Homes for living, not holding: Vietnam’s bold property pivot

As real estate prices rise, Hanoi is turning the rental market into a crucial pillar of its policy

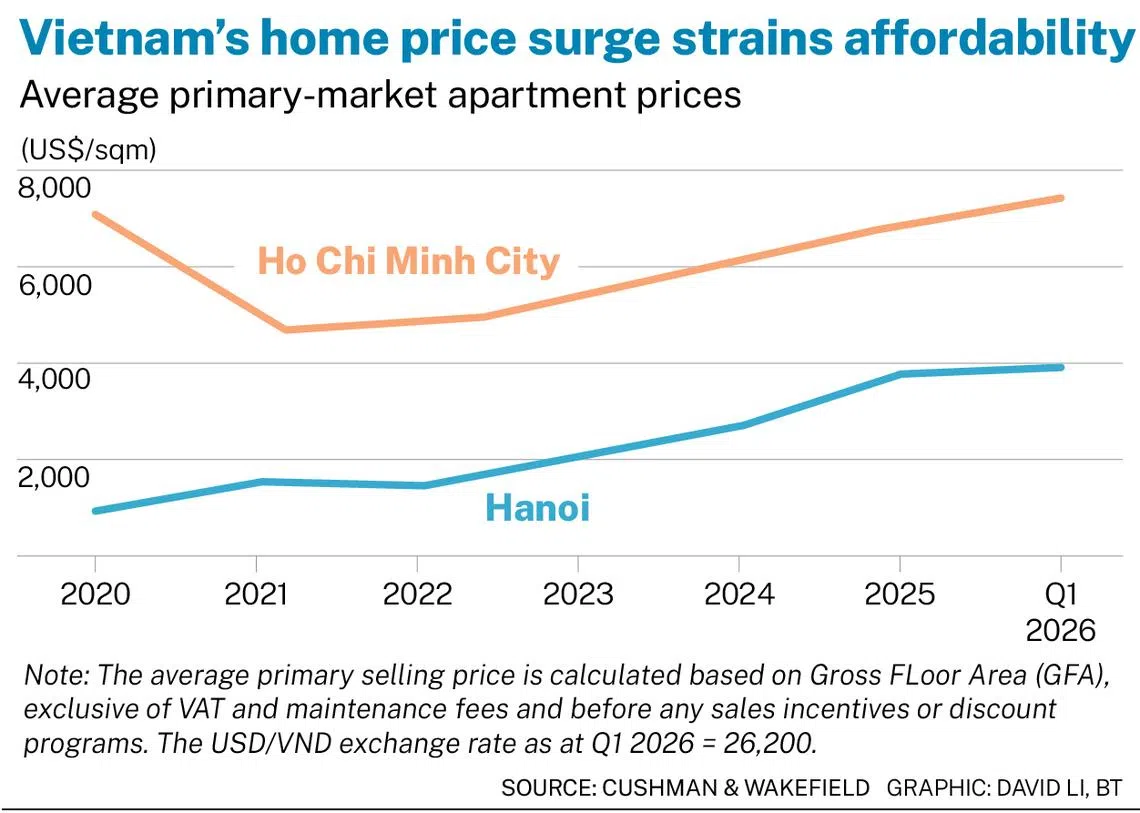

[HO CHI MINH CITY] Vietnam is trying to turn renting from a last resort into a pillar of its housing strategy, as runaway apartment prices put homeownership beyond the reach of many young workers and households.

The shift marks a break from one of the country’s most durable economic instincts: buy property, hold it and let land value build family wealth.

Vietnam’s president and Communist Party chief, To Lam, in May said that rental housing must be a “strategic pillar” until 2030, especially in major urban areas, industrial zones and areas where property prices have detached from local incomes.

Prime Minister Le Minh Hung also called for a “transformation in thinking”, shifting focus from “supporting ownership” to ensuring the “right to accommodation for all citizens”, in a statement on Jun 15 after a meeting with Ho Chi Minh City’s party leadership.

From ownership to access

The momentum for this transition is visible in the recent surge of private and public-sector participation in the rental market.

Various developers including big names such as Vingroup, Nam Long, CT Group and Novaland recently registered to build nearly 100,000 rental units in Ho Chi Minh City until 2030.

On Monday (Jun 22), Hanoi also broke ground on three rental housing projects that will provide about 8,000 units, located roughly 8 to 10 km from the downtown core of Hoan Kiem Lake.

The authorities are also considering increased state funding for national and local housing funds to support rental development, alongside incentives for private developers such as preferential credit and land-fee support.

“The shift is driven by a widening affordability gap,” said Thanh Huong, associate director of research and data-driven property consultancy platform S22M at Savills Vietnam.

“Housing prices in major cities have risen far beyond income growth, making homeownership increasingly unrealistic for young workers and newly married couples,” she noted.

The change also marks a notable turn for a market where real estate has long served as both shelter and the preferred store of wealth.

In the 1980s to the early 2000s, Vietnamese households had few alternatives beyond gold and property.

Today, younger households have more choices, from equities and bonds to funds and digital assets, reducing the need to treat property as the only path to asset accumulation, Huong pointed out.

That shift, combined with urbanisation and job mobility, is creating “growing acceptance of rental-based living”, she said, though “deep-rooted cultural barriers remain, and the institutional rental market is still in its very early stages”.

The trend for leasing homes is seen in other regions across the Asia-Pacific as well.

Savills observed that South Korea and China’s tier-one cities have also seen younger households rent for longer as property prices outpace incomes. It noted that Japan has the region’s most mature rental market.

The developer math

The biggest constraint of rental housing is economics.

Build-to-sell remains the dominant model because it gives developers faster capital turnover, higher margins and a familiar market mechanism. Vietnam’s low property holding costs, including minimal property and inheritance taxes, continue to reinforce the culture of buying and holding real estate as an asset.

Local developers have raised concerns that rental housing shifts the capital burden from households to developers, forcing them to wait years to recover their investment through rental income.

“Build-to-rent requires patient capital,” Huong added, noting that it could only become a meaningful segment “if key conditions are met”, including clear regulations, long-term financing and a maturing tenant base.

Yet commercial housing is under its own pressure, as much of the current pipeline remains concentrated in higher-priced segments. This further compounds the affordability crisis.

The bulk or roughly 86 to 88 per cent of new launches in Hanoi and Ho Chi Minh City between 2025 and the first quarter of this year comprised high-end and luxury residential units, according to SSI Research in a strategy report on the second half of 2026.

The market is caught between recovering supply and strained demand, as mortgage rates rose from 6.5 to 8.2 per cent in the fourth quarter of 2025 to 8.5 to 10 per cent in the first three months of this year.

Developers, meanwhile, are also facing higher financing costs, rising construction expenses and slower absorption.

It is no wonder then that recent policies in the country have markedly shifted towards improving housing affordability and strengthening social welfare, rather than continuing to prioritise commercial housing development as home prices skyrocket.

Towards that end, alongside efforts to promote new rental housing, 77 social housing projects were newly licensed in 2025, up 235 per cent from a year earlier.

As at end-April 2026, more than 780 social housing projects are under development or already in use in the country. These projects are expected to supply about 725,000 units – nearly three-quarters of Vietnam’s target of one million units by 2030.

The authorities are also steering credit towards segments aligned with the government’s policy priorities, including social housing, which has been carved out from banks’ tighter limits on real estate credit growth this year.

“This reinforces the government’s push to curb speculative demand and reaffirm the housing market’s basic function as providing a place to live,” SSI analysts noted.

Vietnam versus China housing demographics

The shift to rental housing does not mean Vietnam’s commercial housing market is losing its spark.

Analysts argue that the country’s structural drivers – young demographic profile, expanding middle class and shrinking household size – continue to underpin sustainable housing demand and support the market’s long-term prospect.

SSI Research pointed out that Vietnam’s demographic cycle remains more favourable than China’s when Beijing began tightening its property sector in 2020 – a policy move that triggered a prolonged downturn in one of the world’s largest housing markets.

The South-east Asian country’s median age is around 33, compared with China’s roughly 36 in 2016, while its urbanisation rate is still far lower at 38 per cent versus China’s 59 per cent.

“In Vietnam, this tightening cycle is emerging while housing demand is still expanding, creating a demographic advantage that could last for about another decade before the country moves closer to the ageing thresholds China is facing today,” it noted.

Some investors, meanwhile, see rental housing not as a replacement for ownership. Instead, they view social housing as the crucial middle rung between renting and buying private-market apartments.

Raymond Lim, founder and CEO of Singapore-based Vanguard Financial Group, said that Vietnam needs to provide its younger generation a realistic path to homeownership, mirroring the social role that Housing & Development Board public housing has played in Singapore.

“Rental is not the solution,” he pointed out. “You need to create a new class of asset that is government-subsidised”, with strict eligibility rules and without making the housing substandard.

“You need people to have a stake in the country, and real estate is always the easiest way to do it,” Lim said.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

ABSD deadline extended to up to 7 years for developers of large en bloc sites to encourage reuse of land

15-month wait-out curb lifted for private property owners buying HDB resale flats

Mortgagee-sale listings hit six-year high in H1 2026 as financing conditions tighten

Knight Frank winds down real estate agency unit, agents to move to OrangeTee & Tie