External shocks cloud Vietnam’s market rerating path despite FTSE upgrade catalyst

Oil-driven inflation, currency pressure and persistent foreign outflows are weighing on sentiment

[HO CHI MINH CITY] Vietnam’s equity market is entering a period of heightened volatility, with mounting geopolitical risks overshadowing a widely anticipated upgrade to emerging-market status by FTSE Russell later this year.

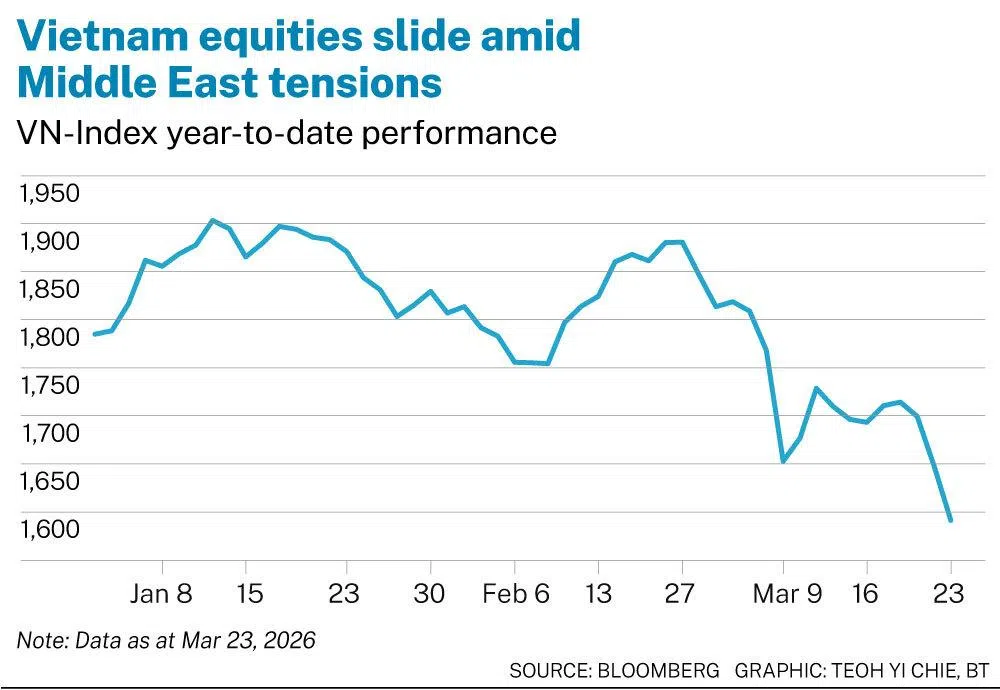

As at market close on Tuesday (Mar 24), the benchmark VN-Index had dropped 14.1 per cent from the beginning of March and was down 9.5 per cent for the year, reflecting a sharp deterioration in sentiment as investors grapple with rising global uncertainties and a surge in energy prices.

Analysts described the current environment as a “tug of war” between the upbeat outlook tied to a potential upgrade – expected to take effect on Sep 21 following an interim review outcome due on Apr 7 – and intensifying external shocks, particularly amid the unexpected developments of the conflict in the Middle East.

“Factoring in both the war and its broader macro implications, the more probable path remains a gradual decline (in the equity market) driven by continued de-risking,” Tyler Nguyen, chief market strategist at Ho Chi Minh City Securities (HSC), said on Tuesday.

However, he expected a short-term technical rebound that is supported by what American President Donald Trump called “productive” US-Iran talks. On Tuesday, the VN-Index climbed about 1.5 per cent, buoyed by gains in the US market.

Despite the FTSE policy advisory board meetings in March and an official upgrade decision expected in early April, brokerage shares – which are often seen as a proxy for retail and institutional risk appetite – have faced notable selling pressure since the beginning of March.

“(This suggests) that the market is currently pricing geopolitical risk above the upgrade catalyst,” Nguyen noted in a separate market note.

The weakness seen in the brokerage sector came alongside persistent foreign outflows, reinforcing concerns that global investors are turning more cautious on Vietnam even as structural reforms progress.

Foreign investors have recorded net sales of around 28 trillion dong (S$1.4 billion) in the year to date, after net equity outflows hit a record of more than US$5 billion in 2025 – even as the VN-Index rose more than 40 per cent last year.

Upgrade case strengthens

Vietnam is widely expected to be upgraded to Secondary Emerging Market status in September, with the outcome of FTSE Russell’s interim review set to come early next month.

Domestic regulatory changes effective from February, including the introduction of a “global broker model” that simplifies market access for foreign institutions, have addressed key bottlenecks that previously hindered inclusion.

Under the new framework, foreign institutional investors can execute trades via international brokers without opening local accounts, significantly reducing administrative hurdles and counterparty risk, as well as strengthening investor confidence.

FTSE earlier said that the interim assessment will evaluate whether sufficient progress has been made in facilitating global broker access – a key requirement for efficient index replication.

The capacity of domestic securities firms to execute Vietnam’s non-prefunding (NPF) model, in which brokers provide capital support for foreign buy orders, has also been closely monitored by the London-based index provider.

Vietcap analysts estimated that the total maximum NPF capacity of the five largest domestic brokerages, including Vietcap itself, is close to US$5 billion, comfortably exceeding the expected demand of around US$1.5 billion from index-tracking funds.

“Index-tracking funds are also set to disburse capital in multiple tranches, thereby alleviating concerns about NPF capacity,” the analysts said. They added that details on the disbursement schedule are expected alongside the Apr 7 announcement.

Another key milestone was the roll-out of the KRX trading system in May 2025, which addressed technical bottlenecks, such as order congestion, and introduced new features aimed at improving market efficiency.

Even so, analysts expect a more turbulent path ahead, with mounting downside pressure as global and domestic risks become increasingly evident.

“The global economy faces growing headwinds, and Vietnam is unlikely to remain insulated,” HSC’s Nguyen said. “In our view, these risks are still insufficiently priced into current valuations.”

At the centre of these concerns is a spike in oil prices driven by ongoing tensions in the Middle East, which is feeding quickly into Vietnam’s cost structure.

Quan Trong Thanh, head of research at Maybank Securities Vietnam (MSV), estimates that under a large-disruption scenario, the oil-price shock could add more than three percentage points to Vietnam’s monthly headline inflation, which may quicken to above 5 per cent.

According to government estimates, logistics costs in Vietnam are roughly 16 per cent of the country’s annual gross domestic product. This has amplified the speed and breadth of cost pass-through across the economy.

Retailers and suppliers are already feeling the strain. Logistics costs have reportedly risen 20 to 30 per cent for international shipping and 15 to 20 per cent domestically, while input costs across sectors – from livestock to steel – have surged.

Nguyen Minh Tam, a category director at WinCommerce – Vietnam’s largest modern retail chain operator – said on Mar 17 that 70 to 80 per cent of its suppliers have proposed price increases, particularly for imported fresh food, spices, fruits, meat and seafood, with adjustments ranging from 5 to 20 per cent depending on categories and input sources.

He added that, based on data from the firm’s more than 4,700 grocery outlets nationwide, consumers are growing more cautious, prioritising essential and value-for-money products.

Pressure is also spilling over to the dong, with the “free market” USD/VND rate rising 4.8 per cent since the outbreak of the conflict to close to 28,000 dong per dollar on Monday, surpassing its previous peak in November 2025, while the official rate remains flat in the year to date.

MSV’s Thanh assigned a 50 per cent probability to a cyclical downturn if geopolitical tensions in the Middle East last beyond two months, cautioning that corporate earnings could be squeezed by weaker demand and rising logistics, material and interest costs.

In this scenario, he expects marketwide earnings per share growth to slow to between negative 5 per cent and positive 6 per cent, with gains concentrated in energy and commodities while most other sectors, particularly highly leveraged firms, come under pressure.

“The market would likely encounter a notable correction due to both valuation de-rating and lower earnings per share,” Thanh said.

Even in a milder event-driven downturn – which Thanh assigned a 40 per cent probability, assuming the conflict lasts only four to six weeks – foreign investors are unlikely to return aggressively in the near term.

“Foreign investors, despite Vietnam’s stock-market upgrade, will also stay cautious to see how Vietnam can navigate external headwinds in order to manage high growth and macro stability,” he added.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

A ‘shadow bank’ hiding in Singapore’s Little India casts light on financial services gap

UOB CEO’s youngest child Grant Wee turns burnout into a wellness business

Can Seatrium build on its robust H1 earnings? UOBKH and DBS analysts have divided views

Yeoh Pei Xien: YTL’s third-gen scion with a pastor’s heart