Singapore equities can weather the LNG storm

Global uncertainty is also driving capital reallocation, and the city-state stands to benefit

THE Middle East conflict has escalated into a direct supply shock.

Qatar’s Ras Laffan Industrial City, which accounts for around 20 per cent of global liquefied natural gas (LNG) supply, sustained significant damage, prompting QatarEnergy to declare force majeure.

The Strait of Hormuz, through which roughly 25 per cent of seaborne oil and 19 per cent of global LNG transit, has effectively closed.

Singapore sits directly in the transmission path. The country relies on imported gas for about 95 per cent of its electricity generation, and Qatar accounted for an estimated 47 per cent of its seaborne LNG intake under a long-term contract signed in 2023.

The disruption is therefore immediate and material.

System resilience: four buffers

Singapore’s energy system has materially strengthened its defences since the 2021-22 crisis. Four structural buffers are now active, and reduce the probability of a physical supply shortfall.

Pipeline gas from Malaysia and Indonesia, representing 43 per cent of total supply, continues to flow without interruption.

Strategic LNG and diesel reserves remain fully intact. Singapore GasCo, the centralised state gas buyer that became operational in January 2026, provides a single coordinated procurement function that did not exist during the previous crisis. Dual-fuel power-generation infrastructure, subject to regular readiness testing mandated by the Energy Market Authority (EMA), ensures that each generation unit can transition between gas and diesel as required.

Regulatory and fiscal measures reinforce these physical buffers.

The EMA’s 80 per cent hedging requirement for electricity retailers, introduced in August 2023, slows the pass-through of wholesale price volatility to retail tariffs.

Budget 2026 provides up to S$570 in U-Save rebates for eligible HDB households to help with their utility bills.

This is about 1.5 times the standard annual allocation. Prime Minister Lawrence Wong confirmed on Mar 18 that additional fiscal capacity remains available.

Singapore entered 2026 with a Budget surplus of about S$10.6 billion, equivalent to 1.3 per cent of gross domestic product. This provides substantive room for further policy deployment if conditions deteriorate.

Why LNG price spikes do not drive STI weakness

The April 2026 electricity tariff revision reflects the prevailing pressure.

Before goods and services tax, overall tariffs rose by an average of 2 per cent quarter on quarter. For context, tariffs reached levels of about 40 per cent above pre-crisis levels during the 2022 episode.

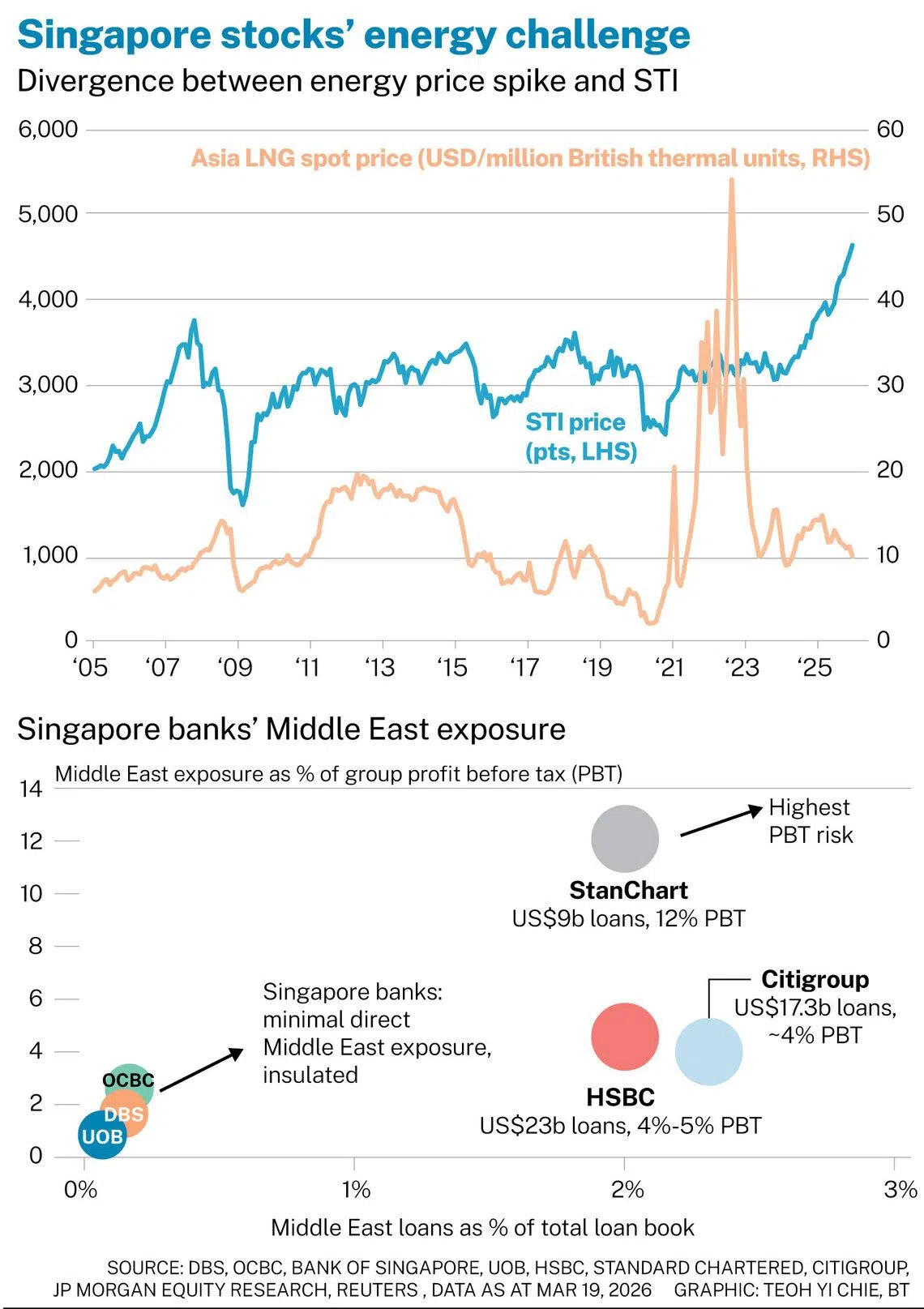

Yet, historical precedent does not support the view that LNG price surges translate into sustained Straits Times Index (STI) underperformance.

Asian LNG import prices and Singapore’s wholesale electricity price have tracked one another closely through every major global disruption over the past two decades. Singapore equities, however, have not followed the same path.

The STI held up through the 2021-22 LNG price surge and continued trending higher thereafter. The key distinction is that energy cost shocks transmit into household tariffs, not into equity market earnings trajectories in a sustained way. The decoupling between energy volatility and equity returns is well-established in Singapore’s market history.

Singapore as safe haven

The same shock that pressures energy costs is simultaneously redirecting capital towards the city-state.

The Singapore dollar appreciated against major currencies amid the global trade volatility in 2025, reflecting its recognised role as a regional safe-haven currency.

The Monetary Authority of Singapore’s exchange rate-based monetary policy framework provides an additional moderating effect on imported energy costs, as a stronger Singdollar reduces the local-currency cost of each US dollar-denominated LNG cargo.

Importantly, the Republic’s banks have limited direct exposure to the Middle East.

Unlike global peers such as HSBC and Standard Chartered, which maintain meaningful lending presence in key Gulf hubs, DBS, OCBC, and UOB have not disclosed any material Gulf Cooperation Council loan books. Direct downside risks from the region therefore remain contained.

At the same time, the indirect impact is more constructive. Global uncertainty is driving capital reallocation, and Singapore continues to stand out as a key beneficiary.

The city-state’s strong rule of law, currency stability, and pro-business regulatory framework underpin its position as a global wealth hub.

Historically, periods of geopolitical stress, including US-China tensions, have supported strong inflows into Singapore, benefiting banks through rising wealth balances and client activity.

Recent developments suggest that this pattern is repeating. Investors are increasingly allocating to Singapore assets amid rising geopolitical risks. Anecdotally, wealth managers are reporting growing relocation inquiries and expect incremental inflows from Gulf-based clients if Middle East tensions persist.

For the three local banks, these inflows translate into a direct earnings tailwind – and through the wealth management segment that is already growing fastest.

This is particularly important as wealth income is capital-light, recurring, and less sensitive to interest rates. At a point when net interest margins are beginning to stabilise, the continued expansion of wealth management assets provides another durable earnings support.

Near-term headwinds, but structural thesis intact

The near-term costs of this disruption are real. Higher electricity tariffs will feed through to transport, logistics and industrial production costs, compressing margins in energy-intensive sectors and nudging headline inflation higher in the coming quarters. These cost pressures are genuine and should not be minimised.

Yet, the structural investment case for Singapore equities remains intact.

The key rerating catalysts, namely the Equity Market Development Programme, the Value Unlock package, sustained wealth inflows supporting banking sector earnings and a dividend yield that compares favourably with regional peers, have not been dislodged by this shock.

This revival was already under way before the crisis.

What the crisis now adds is an additional layer of tailwind: Gulf capital shaken loose by regional instability will need a destination, and Singapore is a natural one.

The Republic’s resilience has never been defined by the absence of shocks, but by its capacity to absorb and transmit them more effectively than its peers.

The current energy disruption is a test of that framework. On balance, Singapore continues to pass it.

The writer is a research analyst with the research and portfolio management team of FSMOne Singapore, the business-to-consumer division of iFast Financial

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services