US dollar set to be stronger for longer

The initial risk aversion that pushed US bond yields and the US dollar higher should dissipate in the days and weeks ahead. But a full reversal of dollar strength appears unlikely

THE hawkish shift in expectations for US monetary policy into the second half of 2023 – alongside a spike in market jitters over the debt ceiling impasse – has seen the US dollar appreciate meaningfully across the board, including against Asian currencies in general and the Chinese yuan in particular.

Between Apr 13 and May 24, the US dollar index (DXY) has risen 2.5 per cent and Asian currencies have fallen 1.8 per cent. The yuan has underperformed and depreciated by 2.5 per cent. The prospects for most Asian currencies hinge quite heavily on where the US dollar goes and how much tighter global liquidity gets, both as a result of the dollar strength and the US Federal Reserve’s policy rate trajectory.

China’s yuan, though, is probably going to be significantly more dependent on the country’s growth and balance of payments (BOP) fundamentals.

Nothing and something

Let us first address the elephant in the room: the US debt ceiling impasse. Although the ramifications of the US Treasury defaulting on its debt obligation would have been catastrophic, it was always unlikely for that very reason, in our view. In the last few days, it seems a last-minute deal between the Democrats and Republicans has been agreed upon in principle, although it still needs to be voted upon before being fully approved.

Thus, the initial risk aversion that pushed US bond yields and the US dollar higher should subsequently dissipate in the days and weeks ahead, although a full reversal in US dollar strength appears unlikely.

The shift higher in interest rate expectations might prove more enduring, however. While we have consistently expected that the Fed would keep interest rates at the current terminal level of 5 per cent to 5.25 per cent, the market seems to only now be coming round from its originally more dovish starting position.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

Back in April, the market assigned a 93 per cent probability of the Fed cutting policy rates by at least 50 basis points (bps) by the end of the year. This probability has now fallen to 47 per cent. The decline in the probability of over 75 bps of cuts has been even sharper – from 68 per cent to under 12 per cent.

The shift in expectations has been prompted by a trifecta of risks, including the still-tight US labour market, a growing view that long-term inflation expectations may actually be rising, and importantly, that Fed officials appear to have noticed and have become concerned.

Although some Fed officials have hinted at additional rate hikes, we continue to expect that they are “done”. The pricing out of rate hikes, however, still has some way to go, and therein lies some possible near-term US dollar support.

US dollar strength

There exists a close, enduring and inverted relationship between US interest rates, the US dollar and Asia’s risk assets. Higher US interest rates and dollar strength suck both opportunity and liquidity from non-US dollar markets, meaning they tend to herald periods of (pronounced) local equity underperformance.

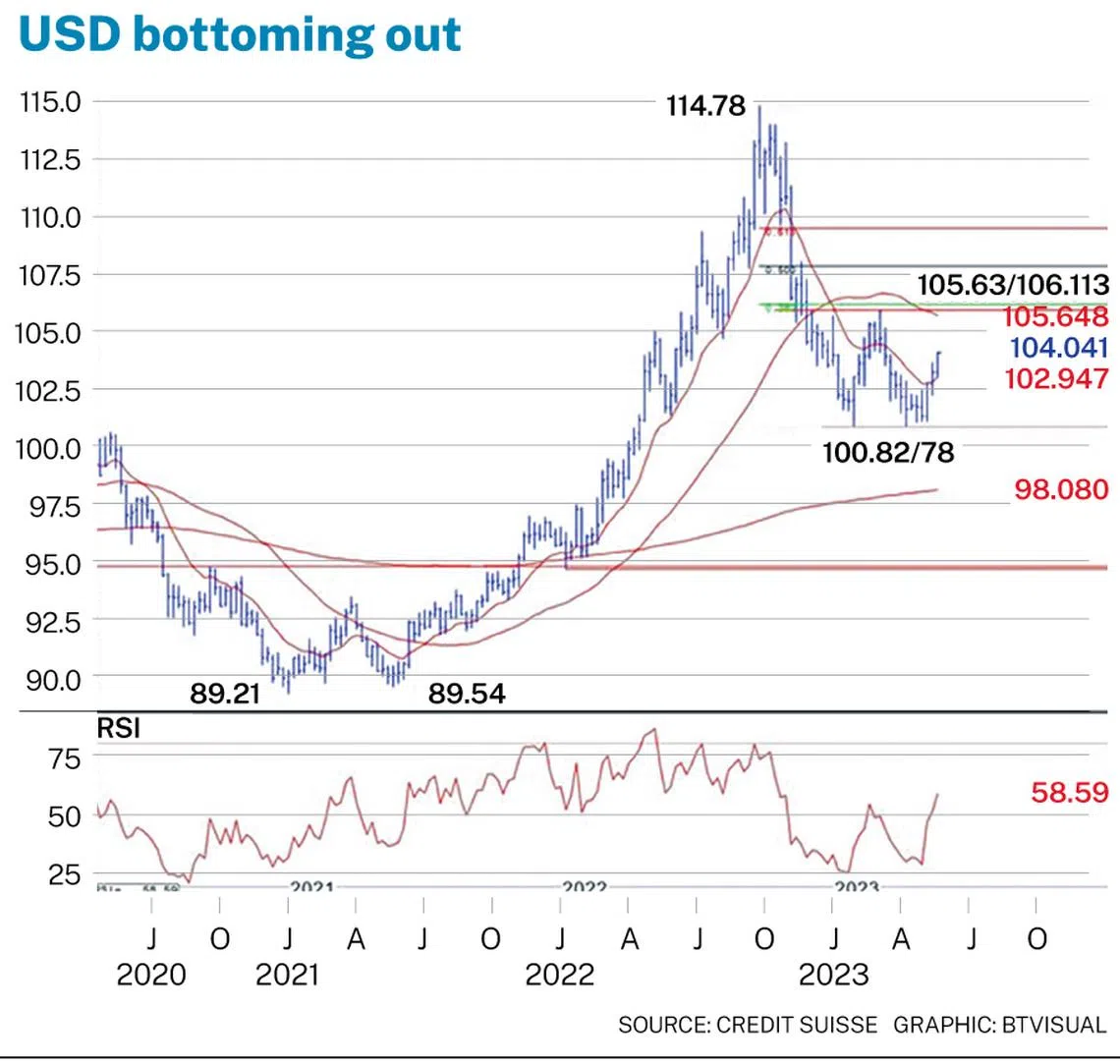

While we remain neutral on the US dollar, the technical picture appears to have turned more supportive. The failure of the DXY to break the key support just below 101 – along with the shift in economic fundamentals – potentially opens the way for a retracement higher to key levels around 106, and then 108.

Yuan dynamics

The historical record suggests that the broad rise in the US dollar will almost certainly be accompanied by a decline in Asian currencies. The most consequential and most watched currency among these is the yuan. Within the space of the last month (since Apr 24), the US dollar/yuan rose 2.4 per cent from below 6.90 yuan (S$1.32) to 7.07 yuan. This has been broadly in line with the DXY’s rise, but has exceeded the decline in almost all other Asian currencies.

This begs the obvious question: Is the yuan underperformance likely to continue? We had previously expected the post-Covid reopening to have negatively impacted China’s current account balance. This now appears somewhat unfounded, at least in the level of severity.

Thus it appears likely that the yuan may well avoid sustained underperformance versus its emerging market counterparts. Earlier this month, we turned from positive to neutral on the US dollar/yuan, with three-month and 12-month targets at 7 yuan.

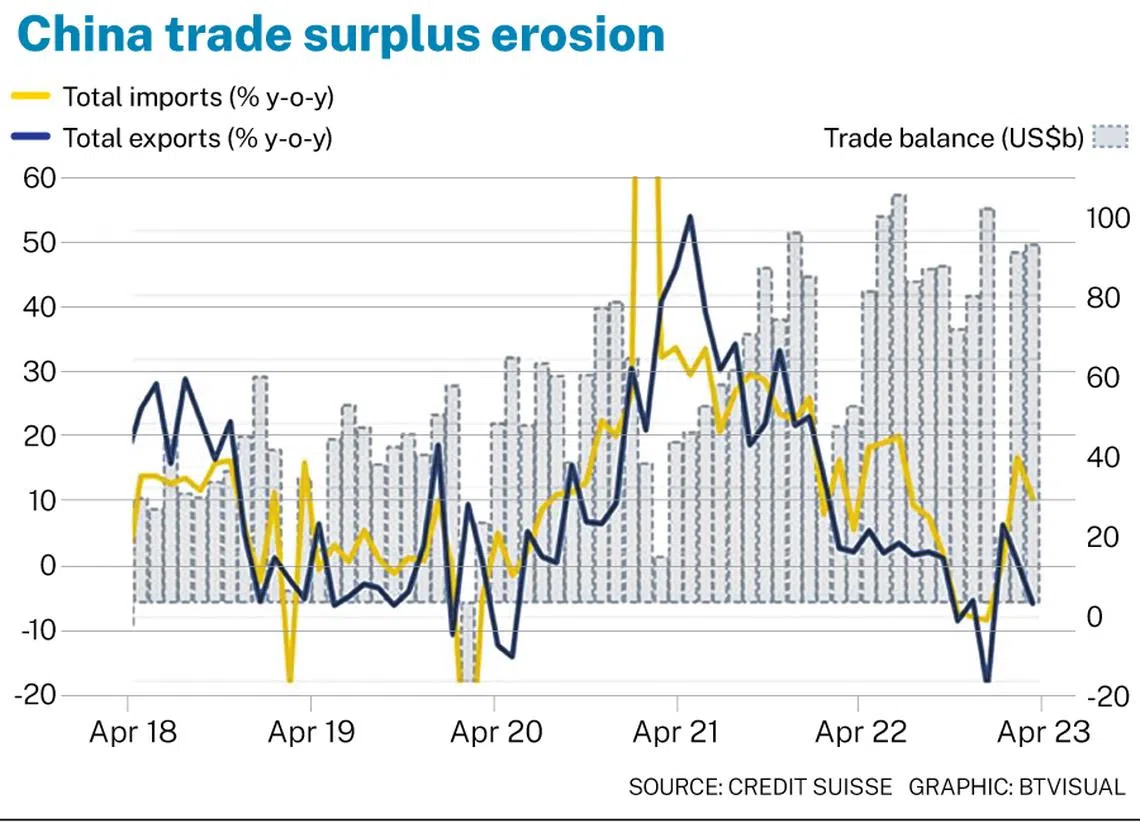

The main reason for the improved yuan outlook is that the recovery in domestic investment activity, along with the recovery of related import demand, has been lacklustre. This has seen the trade surplus rebound to a monthly average of almost US$90 billion (for March and April) – close to a record high.

We expect that import demand will eventually start to gather strength when investment demand picks up, and the trade surplus will narrow as a result. But this is likely to be a more gradual process and thus unlikely to compound the ongoing US dollar strength. For the time being, the economic recovery is largely being driven by consumption, which tends to be less import-intensive.

The consumption-led recovery is nonetheless likely to translate into fairly robust corporate earnings growth. Despite the underperformance of the MSCI China (versus the S&P 500), Stock Connect flows have remained net inward.

Over April through to May 24, as China’s economic momentum disappointed and geopolitical tensions remained elevated, there were still net inflows of some 3.8 billion yuan. Although this was far below the first quarter’s total net inflows of 186 billion yuan, it nonetheless attests to the resilience of investor demand for Chinese onshore equities. This, in turn, suggests portfolio outflows are unlikely to be the cause of near-term yuan weakness.

In fact, the portfolio account might even turn into a source of support for the yuan if the recent signs of a thaw in US-China tensions continue to develop. This month, there has been a flurry of diplomatic activity.

An affirmative response to recent calls from South Korea and a US semiconductor association to slightly ease restrictions on equipment exports to Chinese chip producers could indicate that tensions might be coming off the boil. This, in turn, would be positive for foreign investor sentiment on China equities, in our view.

The yuan’s fundamentals therefore look a lot healthier than they did prior to May. The yuan’s Bank of International Settlements real effective exchange rate has also fallen to one standard deviation below the 10-year average, which could help support China’s exports and slow imports growth. We thus reiterate our neutral view on the US dollar/yuan, while keeping a close eye out for further improvements in the underlying BOP conditions.

The writer is chief investment officer, Asia-Pacific, Credit Suisse.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.