Singapore to reassess growth, inflation forecasts if necessary: DPM Gan

City-state faces an ‘unpredictable and uncertain’ global trading environment, says the deputy prime minister

[SINGAPORE] The Republic will reassess its growth and inflation forecasts if necessary, following the outbreak of conflict between the US, Israel and Iran, which has raised the risk of higher global energy prices, said Deputy Prime Minister Gan Kim Yong in Parliament on Monday (Mar 2).

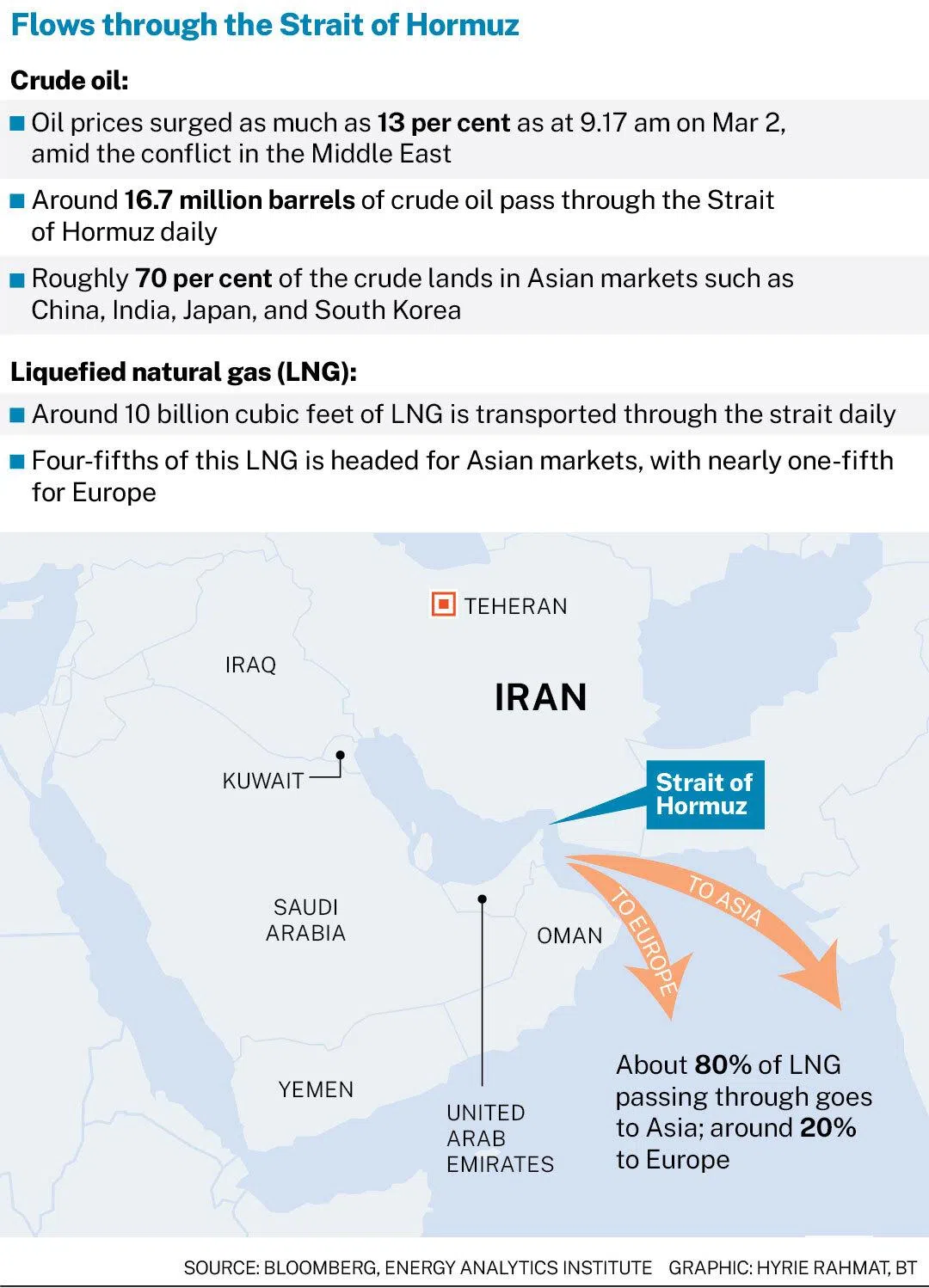

The US and Israel launched joint strikes on Iran on Feb 28, with Teheran retaliating by targeting Israeli territory and US military bases in the region. The Strait of Hormuz – a critical shipping route for crude oil and liquefied natural gas – has been closed in the near term as a result.

“This could result in an increase in global energy prices, depending on how protracted the conflict is,” said Gan, who is also minister for trade and industry. “Higher energy prices could lead to higher costs for businesses and consumers and weigh on the global and Singapore economies.”

Oil prices surged to a four-year high when markets reopened on Monday. Brent rallied as much as 13 per cent to above US$82 a barrel – the highest level since January 2025 – while West Texas Intermediate was near US$72.

“We are monitoring the developments closely, and will reassess our GDP (gross domestic product) and inflation forecasts, if necessary,” he added.

In a statement on Monday afternoon, the Monetary Authority of Singapore (MAS) said foreign exchange and money markets continue to function normally in the wake of the ongoing situation in the Middle East.

The Singapore dollar nominal effective exchange rate (S$NEER) also remains “within its appreciating policy band, which will continue to dampen imported inflationary pressures”.

MAS is monitoring developments arising from the conflict and is assessing its impact on the domestic economy and financial system.

“Complex” situation

Gan, speaking at the Ministry of Trade and Industry’s (MTI) Committee of Supply debate, warned that the current global trading environment remains “unpredictable and uncertain”.

“We face a more complex global environment marked by heightened great power competition, rising protectionism and a more fragmented global order,” he said.

On the tariff front, he noted that the US Supreme Court struck down the reciprocal tariffs imposed last year, but that the tariffs have since been replaced with a new Section 122 tariff of 10 per cent for up to 150 days.

President Donald Trump has also signalled his intention to raise this to 15 per cent, though details have yet to be finalised.

“There is still considerable uncertainty about how the tariff will evolve over time,” Gan said. He added that the government is working with partners of the Singapore Economic Resilience Taskforce (Sert) to provide information to businesses and workers and gather feedback to help them navigate these uncertainties.

Major structural forces are also reshaping industries, businesses and jobs, Gan noted.

Artificial intelligence and automation are transforming how value is created and how work is organised, while the global push towards decarbonisation is changing industrial processes, influencing investment patterns and affecting relative competitiveness.

Together with demographic constraints outlined during the Prime Minister’s Office’s Committee of Supply debate last week, Gan said that sustaining growth and creating good jobs would become “more challenging”.

Nevertheless, he noted that there remain “good opportunities for Singapore as a trusted, knowledge-driven and connected hub”, even in a more difficult environment.

The Sert committees are thus taking “a hard, honest look” at how Singapore must reset its economic strategy.

Gan added that the Republic would need to “work harder and smarter, be creative and take calculated risks and explore bold solutions” to reach the higher end of its GDP trend growth range of 2 to 3 per cent a year on average over the next decade, and to create good jobs.

Bishan-Toa Payoh GRC MP Saktiandi Supaat asked whether MTI has defined clear trigger conditions – such as sustained increases in energy costs or trade disruptions – under which targeted, time-bound enterprise support would be activated.

Gan replied that the government would continue to assess the situation, given Singapore’s significant dependence on Middle East energy supplies, and reiterated that a protracted conflict would have a “significant impact on the overall energy cost”.

Nevertheless, he added that Singapore has built up resilience against potential external shocks in energy supply over the past few years, though he did not elaborate on specifics for reasons of confidentiality and security.

Regional impact

In a research note, OCBC chief economist Selena Ling and senior Asean economist Lavanya Venkateswaran warned of a geopolitical risk premium and flight to quality in the near term, with the situation in the Middle East still fluid.

Businesses with exposure to the Middle East may have to deal with spillover effects such as trade diversion or higher risk premiums until the situation settles.

“The impact on global markets really depends on how prolonged the conflict is,” they added.

ANZ Research chief economist for South-east Asia and India Sanjay Mathur and Asia economist Krystal Tan echoed this view, noting that the economic impact on the region will hinge on the duration of the conflict and the time taken for political stability to re-emerge in Iran – factors that will determine how long oil prices stay elevated.

OCBC said that, for the region, sustained higher oil prices would hit trade balances, push up inflation and strain government budgets across the Asean-6 economies and India.

On trade, India, Indonesia, Malaysia, the Philippines, Thailand and Vietnam are all net petroleum importers and are exposed to a deterioration in their trade balances, said Ling and Venkateswaran.

OCBC estimates that a US$10-a-barrel increase in global oil prices would drag the current account balance by 0.5 per cent of GDP for Thailand; 0.4 per cent for the Philippines; 0.3 per cent for India; and 0.2 per cent for Indonesia, Malaysia and Vietnam.

ANZ flagged India and the Philippines as particularly vulnerable among the net importers – India because it is unlikely to be able to source discounted Russian oil as before, given trade commitments to the US, and the Philippines due to its large current account deficit of over 3 per cent of GDP.

Inflation and growth

On inflation, the pass-through will vary, depending on the level of subsidies in the region. OCBC estimates that the Philippines faces the biggest risk, with inflation potentially pushed up by 0.6 percentage points, followed by Singapore, India and Vietnam.

Yet both research houses believe the overall inflationary impact is manageable, noting that price pressures in 2025 were benign and headline inflation is expected to remain within most central banks’ target ranges, even with a persistent oil price spike.

ANZ added that a weaker US dollar would also help reduce import cost pressures across the region.

On growth, OCBC expects consistently higher oil prices to be marginally negative for GDP growth in Thailand, the Philippines, Vietnam and India. The impact will likely be more neutral for Indonesia and Malaysia.

ANZ was more sanguine. It believes that normalised demand, the ongoing tech supercycle and easing interest rates by the US Federal Reserve will offset the drag from higher energy costs, making a significant hit to regional growth unlikely.

OCBC said that if oil prices persist at elevated levels, central banks with a modest easing bias will likely have to reassess the room left for additional rate cuts.

ANZ concurred, though it noted that policy buffers have been rebuilt in the region, granting policymakers greater scope to intervene if needed.

For Singapore specifically, OCBC added that MAS may need to tighten monetary policy earlier than expected if higher imported costs are sustained.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

Knight Frank Singapore CEO Galven Tan resigns after 2.5 years at helm

ABSD deadline extended to up to 7 years for developers of large en bloc sites to encourage reuse of land

15-month wait-out curb lifted for private property owners buying HDB resale flats

Philippines’ income upgrade hides grim reality for most Filipinos