Singapore households’ net wealth up, but also taking on more debt such as home loans

This marks the 10th straight quarter in which household borrowing has picked up pace

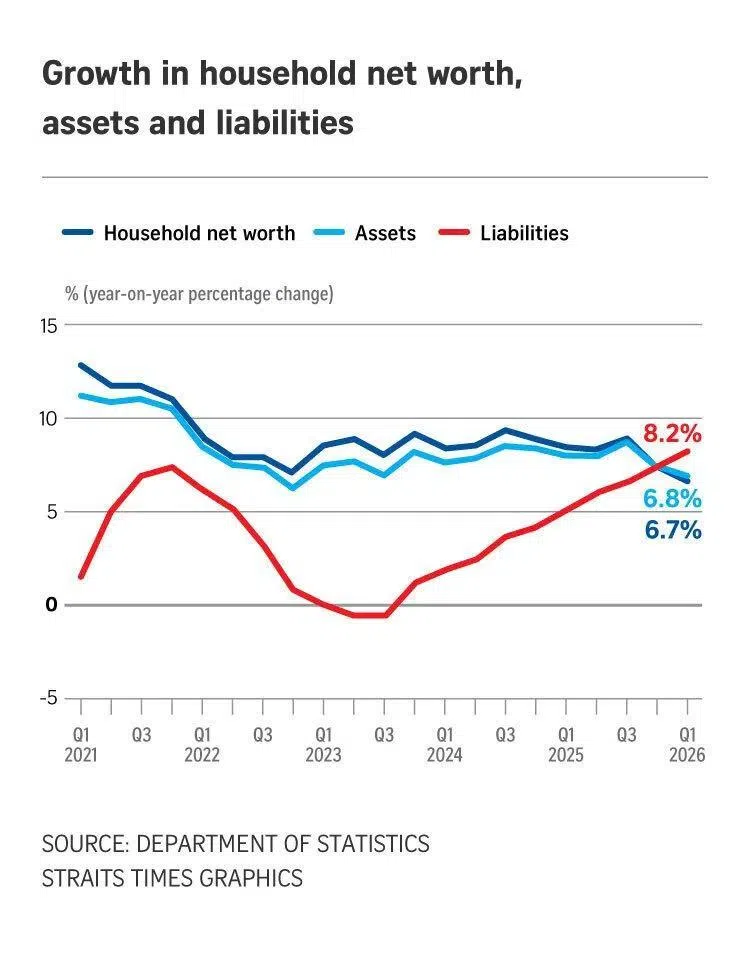

[SINGAPORE] Households here are better off than a year ago, with net worth rising 6.7 per cent, but are also taking on debt at a faster pace.

Household liabilities grew by 8.2 per cent year on year in the first quarter of 2026, according to the latest household balance sheet released by the Department of Statistics (SingStat).

This marked the 10th straight quarter in which household borrowing has picked up pace.

Meanwhile, the financial and residential property assets held by households increased year on year by 6.8 per cent in the first quarter of 2026, although at a slower pace than the 7.3 per cent growth in the fourth quarter of 2025.

Notably, households are accumulating debt at a faster clip than they are building wealth – a shift that emerged in the fourth quarter of 2025 and continued through the next quarter.

Lee Yen Nee, senior country risk analyst for the Asia-Pacific region at BMI, a unit of Fitch Solutions, told The Straits Times: “While household liabilities have grown faster than assets, the sheer scale of household wealth means systemic risks remain very low.”

Household net wealth continued to expand in the first quarter to S$3.3 trillion, while total liabilities rose to S$415 billion.

SingStat’s report released on May 26 also showed that household net wealth as a percentage of personal disposable income held steady at 868.3 per cent in the first quarter. This means the net worth of all households – assets net of liabilities – is about 8.7 times their annual aggregate take-home pay.

Excluding illiquid property assets, financial assets as a percentage of personal disposable income fell 0.5 percentage point to 557.3 per cent.

SEE ALSO

Financial assets include readily available bank deposits and other less liquid assets, such as insurance and listed securities. While not completely representative, this figure gives a rough idea of a country’s financial cushion.

At 5.6 times take-home pay, it means that households collectively have a reserve that can sustain them for around five to six years if they lose their jobs.

Mortgage and car loans

The pick-up in household liabilities in the first quarter of 2026 was due to faster growth in mortgage and personal loans, noted SingStat.

Mortgage loans grew 5.8 per cent year on year, following 5.4 per cent growth in the fourth quarter of 2025.

A home loan is typically the biggest debt for a Singapore family, making up at least 70 per cent of total liabilities.

Personal loans, which make up the remaining 30 per cent of total liabilities, grew for nine straight quarters – since the first quarter of 2024 – to S$118.6 billion.

Such loans include secured car loans, outstanding balances on credit and charge cards, and other unsecured loans like education loans, overdrafts and renovation loans.

Car loans and other unsecured loans drove the increase in personal loans in the first quarter.

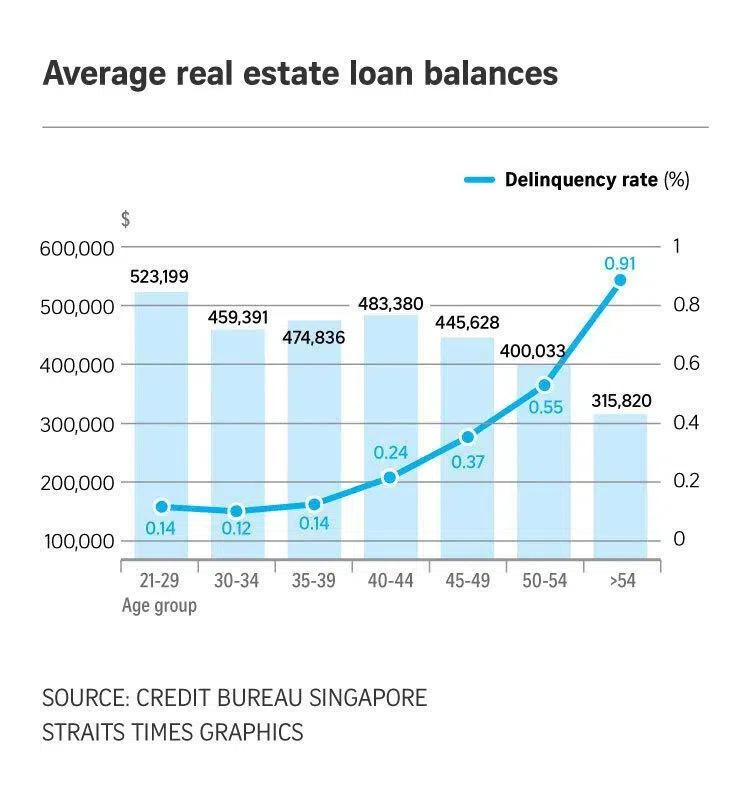

A separate quarterly report from Credit Bureau Singapore showed that home owners in the 21 to 29 age group had the highest average home loan balances of S$523,199 in the first quarter of 2026, but one of the lowest delinquency rates of 0.14 per cent.

A delinquency rate of 0.14 means 14 out of every 10,000 households are delinquent or late in their payments by more than 30 days.

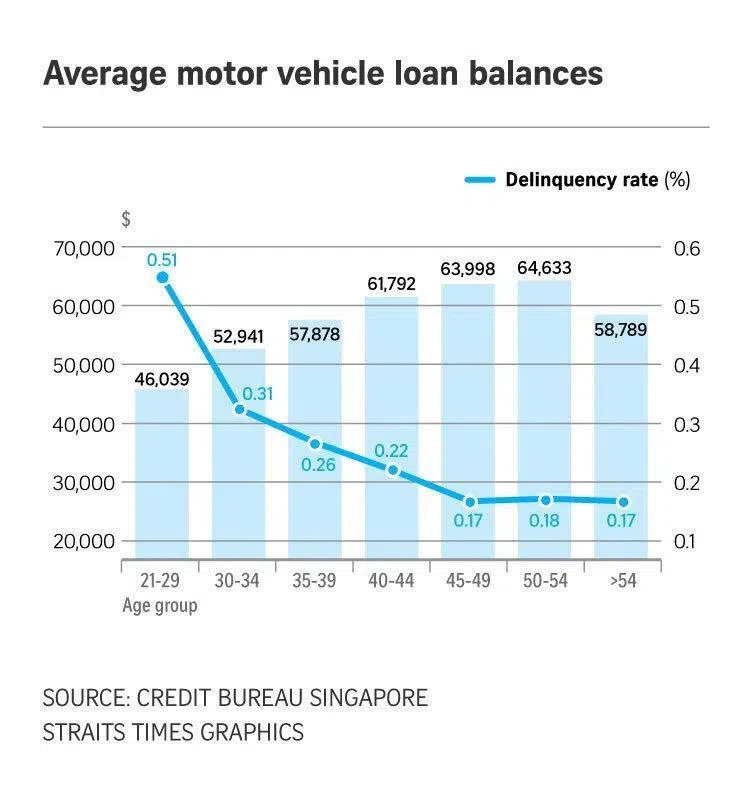

The report also showed that borrowers in the 50 to 54 age group had the highest car loan balances of S$64,633, but their delinquency rate of 0.18 per cent was among the lowest across age cohorts.

Meanwhile, those aged between 21 and 29 have the highest delinquency rate of 0.51 per cent despite having the lowest average balances of S$46,039.

Unsecured personal loans and credit card debt

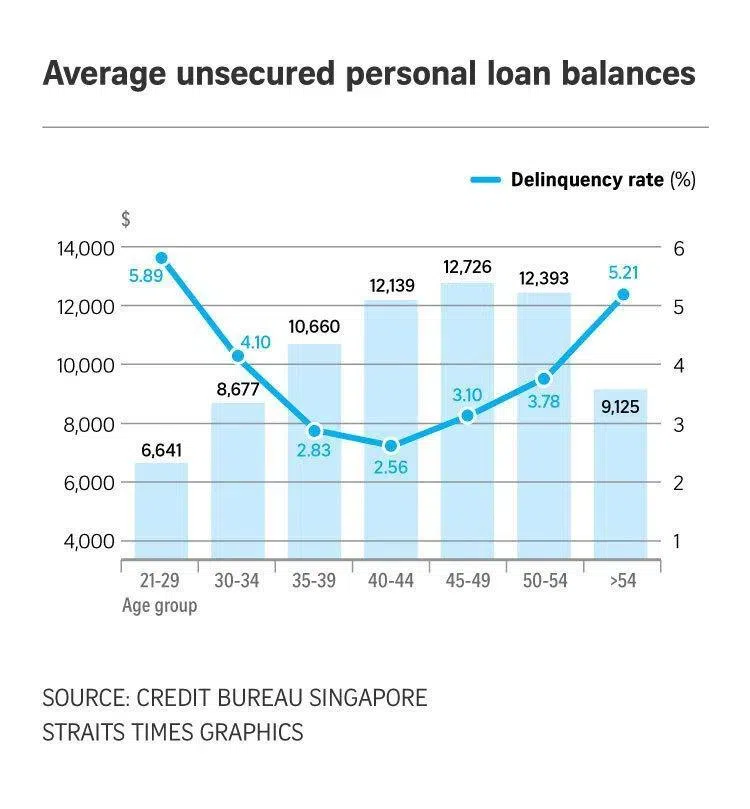

The situation for unsecured personal loans was more of a concern, with delinquency rates above 1 per cent.

Borrowers aged 21 to 29 and those over 54 were the most likely to fall behind in their payments, despite having some of the lowest average unsecured personal loan balances.

Meanwhile, unpaid credit and charge card bills grew at a slower pace of 6.8 per cent in the first quarter, from 6.9 per cent growth in the fourth quarter.

The SingStat household balance sheet data tracks the total outstanding balances of credit cards issued by commercial banks to Singapore residents, inclusive of both current and overdue accounts.

Separately, a report by the Monetary Authority of Singapore (MAS) on May 29 monitors credit card rollover balances. Such amounts not paid by the due date continued to grow in the first quarter of 2026, but at a slower pace of 12.7 per cent year on year to S$9.4 billion.

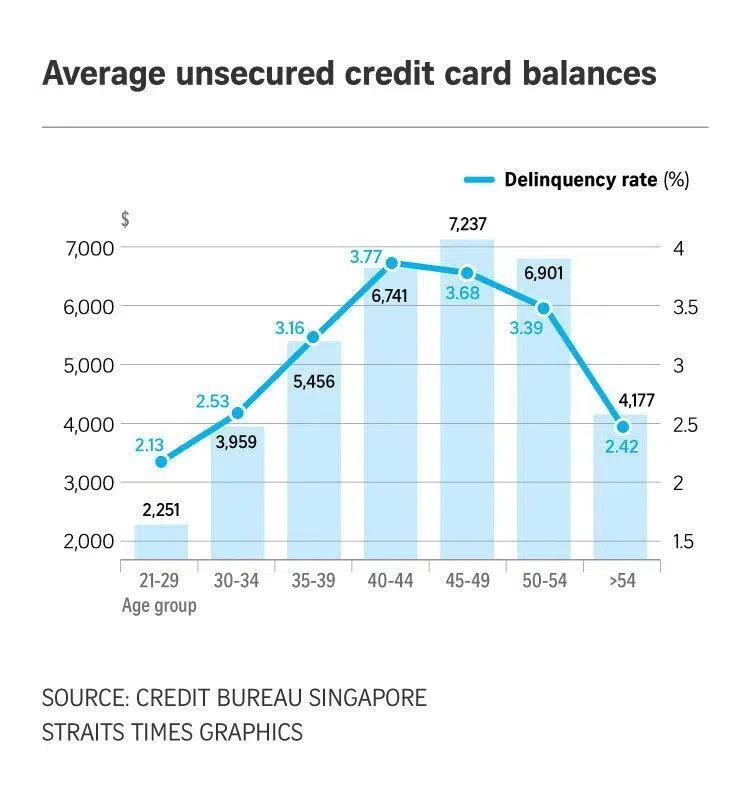

Borrowers in the 40 to 54 age bracket had some of the highest average balances of S$6,741 to S$7,237, and their delinquency rates of 3.39 to 3.77 per cent were among the highest.

Debt growth contained

Still, SingStat figures indicate that the debt situation remains broadly stable for now.

Despite household liabilities as a percentage of personal disposable income rising 0.5 percentage point to 107.9 per cent in the first quarter of 2026, this remains below the 10-year historical average of 132 per cent.

Household liabilities as a percentage of personal disposable income measures how much debt a typical family owes relative to what it earns after taxes. A higher ratio indicates potentially greater financial strain, as more take-home pay is diverted to service debt.

BMI’s Lee noted that despite the rise in borrowing, “liabilities accounted for just 11 per cent of household assets in the first quarter of 2026, broadly in line with around 10.9 per cent throughout 2025”.

Lee added that Singapore’s rules on borrowing and loans provide a strong safeguard against over-leveraging by households.

She said measures such as the total debt servicing ratio (TDSR) and loan-to-value (LTV) limits ensure that additional borrowing remains prudent and sustainable.

TDSR caps a borrower’s total monthly debt obligations to no more than 55 per cent of their gross monthly income, while LTV limits cap the maximum amount a borrower can take for secured loans, typically at a percentage of the asset’s value.

Unsecured loans, like credit card debt and personal loans, do not use LTV because there is no underlying asset to value. Instead, MAS caps a borrower’s total unsecured credit at 12 times their monthly income.

If a borrower exceeds this limit for three consecutive months, he will not be able to obtain new credit facilities. His existing credit lines will also be suspended.

Given the safeguards in place, Lee surmised that the recent pick-up in liabilities growth is more likely to be driven by the wealthier households who have strong cash reserves.

The debt build-up does not reflect a rise in financial vulnerability across the population, she added. THE STRAITS TIMES

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services