, and that it considers the needs and realities of all segments of society. The national adaptation plan will have wide-reaching consequences for the way that the city develops and builds itself in the coming years. Businesses and investors should take heed. |

|

Did you receive this newsletter from someone? Sign up here to get the latest updates sent right to your inbox. |

|

|

|||||||||||||||||

|

|

|||||

|

|||||

|